AI in Preventive Care market Size (2023 – 2030)

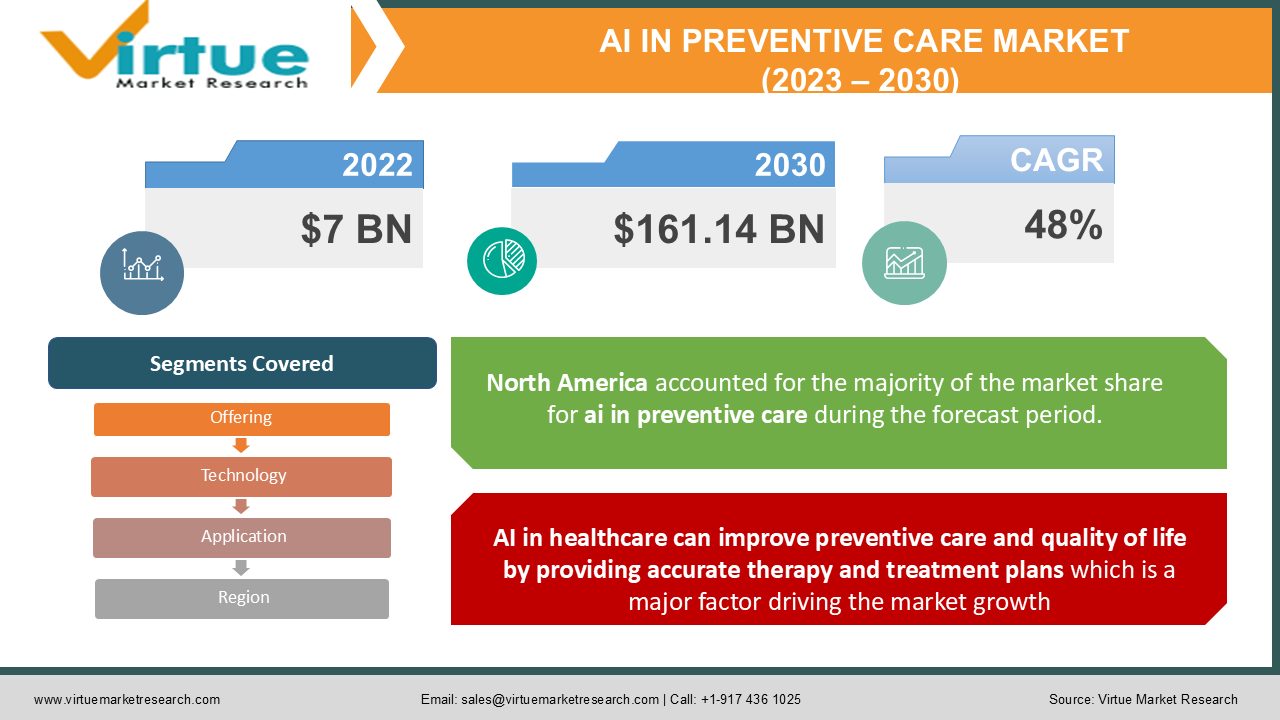

The AI in the preventive care market was valued at USD 7 billion in 2022 and is projected to reach USD 161.14 billion by 2030. The market is anticipated to expand with a stellar CAGR of 48% over the forecast period. The market's growth is being fueled by an upsurge of massive and complicated medical databases, a burgeoning need to minimise healthcare costs, enhanced computing power and decrease in hardware costs, and an increase in the number of partnerships and collaborations among different players in the healthcare sector, and a growing need for improved healthcare services due to a workforce-patient imbalance.

INDUSTRY OVERVIEW:

In the worldwide healthcare sector, artificial intelligence (AI) has evolved as a radical revolutionary force. The substantial influence of AI-driven solutions has benefited both providers and seekers along the patient care continuum. The healthcare industry has grown and changed at an extraordinary pace over the last decade, and AI integration has played a critical role in this industry. From chronic illnesses like cancer to radiologic treatments and risk evaluation, AI in healthcare provides companies with several potentials to rely on cutting-edge technology to provide more efficient solutions. AI has significant advantages over conventional analytical methodologies and decision-making processes in the healthcare industry.

Within the wide AI spectrum, machine learning, cloud computing, and deep learning algorithms have enabled healthcare practitioners to acquire useful insights into diagnostics and care procedures, resulting in reduced treatment variability and more accurate clinical outcomes. Because AI effortlessly duplicates human cognition in the interpretation and analysis of complicated healthcare data, it has caused huge advancements in healthcare. In essence, the technique relies on computer algorithms to arrive at major judgments, with no human involvement.

AI-based health apps attempt to simplify and innovate treatment methods to produce accurate patient results. Many world-renowned medical institutes, like Memorial Sloan Kettering Cancer Center, the NHS in the United Kingdom, and the Mayo Clinic, have created cutting-edge AI-powered algorithms and technologies. Disease diagnosis, medication discovery, treatment protocol creation, patient monitoring and care, and customised medicine development are all areas where these techniques are useful. Furthermore, major tech giants, like Google, Apple, and IBM, have made forays into the healthcare field in recent years by building AI algorithms.

COVID-19 IMPACT ON AI IN THE PREVENTIVE CARE MARKET:

Due to the increased use of AI and ML solutions in the healthcare sector, the AI in healthcare market has historically seen considerable growth. One of the most important foundations in global health crisis management is artificial intelligence. During these difficult times, AI has made disease detection, medicine research, and robot delivery far more efficient. The outbreak of the COVID-19 pandemic provided a chance to demonstrate AI's capabilities and expertise in the healthcare industry. During the pandemic's second wave, medical facilities all over the world used AI-based automated systems, inpatient care bots, and AI-assisted surgery robots to deal with the constant influx of patients, which would have otherwise swamped the whole hospital operating cycle.

MARKET DRIVERS:

AI in healthcare can improve preventive care and quality of life by providing accurate therapy and treatment plans which is a major factor driving the market growth:

AI in healthcare has expanded its relevance as a crucial tool for combatting epidemics and pandemics, as it may improve preventative care and quality of life, lead to accurate diagnosis and treatment strategies, and improve overall patient outcomes. Artificial intelligence integration may increase the accuracy of radiological instruments and, in certain circumstances, replace the requirement for tissue samples, which is likely to fuel market revenue growth throughout the projection period. Artificial intelligence can potentially help to alleviate a skills shortage by taking over some diagnostic duties that are traditionally performed by humans.

AI streamline and automates many operations and also aidsI in research and development:

AI also allows researchers to examine large amounts of data for a more effective study of infectious and rarer diseases, which can aid in the development of more reliable diagnostic and treatment methods. Implementation of artificial intelligence (AI) into electronic health records (EHRs) to create more intuitive interfaces and automate regular operations to save time and money is another significant driver projected to promote market revenue growth in the future. Artificial intelligence may also increase the ability of medical devices to monitor patients in ICU and assess issues, resulting in better patient outcomes and lower healthcare costs. These are some of the major aspects likely to contribute to market revenue growth in the future.

MARKET RESTRAINTS:

Medical professionals' apprehension about using AI-based technology is hampering the market growth:

With the rapid advancement of digital health and mobile health technology, healthcare practitioners may now assist patients with unique treatment options. Doctors may use AI technology to help them diagnose and treat patients more efficiently. However, doctors have been seen to be wary of new technology. Doctors and professionals feel that qualities like empathy and persuasion are human abilities, and AI cannot eliminate the need for a doctor. Furthermore, there is a risk that patients would become overly reliant on these technologies and will forego critical in-person treatments, thus jeopardising long-term doctor-patient relationships.

Concerns regarding data privacy are a major factor inhibiting the adoption of AI in the healthcare industry:

In the medical field, AI has numerous applications. Due to data privacy issues, however, AI use in the sector is limited. In some nations, federal regulations safeguard patient health data, and any violation or failure to keep it secure can result in legal and financial consequences. Because AI for patient care necessitates access to a variety of health information, AI-based technologies must follow all data security procedures put out by governments and regulatory agencies. This is a challenging process because most AI platforms are concentrated and demand a lot of computational capacity, thus patient data, or portions of it, may need to be stored in a vendor's data centre. The vendor data centres are not secure enough to prevent data breaches since the data is available to a wide range of personnel, making it harder to contain breaches. If patient data is accidentally exposed from these data centres, it can result in massive litigation and payment demands from aggrieved parties. Thus, the aforementioned reasons are negatively impacting the market growth.

AI IN PREVENTIVE CARE MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2022

|

|

Forecast Period

|

2023 - 2030

|

|

CAGR

|

48%

|

|

Segments Covered

|

By Offering, Technology, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Intel, Koninklijke Philips, Microsoft, IBM, Siemens Healthineers, Nvidia, Google, General Electric Company, Medtronic Micron Technology, Amazon Web Services, Johnson & Johnson, General Vision, CloudmedX Oncora Medical, Enlitic, Gauss Surgical Qventus, Desktop Genetics, Cylance Ginger.io, Pillo

|

This research report on AI in the preventive care market has been segmented and sub-segmented based on Offering, By Technology, By Application, By End - User and By Region.

AI IN THE PREVENTIVE CARE MARKET - BY OFFERING

-

Hardware

-

Software

-

Services

Based on offering, the AI in the preventive care market is segmented into Hardware, Software and Services. Owing to the fast-expanding acceptance rate of AI-based technology solutions among medical providers, payers, and patients, the software solutions category led the market for artificial intelligence in healthcare in 2021, accounting for the biggest revenue share of 39.9%. Over the projection period, the software segment is projected to develop profitably. The increasing prevalence of AI-based technologies in numerous healthcare applications, such as cybersecurity, clinical trials, virtual assistants, robot-assisted surgeries, telemedicine, dose error reduction, and fraud prevention, is responsible for this large market share. Furthermore, an increasing number of strategic efforts, such as alliances and seed investments, conducted by major market players are contributing positively to the development of the market.

AI IN THE PREVENTIVE CARE MARKET - BY TECHNOLOGY

Based on Technology, the AI in the preventive care market is segmented into Machine learning, Natural Language Processing, Context-Aware Computing and Computer Vision. Machine learning led the global AI in the prevention care market in 2021. During the projected period, the machine learning segment is expected to grow at a faster rate. Because medical facilities and healthcare systems generate vast volumes of data, most algorithms use machine learning methodologies to uncover patterns and anticipate results, resulting in this segment's market domination. Moreover, pharmaceutical and biotechnology companies are increasingly relying on machine learning for drug-genomic applications since it extracts meaningful information from big data sets and complements genomic research, as a result propelling the market towards growth.

AI IN THE PREVENTIVE CARE MARKET - BY APPLICATION

Based on application, the AI in the prevention care market is divided into Medical Administration and Support, Patient Management, Research & Development, and others. The Patient Management application is poised to experience significant growth over the forecast period. Medical specialists and researchers now have access to a wide range of unstructured and unprocessed data that was previously unavailable. As a result of the increased volume of data, healthcare institutions have turned to current big data analytics and information-driven solutions. Healthcare practitioners are becoming more interested in AI's growing role in diagnosing patient symptoms and tracking their development through various phases of sickness. Apart from its benefits, this is the key reason why real-time remote patient monitoring systems may bring a long-term paradigm change in healthcare improvement.

AI IN THE PREVENTIVE CARE MARKET - BY END-USER

-

Pharmaceutical Companies

-

Hospitals

-

Patients

-

Others

Based on end-user, the AI in the prevention care market is divided into pharmaceutical companies, Hospitals, and Patients. The pharmaceutical company segment accounted for the greatest proportion of the market in 2021. Because of the introduction of unique and effective solutions for health diagnosis and monitoring, the AI market in preventative care is expected to grow substantially. Artificial intelligence may speed up the development process and reduce the risk associated with the manufacturing of pharmaceutical products, making it simpler for doctors to research complex disorders at the genetic level, which is eventually driving the market growth. Pharmaceutical companies rely on data to prove the safety and efficacy of their products. As a consequence, AI helps to make data analysis more efficient and safer. This market is also expected to rise because of the rising prevalence of diseases including cancer and genetic disorders, as well as the growing demand to reduce drug development time and costs.

AI IN THE PREVENTIVE CARE MARKET - BY REGION

-

North America

-

Europe

-

The Asia Pacific

-

Latin America

-

The Middle East

-

Africa

By region, the AI in the prevention care market is grouped into North America, Europe, Asia Pacific, Latin America, The Middle East and Africa. North America emerged as the largest regional market in AI in the prevention care market in 2021 and contributed the largest revenue share of 57.4%. and is anticipated to continue with the trend during the forecast period. Developments in healthcare IT infrastructure, increasing medical expenditures, mass acceptance of AI/ML technologies, favourable government initiatives, attractive funding opportunities, and the existence of numerous significant industry competitors are driving the market. Furthermore, the expanding elderly population, changing lifestyles, higher incidence of chronic illnesses, burgeoning need for value-based care, and increased awareness of AI-based technologies are all contributing to market expansion in North America. The Asia Pacific area, on the other hand, is estimated to rise at the quickest rate of 45 % over the projection period. The significant developments and improvements in IT infrastructure, as well as entrepreneurial initiatives focusing on AI-based technologies, are responsible for this growth rate. Private investors, venture capitalists, and non-profit organisations are increasing their investments to improve therapeutic results, data analysis, and security, as well as lower costs. Some of the main drivers driving the Asia Pacific market's growth include favourable government policies enabling and pushing healthcare organisations and care providers to quickly embrace AI-based technology.

AI IN THE PREVENTIVE CARE MARKET - BY COMPANIES

Due to the existence of a large number of competitors in the industry operating in both the local and foreign markets, artificial intelligence in the preventative care market is extremely competitive and fragmented. Because of the growing use of AI in numerous medical fields, major market participants are pursuing tactics such as product development and mergers and acquisitions. Some of the major players operating in the AI in the preventive care market include

- Intel

- Koninklijke Philips

- Microsoft

- IBM

- Siemens Healthineers

- Nvidia

- Google

- General Electric Company

- Medtronic

- Micron Technology

- Amazon Web Services

- Johnson & Johnson

- General Vision

- CloudmedX

- Oncora Medical

- Enlitic

- Gauss Surgical

- Qventus

- Desktop Genetics

- Cylance

- Ginger.io

- Pillo

NOTABLE HAPPENING IN AI IN THE PREVENTIVE CARE MARKET

- PRODUCT LAUNCH- Philips introduced two new HealthSuite solutions in August of 2021. HealthSuite solutions enable health systems to link informatics applications that may be merged and scaled up or down based on changing requirements.

- INVESTMENT- In January 2020, Microsoft, a well-known American company, unveiled AI for Health, a five-year, USD 40 million initiative aimed at helping healthcare institutions use artificial intelligence and machine learning to improve the health of patients and communities.

- COLLABORATION- Care.ai and NVIDIA formed a partnership in October 2019 to deliver ai - powered automated health tracking in healthcare utilizing NVIDIA's platform. The agreement will enable healthcare institutions to improve patient safety and staff efficacy by combining care.ai's independent monitoring system with NVIDIA's Jetson technology.

- COLLABORATION- EBSCO Information Services and IBM Watson Health partnered in March 2020 to give companies with access to evidence-based medication and ailment data, which might help them better deal with serious contagious diseases like COVID-19.

- ACQUISITION- In July 2019, IBM announced the acquisition of RedHat to combine its innovation and industry knowledge with RedHat's open hybrid cloud technology. The firms collaborated to create a next-generation heterogeneous multi-cloud platform for healthcare organisations, which allows them to securely manage healthcare data and run apps across numerous public and private clouds and premises.