Ultrasound Devices Market Size (2024 – 2030)

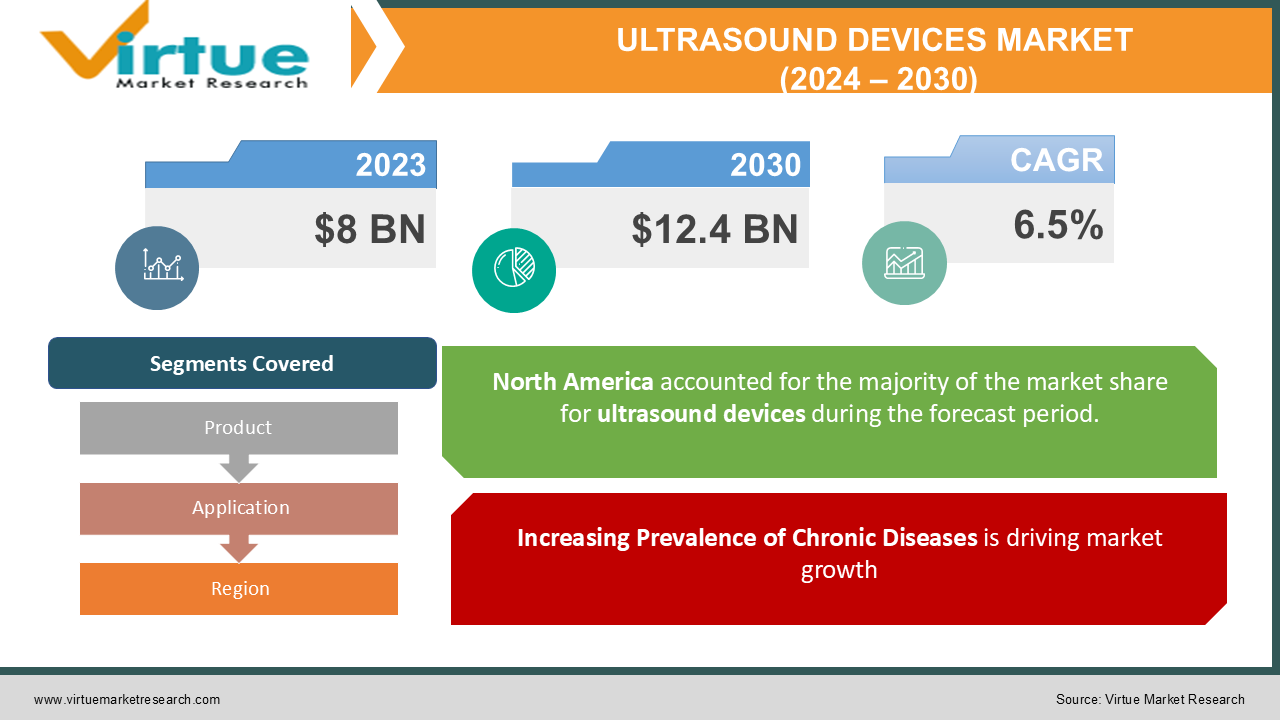

The Global Ultrasound Devices Market was valued at USD 8 billion in 2023 and is projected to grow at a CAGR of 6.5% from 2024 to 2030. The market is expected to reach USD 12.4 billion by 2030.

Ultrasound devices are essential medical instruments that use high-frequency sound waves to create images of organs and structures within the body, aiding in the diagnosis and monitoring of various medical conditions. This market is driven by the increasing prevalence of chronic diseases, a growing aging population, and advancements in ultrasound technology. The rising demand for non-invasive diagnostic procedures further supports market growth, as ultrasound devices are often preferred for their safety, speed, and accuracy compared to other imaging modalities.

Key Market Insights:

-

North America dominated the market, accounting for approximately 40% of the global market share in 2023, driven by advanced healthcare infrastructure and high adoption of new technologies.

-

The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by increasing healthcare expenditure and rising awareness about advanced diagnostic techniques.

-

Portable ultrasound devices are gaining popularity, particularly in emergency and rural healthcare settings, due to their mobility and ease of use.

-

The increase in outpatient procedures and the preference for point-of-care ultrasound are significantly contributing to market growth, enhancing the accessibility of ultrasound imaging.

-

The emergence of AI and machine learning technologies in ultrasound imaging is expected to revolutionize the market, improving diagnostic accuracy and workflow efficiency.

-

Rising investments in healthcare infrastructure, especially in emerging economies, are boosting the adoption of ultrasound devices.

-

The growing trend of telemedicine is also impacting the ultrasound devices market positively, as remote diagnostics and consultations become more prevalent.

Global Ultrasound Devices Market Drivers:

Increasing Prevalence of Chronic Diseases is driving market growth: The major growth driving the ultrasound devices market is the increasing cases of chronic diseases, such as cardiovascular diseases, cancers, and musculoskeletal disorders. Most of these conditions generally require constant observation and imaging of patients for accurate evaluation of diagnosis and treatment decisions, which consequently increases ultrasound imaging demand. Chronic diseases have been found to account for about 71% of the mortality toll worldwide. This means effective diagnostic equipment is badly required to contain the alarming rise of these deaths. The advancement in chronic condition monitoring capability has also made ultrasound gadgets more useful tools in achieving the correct decisions concerning patient care on the part of health experts. Ultrasound imaging does not have to be an invasive process, thereby avoiding discomfort among patients; thus, there are many evaluations that can be performed on the same device, and this makes it highly coveted in the chronic disease management regime. Advancements, for example, in developing portable and handheld ultrasound imaging devices make it accessible to perform imaging in various setting places, including outpatient clinics or even at home. More of the patients will, consequently, be able to acquire timely and accurate diagnoses thereby contributing to the overall ultrasound devices market growth.

Technological Advancements is driving market growth: This market advances at an extremely rapid pace of advancement in ultrasound technology. Advanced classical machines with 3D and 4D ultrasound imaging, elastography, and Doppler ultrasound imaging capabilities add more elaborate details and precision to images. The incorporation of AI and machine learning algorithms into ultrasound devices is revolutionizing the field, and automation of image analysis provides accurate diagnostics. These advances not only benefit the experience of healthcare users but also enhance patient outcomes through early detection of diseases. Additionally, the availability of portable and point-of-care ultrasound equipment has allowed health care professionals to do imaging in any setting-from remote locations to underserved areas. These are mostly battery operated and very compact, increasing accessibility and convenience. Thus, the market for ultrasound devices, all its innovations being developed after technology, is expected to grow in the coming times.

Growing Demand for Non-Invasive Diagnostic Procedures is driving market growth: Rising interest from patients and professionals in health care in non-invasive diagnostic methods is driving the growth of the market for ultrasound devices. Unlike imaging techniques like MRI and CT scan, ultrasounds do not expose patients to ionizing radiation and are, therefore, safe for patients. Minimization of such exposure in those populations is thus very crucial-for instance, pregnant women or children. Not least, the ultrasound technique may be performed more quickly and less expensively than some others, therefore more advantageous in terms of cost, attractiveness to the patient as well as health facilities. In addition, greater awareness concerning advantages of non-invasive diagnosis is likely to gain acceptability to ultrasound diagnostics through regular imaging studies. On another hand, the continuous revolution in technology, not forgetting the invention of new ultrasounds, namely transportable portable and even handheld versions widens access and wider acceptability for use across health establishment in all regions. Growing demands for quicker, safer, and lower-cost diagnostic options will keep ultrasound devices at the threshold of expansion over the next few years.

Global Ultrasound Devices Market Challenges and Restraints:

High Cost of Advanced Ultrasound Equipment is restricting market growth: The greatest hurdle of the ultrasound devices market is that high-end ultrasound machines are quite costly. This means, though technology has evolved a lot and produced an advanced imaging device and many more features, it does not come for free of cost. It creates difficulties for many health care setups as there are fewer budget allocations for many health facilities, especially in developing areas. Another additional cost can be incurred on maintenance and repair as well as the training of medical professionals in handling such highly technical ultrasound equipment. Thus, smaller clinics and rural health facilities might not afford newer ultrasound machines, thereby not utilizing the overall potential of this market. It also means unequal access to advanced ultrasound machines between developed and developing nations, thereby having limited use in areas where there is most need for improved diagnostic capabilities. Such factors have made manufacturers focus on less expensive options and financing so that ultrasound machines can reach a wider segment of health-care providers.

Regulatory and Reimbursement Challenges is restricting market growth: High levels of regulatory and reimbursement problems might be challenging growth prospects for the ultrasound devices market. The approval for introducing a new ultrasound device may take months or years depending on the complexity and standard levels of testing as observed under the health authorities. Furthermore, the policies of reimbursement for ultrasound procedures vary from one region to another and even between different healthcare systems, which influences the willingness of healthcare providers to invest in new technology. In other instances, some applications may not be covered by insurance, which discourages the patients from choosing these services. Such variability can lead to uncertainty for health care providers and manufacturers in planning their finances and making investments in new ultrasound technologies. Stakeholders in the ultrasound devices market, therefore, need to be proactive and advocate for appropriate reimbursement policies that are instituted and sustained while being informed about the regulatory changes that can impact product development and approval processes.

Market Opportunities:

The ultrasound devices market thus comprises of a lot of growth and innovation opportunities. Actually, in this rapidly changing healthcare sector with patient-centricity at its forefront, it may well be concluded that portable or handheld ultrasound devices have turned into the next big opportunity for growth and innovation. This portability does enable point-of-care imaging so that clinicians can effectively conduct ultrasound examinations in emergency departments, primary care offices, or other remote settings. With the growth of telemedicine, integration of portable ultrasound devices within virtual health models holds a unique opportunity for expanding access to diagnostic imaging services for patients in underserved areas. In addition, with innovations in artificial intelligence and machine learning, smarter ultrasound solutions for better diagnostic accuracy, automating image analysis and simplification of workflows are arriving on the scene. Therefore, with healthcare organizations looking for ways to become more efficient and cost-effective, this would increase the demand for the technologically advanced solution. Increased preventive care and early disease detection are also driving the ultrasound devices market as such imaging technologies will find massive applications in identifying health conditions before they are beyond curing. As these emerging trends encourage better research and development, manufacturers stand tremendous opportunities within these emerging trends and introduce next-generation ultrasound devices for healthcare providers and patients. Also, partnerships and collaborations with healthcare institutions can help introduce new technologies and improve market penetration as it relates to enhancing the overall quality of care delivered to patients.

ULTRASOUND DEVICES MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6.5% |

|

Segments Covered

|

By Product, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

GE Healthcare, Philips Healthcare, Siemens Healthineers, Canon Medical Systems, Fujifilm Holdings Corporation, Mindray Medical International Limited, Hitachi, Ltd., Samsung Medison Co., Ltd., Esaote S.p.A, Boston Scientific Corporation

|

Ultrasound Devices Market Segmentation: By Product

The most dominant segment in the by product category is the Diagnostic Ultrasound Devices segment, which accounted for over 70% of the market share in 2023. This dominance is attributed to the widespread use of diagnostic ultrasound in various medical applications, including obstetrics, cardiology, and abdominal imaging. The versatility, safety, and effectiveness of diagnostic ultrasound continue to drive its adoption across healthcare settings.

Ultrasound Devices Market Segmentation: By Application

In the by application category, the Obstetrics and Gynecology segment holds the largest market share, primarily due to the essential role of ultrasound imaging in monitoring pregnancies and assessing female reproductive health. The increasing number of pregnancies worldwide, coupled with the rising awareness of prenatal care, contributes to the segment's growth. Additionally, technological advancements in ultrasound imaging techniques are enhancing the quality of care provided in obstetrics and gynecology.

Ultrasound Devices Market Segmentation: By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

North America is leading with a significant share in the ultrasound devices market and covered about 40% in the year 2023. This position can be accredited to many factors that involve the infrastructure of better health care facilities, high expenses incurred on healthcare, and rapid adoption of latest medical technological applications. Continuous progress of ultrasound technology through extensive research and development supported by well-established healthcare infrastructure in this region supports a strong growth rate for its market. An additional factor is the growing number of patients with chronic diseases and the graying population in North America, which fuels the demand for diagnostic imaging services, such as ultrasound. The availability of well-trained medical professionals and a solid reimbursement framework also boosts the use of ultrasound devices in medical practice. In addition, investments in healthcare technology and infrastructure will serve as a stimulus to growth in the market for ultrasound devices in this region. With healthcare services trending towards more patient-oriented care and effectiveness, the ultrasound devices market in North America would continue to lead the rest of the world.

COVID-19 Impact Analysis on the Ultrasound Devices Market:

The COVID-19 pandemic has had a profound impact on the ultrasound devices market, presenting both challenges and opportunities. During the initial phases of the pandemic, many healthcare facilities experienced disruptions in routine imaging services due to the need to prioritize COVID-19 patients and limit non-urgent procedures. This led to a temporary decline in the demand for ultrasound devices, as elective surgeries and routine diagnostic imaging were postponed. Additionally, supply chain disruptions affected the availability of ultrasound equipment and accessories, creating further challenges for manufacturers and healthcare providers. However, as the healthcare industry adapted to the new normal, there was a notable shift towards telemedicine and remote patient monitoring, which created opportunities for portable ultrasound devices. These devices enabled healthcare providers to perform ultrasound examinations at the point of care, reducing the need for patients to visit hospitals or clinics. The pandemic also highlighted the importance of non-invasive diagnostic procedures, driving the demand for ultrasound imaging in various clinical settings. As healthcare systems continue to recover and adapt to the post-pandemic landscape, the ultrasound devices market is expected to witness a resurgence in demand, particularly for portable and point-of-care solutions that enhance accessibility and patient safety.

Latest Trends/Developments:

The ultrasound devices market is witnessing a number of notable trends and developments that are shaping its future. One of the major trends is the increasing inclusion of artificial intelligence and machine learning technologies in ultrasound imaging systems. Advanced technologies are thereby facilitating automated image analysis, increasing the accuracy of diagnosis, and enhancing workflow efficiency in the clinical field. The ultrasound images can be interpreted with the help of AI algorithms for doctors, thus avoiding human error and leading to quicker diagnoses. Another trend is that of increased demand for portable and handheld ultrasound devices that are convenient and flexible in any healthcare environment. They are most valuable in emergency settings, remote locations, and point-of-care applications, allowing quick and accurate assessments without the need for extensive equipment. The ultrasound devices market is increasingly adopting 3D and 4D imaging technologies, which enable better visualization of anatomical structures and thus an enhanced overall experience of diagnosis. This trend is particularly strong in obstetrics and gynecology where expectant parents look for more detailed insights into fetal development. Preventive healthcare coupled with timely detection of a disease requires the use of more ultrasound for diagnostic purposes. Going forward with this, healthcare provider emphasis toward patient-centered outcomes is forcing the ultrasound device market continuously to evolve within innovation coupled with technology breakthroughs.

Key Players:

-

GE Healthcare

-

Philips Healthcare

-

Siemens Healthineers

-

Canon Medical Systems

-

Fujifilm Holdings Corporation

-

Mindray Medical International Limited

-

Hitachi, Ltd.

-

Samsung Medison Co., Ltd.

-

Esaote S.p.A

-

Boston Scientific Corporation