Counter-UAS Systems Market

In 2025, the Global Counter-UAS Systems Market was valued at approximately USD 3,214 million and is projected to reach around USD 8,472 million by 2030, expanding at a CAGR of about 21.4% during 2026–2030.

Explore reportFlight to the Future: Unlocking Competitive Edge in Aircraft Insulation.

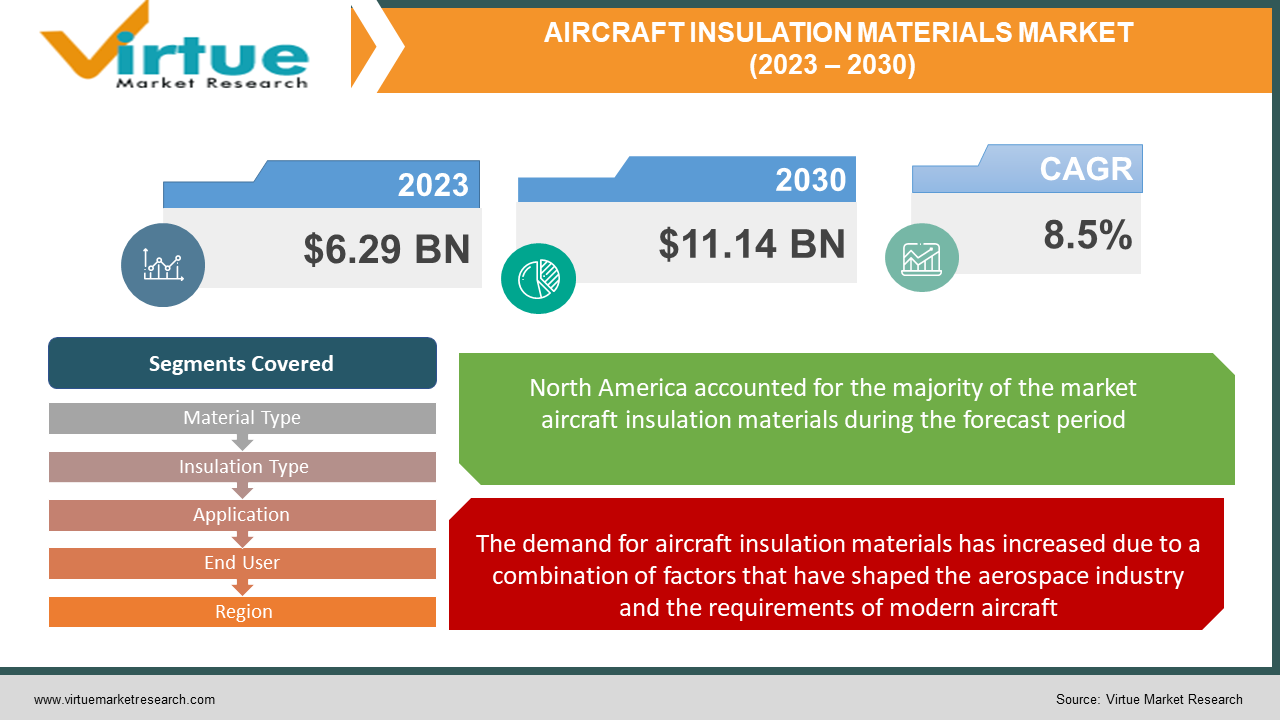

The Global Aircraft Insulation Materials Market was valued at USD 6.29 Billion and is projected to reach a market size of USD 11.14 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 8.5%.

Aircraft insulation materials are essential for maintaining a comfortable and safe environment inside an aircraft. They serve purposes such as thermal insulation, noise reduction, fire protection, and vibration dampening. Common materials include fiberglass, ceramic fiber, foam, and fire-resistant materials. These materials address specific needs like heat resistance, soundproofing, and safety compliance. The choice of materials depends on factors like aircraft requirements, regulations, weight considerations, and eco-friendliness. Advancements continue to enhance cabin comfort, safety, and fuel efficiency. Companies are investing heavily in research and development to create materials that meet the highest standards of performance and sustainability. 3D printing is also being used to create lighter, stronger, and more thermally efficient components. New materials such as graphene are also being explored for their potential in the aerospace industry.

Global Aircraft Insulation Materials Market Drivers:

The demand for aircraft insulation materials has increased due to a combination of factors that have shaped the aerospace industry and the requirements of modern aircraft.

The global aircraft insulation materials market has been driven by factors including the growing demand for air travel, a focus on passenger comfort, stringent safety standards, technological advancements, fuel efficiency goals, the emergence of electric aircraft, retrofitting needs, market competition, and global economic growth. These drivers have led to the development of advanced insulation materials that enhance thermal efficiency, noise reduction, and safety while accommodating industry trends and regulatory requirements.

The increasing emphasis on passenger comfort and safety aligns with the growing demand for advanced aircraft insulation materials, providing both a comfortable travel experience.

The soaring demand for health-conscious and environmentally sustainable solutions has driven a remarkable expansion in the Aircraft Insulation Materials Market. Providing a seamless synergy of functionality and efficiency, aircraft insulation materials meet the diverse needs of the aviation industry and safety regulations. These materials, carefully engineered for optimal thermal insulation, noise reduction, and fire protection, not only enhance passenger comfort but also underline the aviation sector's dedication to safety and performance. By prioritizing both comfort and security, aircraft insulation materials reflect a commitment to responsible aviation practices, aligning with the industry's efforts towards a safer, more efficient, and environmentally conscious future.

Global Aircraft Insulation Materials Market Challenges:

The Global Aircraft Insulation Materials Market is influenced by diverse challenges. Stricter safety regulations demand rigorous testing and higher R&D investments. Weight constraints necessitate lightweight yet effective materials, impacting design choices. Growing environmental concerns require sustainable options, potentially increasing costs. Rapid technological advancements mandate adaptable solutions for evolving aircraft designs. Balancing cost and quality underpins decisions. Supply chain disruptions can lead to delays and increased expenses. Complex installation processes heighten labor costs. Compatibility with various aircraft types drives material versatility. Economic fluctuations affect demand. Successfully navigating these challenges requires innovation, flexibility, and industry collaboration.

Global Aircraft Insulation Materials Market Opportunities:

The Global Aircraft Insulation Materials Market is poised for growth through various opportunities. Leveraging technological advancements enables the creation of more efficient and innovative insulation materials, to meet evolving industry demands. Developing eco-friendly solutions aligns with sustainability trends and attracts environmentally conscious customers. As airlines modernize their fleets and retrofit existing aircraft, there's a demand for cutting-edge insulation materials to enhance passenger comfort and safety. Noise reduction solutions cater to passengers seeking quieter cabins. Lightweight materials support fuel efficiency goals, especially in electric and hybrid aircraft. Collaboration drives novel solutions, while customization, safety enhancements, and wellness-focused materials cater to diverse market segments. Embracing these opportunities positions the market for expansion and innovation.

The aviation industry has encountered significant challenges stemming from the COVID-19 outbreak, precipitating a range of economic issues. Since the pandemic's onset, the civil aviation sector has emerged as one of the hardest-hit industries globally. The International Civil Aviation Organization (ICAO) and the International Air Transport Association (IATA) have taken an active role in monitoring the pandemic's economic repercussions on aviation, frequently issuing reports and forecasts. Consequently, the civil aviation industry has witnessed a reduction in aircraft deliveries and increased backlogs due to diminished flight volumes. This drop in flight activity has, in turn, led to decreased demand for aircraft insulation across various applications within the civil aviation sector, including cabin interiors, flooring, landing gear doors, engine nacelles, aircraft tires, and other components.

Global Aircraft Insulation Materials Market Developments:

On September 2019, BASF SE achieved a breakthrough by introducing a novel particle foam derived from polyethersulfone (PESU). Notable for its impressive attributes such as flame retardancy, remarkable high-temperature endurance, and a lightweight profile, this foam represents a significant advancement in materials technology.

On March 2019, witnessed a strategic move as Transdigm Group, Inc. completed the acquisition of Esterline Technologies Corporation, a distinguished entity involved in aircraft components, machinery systems, and aircraft insulation solutions. This acquisition served to fortify Transdigm Group, Inc.'s global position within the competitive aircraft insulation market, bolstering its overall industry influence.

AIRCRAFT INSULATION MATERIALS MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2022 - 2030 |

|

Base Year |

2022 |

|

Forecast Period |

2023 - 2030 |

|

CAGR |

8.5% |

|

Segments Covered |

By Material Type, Insulation Type, Application, End User, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Duracote , BASF SE, Rogers Corporation, Triumph Group, Boyd Corporation, Zodiac Aerospace |

Global Aircraft Insulation Materials Market Segmentation:

The thermal insulation segment has consistently been a significant component of the aircraft insulation materials market. Thermal insulation materials play a crucial role in maintaining comfortable cabin temperatures, enhancing energy efficiency, and managing temperature differentials in various aircraft components. With the aviation industry's ongoing emphasis on fuel efficiency and passenger comfort, the thermal insulation segment has experienced highest market share. While the acoustic insulation segment has the fastest growth. As passenger expectations for a quieter and more comfortable cabin experience increase, the demand for effective noise reduction solutions has grown. Acoustic insulation materials are essential to dampen engine noise, vibrations, and external sounds, contributing to a more enjoyable flight for passengers. This segment has shown strong potential for growth due to the focus on passenger comfort.

A number of foam insulation materials have gained popularity due to their lightweight nature and outstanding insulation properties, including polyurethane foam and expanded polystyrene (EPS). A wide range of aircraft applications include cabin interiors, walls, ceilings, and cargo holds. Aviation has seen the highest growth in foam insulation because of the demand for lightweight, efficient insulation materials. While Fiberglass insulation materials have been widely used in aviation for their thermal and acoustic insulation capabilities. They may not experience the same rate of growth as newer materials, fiberglass has fastest growth due to its proven performance and compatibility with industry requirements.

The engine segment involves insulation materials used within the aircraft's engines for thermal management and noise reduction. Insulation materials in this segment help regulate engine temperature, optimize performance, and enhance overall efficiency. While the demand for efficient and lightweight insulation solutions is expected to continue, the growth rate of this segment is fastest and influenced by factors such as advancements in engine technology and regulatory requirements for noise reduction. While the airframe segment includes insulation materials used throughout the aircraft's structural components, such as cabin interiors, fuselage, wings, and tail sections. This segment is vital for maintaining passenger comfort, managing temperature differentials, and ensuring noise reduction. With a highest growing on passenger experience and safety regulations, the airframe insulation materials segment has shown steady demand.

The commercial aircraft segment has traditionally been a significant driver of demand for aircraft insulation materials. With the growth in air travel, airlines continuously seek to improve passenger comfort and enhance cabin environments. This segment has seen highest market share in insulation materials to ensure thermal comfort, noise reduction, and safety compliance. However, the growth rate of this segment may be influenced by factors such as fluctuations in air travel demand, airline fleet expansion, and the emergence of more fuel-efficient aircraft models. While the military aircraft segment also requires insulation materials for various applications, including combat aircraft, transport planes, and helicopters. Military aircraft have specific requirements related to stealth, protection, and operational performance. While this segment may not experience the same level of growth as commercial aviation, advancements in military aircraft technology and has fastest growth.

North America has highest market share in the region for the aerospace industry, with a large number of aircraft manufacturers, airlines, and MRO (maintenance, repair, and overhaul) facilities. The region's established aviation infrastructure and technological innovation have contributed to its prominence in the aircraft insulation materials market. The growth rate in North America may be influenced by factors such as fleet expansion, advancements in aviation technology, and regulatory requirements. While Asia Pacific region has witnessed fastest growth in air travel demand due to the rising middle class, economic growth, and urbanization. As a result, airlines in the region have been expanding their fleets, contributing to the demand for aircraft insulation materials.

Global Aircraft Insulation Materials Market Key Players:

The key types of insulation materials used in the global aircraft industry include thermal insulation, acoustic insulation, fire-resistant insulation, and specialized materials for various applications.

The demand for aircraft insulation materials varies based on applications such as cabin interiors, engine compartments, landing gear components, cockpit, avionics, and cargo holds.

Commercial aircraft manufacturers and operators, as well as military aviation entities, are key end-users driving the growth of the global aircraft insulation materials market.

The Asia Pacific region, driven by rising air travel demand and expanding aviation markets, is witnessing both high demand and fast growth in the aircraft insulation materials market.

Manufacturers in the global aircraft insulation materials market face challenges related to stringent regulations, weight considerations, environmental concerns, and supply chain disruptions

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.