Virtual Load Balancer Market Size (2024 – 2030)

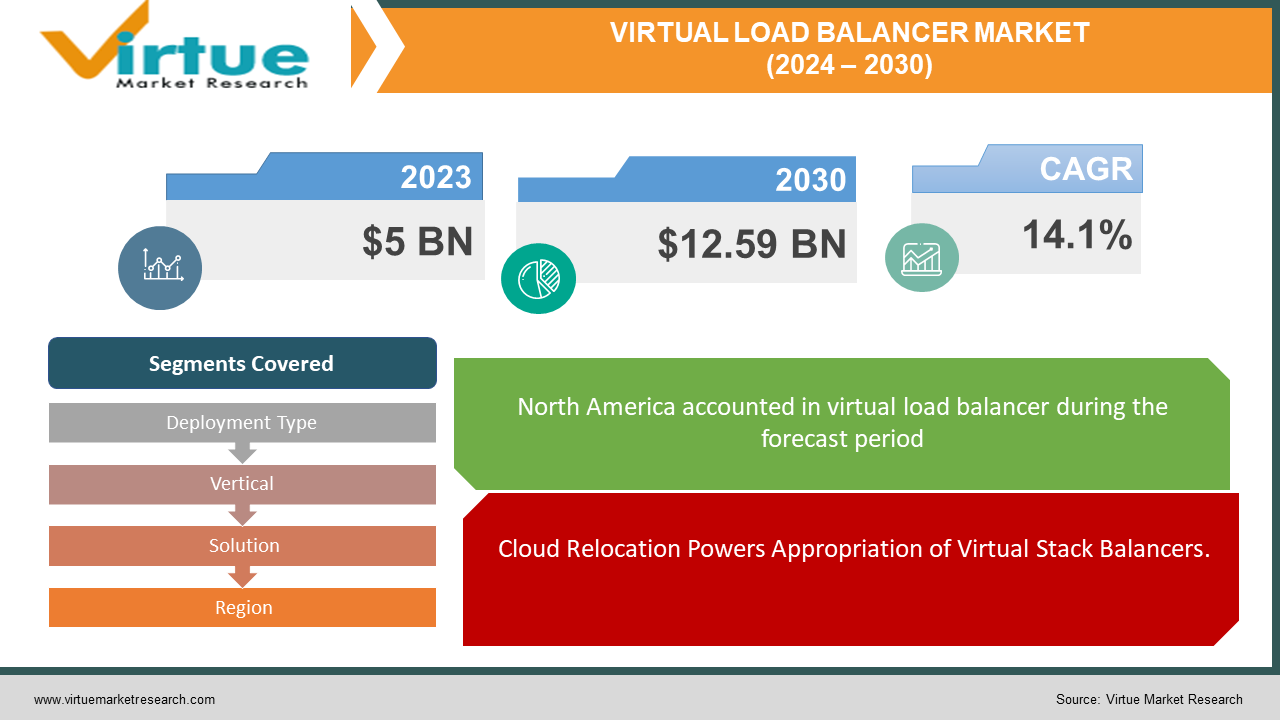

The market for global virtual load balancer market was estimated to be worth 5 USD billion in 2023 and is expected to increase to 12.59 USD billion by 2030, with a projected compound annual growth rate (CAGR) of 14.1% from 2024 to 2030.

The Worldwide Virtual Stack Balancer showcase presents an energetic scene characterized by the rising request for productive and versatile application conveyance arrangements. Virtual stack balancers play an essential part in dispersing approaching organized activity over numerous servers or assets, guaranteeing ideal execution, unwavering quality, and accessibility of applications and administrations. With the multiplication of cloud computing, virtualization, and containerization advances, organizations are progressively embracing virtual stack balancers to address advancing versatility prerequisites, improve application conveyance, and optimize asset utilization. In addition, the developing complexity of cutting-edge IT structures, coupled with the requirement for consistent application conveyance over conveyed situations, drives the selection of virtual stack balancer arrangements. Key advertise players ceaselessly improve to offer progressed functionalities such as application-aware stack adjusting, activity administration, SSL/TLS end, and security highlights to cater to differing client needs and utilize cases. As businesses prioritize advanced change activities and grasp cross-breed and multi-cloud situations, the Worldwide Virtual Stack Balancer showcase is balanced for maintained development, driven by the basic for solid and effective application conveyance arrangements within the advanced time.

Key Insights:

Cloud-based virtual load balancer solutions accounted for 60% of total market revenue in 2022, reflecting the increasing adoption of cloud-native architectures and hybrid cloud environments.Large enterprises emerged as the leading adopters, contributing to 45% of total market revenue in 2022, driven by their complex IT infrastructures and scalability requirements.The Asia-Pacific region experienced the highest growth rate, with a CAGR of 12% during the forecast period, attributed to rapid digital transformation initiatives and increasing investments in IT infrastructure.Despite market growth, 25% of surveyed organizations reported challenges with ensuring seamless integration and interoperability of virtual load balancer solutions with existing IT environments, leading to deployment delays and operational inefficiencies.

Global Virtual Load Balancer Market Drivers:

Cloud Relocation Powers Appropriation of Virtual Stack Balancers.

The expanding selection of cloud computing and movement to cloud-native models are critical drivers moving the Worldwide Virtual Stack Balancer advertise. As organizations move their applications and workloads to the cloud, the requirement for versatile, adaptable, and flexible application conveyance arrangements gets to be foremost. Virtual stack balancers offer energetic activity conveyance, consistent versatility, and tall accessibility over cloud situations, empowering organizations to optimize execution, decrease inactivity, and improve client encounters in cloud-based applications.

Rising Request for Application Execution Optimization.

In today's computerized scene, where client involvement and application execution are basic differentiators, there's a developing request for virtual stack balancers to optimize application conveyance and guarantee consistent execution. With the expansion of high-traffic, latency-sensitive applications such as e-commerce stages, spilling administrations, and online gaming, organizations require productive activity administration, SSL offloading, and substance caching capabilities advertised by virtual stack balancers. These arrangements offer assistance relieve execution bottlenecks, moving forward reaction times, and improving general application unwavering quality, driving their selection over businesses.

Accentuation on Security and Compliance in Application Conveyance.

Security and compliance contemplations play a vital part in application conveyance, particularly in businesses taking care of touchy information and controlled workloads. Virtual stack balancers offer progressed security highlights such as Web Application Firewall (WAF), DDoS security, and SSL encryption to protect applications and relieve cyber dangers. Moreover, compliance orders such as PCI DSS, HIPAA, and GDPR require organizations to actualize vigorous security measures in their application conveyance framework. Virtual stack balancers address these necessities by giving granular get-to controls, encryption conventions, and risk location components, hence serving as indispensable components in guaranteeing secure and compliant application conveyance situations.

Global Virtual Load Balancer Market Restraints and Challenges:

Integration Complexity Ruins Showcase Selection.

The Worldwide Virtual Stack Balancer showcase faces challenges related to the complexity of joining these arrangements into existing IT foundations. Numerous organizations work in heterogeneous situations with assorted structures, conventions, and sending models, making consistent integration an overwhelming errand. Compatibility issues, setup complexities, and interoperability limitations can lead to sending delays, operational disturbances, and expanded usage costs, subsequently preventing showcase selection of virtual stack balancers.

Execution Bottlenecks and Adaptability Concerns Affect Advertise Development.

Despite headways in virtual stack balancer innovations, a few arrangements may experience execution bottlenecks and versatility challenges, especially in high-traffic or resource-constrained situations. Issues such as inactivity, throughput restrictions, and asset disputes can debase application execution and client encounters. Moreover, scaling virtual stack balancers to suit developing workloads and fluctuating activity designs may pose versatility concerns, requiring cautious capacity arranging and optimization techniques to guarantee consistent adaptability and execution.

Security Vulnerabilities Posture Dangers to Application Conveyance Foundation.

Security vulnerabilities in virtual stack balancer arrangements display noteworthy dangers to application conveyance foundation, possibly uncovering organizations to cyber dangers, information breaches, and compliance infringement. Malevolent assaults focusing on vulnerabilities in stack balancer programs or misconfigurations can compromise the secrecy, judgment, and accessibility of basic applications and information. Besides, rising dangers such as application-layer assaults, botnets, and zero-day misuses require proactive security measures and persistent checking to moderate dangers viably. Tending to security vulnerabilities and improving risk location capabilities are fundamental for organizations looking to secure their application conveyance framework and keep up administrative compliance in the confront of advancing cyber dangers.

Global Virtual Load Balancer Market Opportunities:

Quickened Selection of Crossover and Multi-Cloud Situations Drives Advertise Development.

The Worldwide Virtual Stack Balancer showcase presents noteworthy openings driven by the quickened selection of half-breed and multi-cloud designs among organizations. As businesses look to use the adaptability, adaptability, and cost-efficiency of cloud computing, the request for virtual stack balancers to guarantee consistent application conveyance over-dispersed situations is balanced to surge. Virtual stack balancers offer energetic activity administration, adaptability, and tall accessibility highlights basic for optimizing execution and strength in crossover and multi-cloud organizations, situating them as crucial components of advanced IT frameworks.

Development of Edge Computing Activities Fills Request for Edge Stack Adjusting Arrangements.

The expansion of edge computing activities, driven by the requirement for low-latency, high-bandwidth applications, presents profitable openings for virtual stack balancer sellers to offer edge stack adjusting arrangements. Edge stack balancers empower organizations to disseminate application workloads closer to end-users, diminishing inactivity, making strides in responsiveness, and upgrading client encounters for latency-sensitive applications such as IoT, gushing media, and real-time analytics. With the developing selection of edge computing models over businesses, the request for edge stack adjusting arrangements are anticipated to rise, making a prolific showcase scene for virtual stack balancer suppliers to capitalize on.

Grasp of DevOps Hones Goads Development in Application Conveyance Robotization.

The expanding grasp of DevOps hones and mechanization in application advancement and sending forms present openings for virtual stack balancer sellers to enhance and offer robotized application conveyance arrangements. Virtual stack balancers coordinate with DevOps toolchains and organization stages to empower consistent integration, persistent sending, and robotized provisioning of application conveyance administrations, streamlining arrangement workflows, diminishing manual intercessions, and quickening time-to-market for applications. As organizations prioritize dexterity, adaptability, and mechanization in their DevOps activities, the request for virtual stack balancers with vigorous robotization capabilities is anticipated to take off, driving showcase development and advancement in application conveyance computerization.

VIRTUAL LOAD BALANCER MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

14.1% |

|

Segments Covered

|

By Deployment Type, Vertical, Solution, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

F5 Networks, Inc., Citrix Systems, Inc.,Radware Ltd., Kemp Technologies, Inc., A10 Networks, Inc., Fortinet, Inc., Barracuda Networks, Inc., NGINX, Inc. (acquired by F5 Networks), Avi Networks (acquired by VMware), HAProxy Technologies, Inc., Array Networks, Inc., Brocade Communications Systems, Inc.

|

Virtual Load Balancer Market Segmentation: By Deployment Type

-

On-premises

-

Cloud-based

-

Hybrid

Among the different arrangement sorts within the Worldwide Virtual Stack Balancer showcase, cloud-based deployment rises as the foremost compelling arrangement for numerous organizations. Cloud-based virtual stack balancers offer unparalleled adaptability, adaptability, and nimbleness, empowering organizations to powerfully alter assets based on fluctuating requests and scale applications universally with ease. With cloud-based arrangement, businesses can offload the burden of framework administration, decrease capital use, and use pay-as-you-go estimating models, coming about in fetched efficiencies and progressed asset utilization. Besides, cloud-based virtual stack balancers give consistent integration with cloud-native designs and administrations, facilitating rapid sending and empowering organizations to saddle the complete potential of cloud computing. As businesses progressively grasp cloud-first methodologies and look to capitalize on the benefits of cloud computing, cloud-based virtual stack balancers develop as crucial components for optimizing application conveyance within the advanced time.

Virtual Load Balancer Market Segmentation: By Vertical

-

IT and Telecom

-

BFSI, Healthcare

-

Retail

-

Government

-

Others

Among the verticals sectioned within the Worldwide Virtual Stack Balancer showcase, the IT and Telecom sector stands out as the foremost critical and compelling fragment. This segment is characterized by high-volume, high-traffic applications, and administrations, requesting strong and adaptable application conveyance arrangements. Virtual stack balancers play an essential part in guaranteeing the ideal execution, accessibility, and security of basic IT and telecom applications, counting websites, versatile apps, VoIP administrations, and gushing stages. With the expanding digitization of businesses and the expansion of associated gadgets, the IT and Telecom segment requires a dexterous, versatile, versatile foundation to meet advancing client requests and competitive weights. Virtual stack balancers offer energetic activity administration, brilliantly load distribution, and consistent failover capabilities, engaging organizations within the IT and Telecom division to convey predominant client encounters, maximize uptime, and remain ahead in today's computerized scene. As this division proceeds to enhance and scale its computerized framework, the request for virtual stack balancers as necessary components for optimizing application conveyance is anticipated to stay strong, making it a key section driving showcase development and development.

Virtual Load Balancer Market Segmentation: By Solution

-

Application load balancing

-

Network load balancing

-

Global server load balancing (GSLB)

-

Software-defined (SDN) load balancing

Among the divisions by arrangement within the Worldwide Virtual Stack Balancer advertise, application load balancing develops as the foremost successful arrangement for numerous organizations. Application stack adjusting centers on dispersing approaching application activity over numerous servers or assets based on predefined calculations and arrangements, guaranteeing ideal execution, accessibility, and unwavering quality of applications. This arrangement is especially advantageous for businesses working with high-traffic, latency-sensitive applications such as e-commerce websites, online keeping money stages, and client relationship administration (CRM) frameworks. Application stack balancers give granular activity administration capabilities, counting SSL end, content-based directing, and session perseverance, permitting organizations to optimize application conveyance and improve client encounters. With the expanding complexity of cutting-edge IT designs and the rise of cloud-native applications, application stack adjusting arrangements offer consistent integration with microservices, containerized situations, and cloud stages, engaging organizations to attain nimbleness, versatility, and flexibility in their application conveyance foundation. As businesses prioritize computerized change activities and look for to provide predominant application encounters to clients, the request for application load balancing arrangements is anticipated to stay solid, driving advertise development and advancement within the Worldwide Virtual Stack Balancer advertise.

Virtual Load Balancer Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East & Africa

The topographical dispersion of the Virtual Stack Balancer showcase grandstands an assorted scene with shifting degrees of showcase share over diverse districts. North America rises as the prevailing locale, capturing a noteworthy parcel of 35%, owing to its progressed mechanical foundation, early appropriation of cloud computing, and expansion of computerized businesses. Europe closely takes after with a considerable share of 30%, driven by the nearness of set-up businesses, exacting administrative benchmarks, and developing speculations in IT framework. Within the Asia-Pacific locale, bookkeeping for 20% of the advertising, quick financial development, advanced change activities, and expanding web infiltration fuel advertise extension. South America and the Center East and African locales contribute 9% and 8% individually, reflecting rising showcase openings and developing speculations in the innovation framework. These insights highlight the worldwide nature of the Virtual Stack Balancer showcase, with openings and challenges shown over differing locales, each contributing extraordinarily to the market's by and large development and improvement.

COVID-19 Impact Analysis on the Global Virtual Load Balancer Market:

The COVID-19 widespread has essentially affected the Worldwide Virtual Stack Balancer showcase, reshaping request elements and quickening certain patterns while showing challenges for advertising players. As businesses around the world moved to inaccessible work courses of action and computerized operations, the request for virtual stack balancers surged to guarantee consistent application conveyance and execution over disseminated situations. Organizations prioritized ventures in cloud foundation, crossover and multi-cloud designs, and edge computing arrangements, driving the selection of virtual stack balancers to optimize application conveyance and bolster further workforce efficiency. Be that as it may, supply chain disturbances, budget limitations, and extended delays posed challenges for showcase players, driving to sending delays and income vulnerabilities. In addition, increased cybersecurity concerns and the requirement for vigorous application security advances underscored the significance of virtual stack balancers in relieving cyber dangers and guaranteeing information assurance. Looking ahead, as economies recuperate and businesses adjust to the modern ordinary, the request for virtual stack balancers is anticipated to stay solid, driven by continuous computerized change activities, cloud selection patterns, and the basic for effective application conveyance arrangements within the post-pandemic time.

Latest Trends/ Developments:

Within the quickly advancing scene of virtual stack adjusting, a few most recent patterns and improvements are reshaping the advertised flow. One outstanding drift is the expanding selection of Kubernetes-native stack adjusting arrangements, driven by the developing ubiquity of containerized applications and microservices models. Kubernetes-native stack balancers offer consistent integration with holder coordination stages, energetic activity administration, and enhanced scalability, catering to the desires of organizations grasping cloud-native innovations and DevOps hones. Moreover, the rise of edge computing and 5G systems is fueling requests for edge stack adjusting arrangements, empowering organizations to disseminate application workloads closer to end-users for decreased idleness and moved forward execution. Besides, the merging of fake insights and machine learning innovations is revolutionizing virtual stack adjusting with clever activity steering, prescient analytics, and mechanized optimization, improving application conveyance effectiveness and flexibility. As organizations proceed to prioritize deftness, versatility, and execution in their advanced change ventures, these latest patterns and advancements are anticipated to shape the long-term direction of the virtual stack adjusting advertising, driving development, and advertising development.

Key Players:

-

F5 Networks, Inc.

-

Citrix Systems, Inc.

-

Radware Ltd.

-

Kemp Technologies, Inc.

-

A10 Networks, Inc.

-

Fortinet, Inc.

-

Barracuda Networks, Inc.

-

NGINX, Inc. (acquired by F5 Networks)

-

Avi Networks (acquired by VMware)

-

HAProxy Technologies, Inc.

-

Array Networks, Inc.

-

Brocade Communications Systems, Inc.