Counter-UAS Systems Market

In 2025, the Global Counter-UAS Systems Market was valued at approximately USD 3,214 million and is projected to reach around USD 8,472 million by 2030, expanding at a CAGR of about 21.4% during 2026–2030.

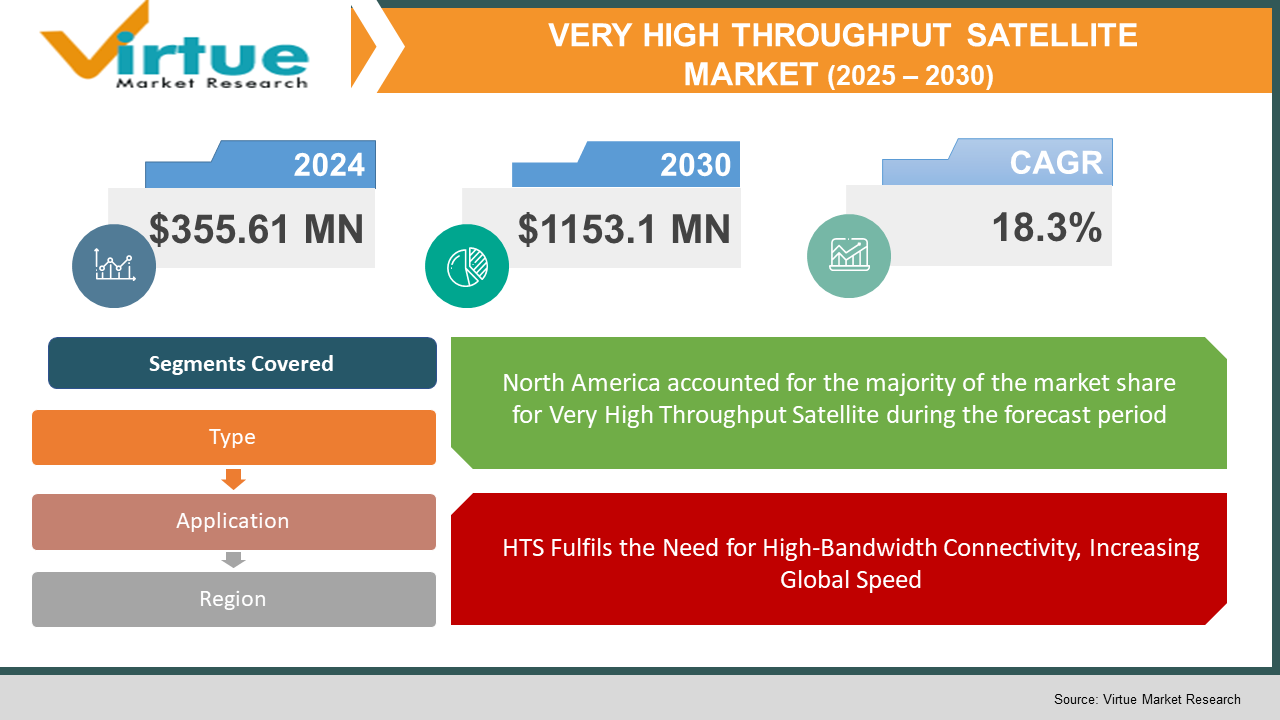

Explore reportThe Global Very High Throughput Satellite Market was valued at USD 355.61 million in 2023 and is projected to reach a market size of USD 1153.1 million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 18.3%.

Spot beams are used by VHS (Very High Throughput Satellite) systems to provide broadband services to end users at bit prices of extra Terabit/s. They are perfect for guiding 5G since they allow more flexibility than VHTS and are successful in accommodating larger demand per beam, more shaped visitor distributions, and dynamic carrier delivery. The excessive degree of frequency reuse and spot beam technology, which permits frequency reusing across several narrowly focused spot beams (typically in the order of thousands of kilometres), as in cell networks, which each characterise technical features of high-throughput satellites, complete the full-size expansion in capability.

Key Market Insights:

According to World Bank research, more than 2.9 billion people do not have access to the internet. HTS technology can close the digital divide by giving underserved and isolated communities access to a dependable and reasonably priced internet connection. A strong and widespread network infrastructure that can handle real-time data needs is promised by the possible integration of HTS with 5G networks and Internet of Things applications. OneWeb hopes to have a constellation of 6,480 satellites, while SpaceX presently has over 2,000 operational satellites in its Starlink constellation. These massive constellations will greatly boost HTS capacity, allowing for greater coverage and possibly reduced consumer data costs. To promote social and economic development, HTS provides an affordable way to close the digital divide in isolated and disadvantaged areas.

Global Very High Throughput Satellite Market Drivers:

HTS Fulfils the Need for High-Bandwidth Connectivity, Increasing Global Speed

The Global Very High Throughput Satellite Market is mostly driven by the growing need for faster internet connections. The increasing use of data-intensive applications such as online gaming, cloud computing, and video streaming has made traditional internet solutions less and less competitive. This is where HTS excels. HTS provides far bigger data capacities and much faster speeds than standard satellite internet. This promotes a more cohesive and effective global community by enabling users to experience the same quality of internet service as those in large cities, even in remote areas. For example, a mining business in a remote region can use HTS to get real-time data from sensors tracking the performance of its equipment. They can optimise operations, reduce downtime, and make data-driven decisions that would be unfeasible with slower traditional satellite internet thanks to this dependable, high-speed connection.

HTS as a Bridge to Equitable Internet Access: Linking the Unconnected.

The difference between people who have access to dependable internet and those who don't is known as the "digital divide." Terrestrial internet infrastructure, such as fibre optic cables, has historically been restricted or non-existent in physically isolated or underserved locations. In many areas, poor connectivity impedes access to vital services, educational opportunities, and economic growth. HTS presents a strong argument by giving a dependable and affordable means of bridging the digital divide. Imagine living in a remote village without consistent internet connectivity. This village's schools can access online educational materials, students may take part in distance learning courses, and medical personnel can access vital medical databases for better patient care because of HTS technology. These communities are empowered by their increased connectedness, which also promotes economic growth and raises citizens' standard of living in general. In these underprivileged places, HTS has the potential to completely transform internet access, resulting in a more just and connected world.

Global Very High Throughput Satellite Market Restraints and Challenges:

Financial limitations and impediments to investing in advanced technologies through IT are among the factors impeding the expansion of the market. Prioritising their own needs assessment is the first thing that organisations wish to consider. Lack of technology is the reason why organisations in developing countries are still trailing those in developed ones. During the forecast period, these factors are impeding the market's growth.

Global Very High Throughput Satellite Market Opportunities:

Numerous aspects are expected to propel the global very high throughput satellite market's huge rise. The growing demand from travellers for in-flight Wi-Fi presents a great potential for HTS to offer high-speed internet access on aircraft. HTS provides a financially viable way to close the digital divide in underserved and isolated locations by providing dependable internet connectivity where traditional infrastructure is missing. Adoption will be accelerated by the introduction of new HTS constellations that offer reduced latency, increased capacity, and greater coverage. Furthermore, the growth of the Internet of Things (IoT) necessitates high-bandwidth, low-latency connections, which HTS can provide to support applications such as asset tracking, remote monitoring, and smart city projects. With even more cutting-edge applications on the horizon, these trends, along with continuing technological developments and improvements in price, offer a promising future for the global very high throughput satellite market.

VERY HIGH THROUGHPUT SATELLITE MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

18.3% |

|

Segments Covered |

By Application, Type, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Airbus Group SE, Eutelsat S.A., Hughes Network Systems, LLC, Inmarsat, Intelsat, Orbital ATK Inc., SES S.A., Space Systems Loral, Thales Group, The Boeing Company |

Payload

Structure

Power System

Altitude Control System

Propulsion System

The payload, structure, power system, attitude control system, and propulsion system segments make up the Very High Throughput Satellite market. Of these, it is anticipated that the Payload Structure will gain market share and maintain its leadership throughout the forecast year. This is because advancements in payload technology have resulted in lower unit costs for elevated deployment for commercial end users, which is expected to boost market growth.

Broadband

Mobility

Enterprise

Government

Cellular Backhaul

Broadcast

A significant CAGR is expected for the broadband phase. This is mostly because network connectivity is becoming more and more in demand. Massive amounts of information need to be transported safely and reliably, and the military and aerospace sectors are two places where broadband is used. Apart from repeaters, these maintain sign energy. Because technology is developing quickly and breakthroughs will be observed in every industry, another section is also anticipated to rise over the projection period.

North America

Asia-Pacific

Europe

South America

Middle East and Africa

The most significant factor driving the global market for very high throughput satellites is the APAC region. The rise in this area can be attributed to important factors including a sizable market size and a high number of nearby participants. However, given the state of the market today, it is expected that the North American region would experience a deregulated telecom sector. It is anticipated that Asia Pacific will see a significant CAGR during the projection period. Particularly responsible for the expansion and contribution of this region are countries such as China and Japan. The regional market is expected to grow over the projected period due to the increased use of satellite antennas in the communications, IT, aerospace, and automobile industries.

COVID-19 Impact Analysis on the Global Very High Throughput Satellite Market:

The global COVID-19 pandemic has caused significant harm to the financial operations of countries across the globe. There have also been effects on the production of small satellite systems, subsystems, and components. While small satellite structures hold great significance, their manufacturing processes have been suspended due to disturbances in the supply chain. Resuming manufacturing activities depends on a few circumstances, including import-export laws, the level of COVID-19 exposure, and the extent to which manufacturing processes are underway. Transportation schedules may no longer be set in stone, even if businesses may still be accepting orders. The release of COVID-19 has resulted in a considerable response in terms of market size growth for Very High Throughput Satellites. This is because of the quarantines, flying bans, and tour limitations, which also led to the temporary closure of all offline activities and workplaces. The offline market was hindered by these factors, and there was a strong desire to adopt digital processes. These problems with the supply chain hurt the Very High Throughput Satellite business. However, because development techniques had been suspended in many locations, use in housing construction had decreased.

Recent Trends and Developments in the Global Very High Throughput Satellite Market:

Recent trends and advancements are driving a dynamic shift in the global very high throughput satellite market. The "constellation boom," in which for-profit businesses like SpaceX and One Web are deploying vast networks of smaller HTS satellites in Low Earth Orbit, is a notable trend. When compared to conventional HTS deployments, these constellations offer a few important benefits, including greater capacity, lower latency, and broader coverage. With developments in strong antennas, enhanced onboard computing, and the use of higher frequencies to enable even faster data transmission speeds, the technological landscape is also changing quickly. Companies are moving in the direction of affordability as they realise the necessity for broader adoption. This involves creating more affordable, smaller user terminals and creative financing schemes to make HTS accessible to customers and companies in underserved or isolated regions.

Key Players:

Airbus Group SE

Eutelsat S.A.

Hughes Network Systems, LLC

Inmarsat

Intelsat

Orbital ATK Inc.

SES S.A.

Space Systems Loral

Thales Group

The Boeing Company

The Global Very High Throughput Satellite Market was valued at USD 355.61 million in 2023 and is projected to reach a market size of USD 1153.1 million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 18.3%.

The worldwide Global Very High Throughput Satellite Market growth is estimated to be 18.3% from 2024 to 2030.

Growing adoption in distant and underserved areas, the advent of new constellations with better capabilities, and the growing demand for in-flight connection are some of the potential future trends and prospects for the global very high throughput satellite market.

There were conflicting effects of the COVID-19 outbreak on the worldwide market for very high throughput satellites. At first, lockdowns and worries about business continuity caused a spike in demand for satellite-based internet access. Long-term growth was, however, impeded by delays in projects and disruptions in the supply chain.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.