Thermal Insulation Market Size (2024 – 2030)

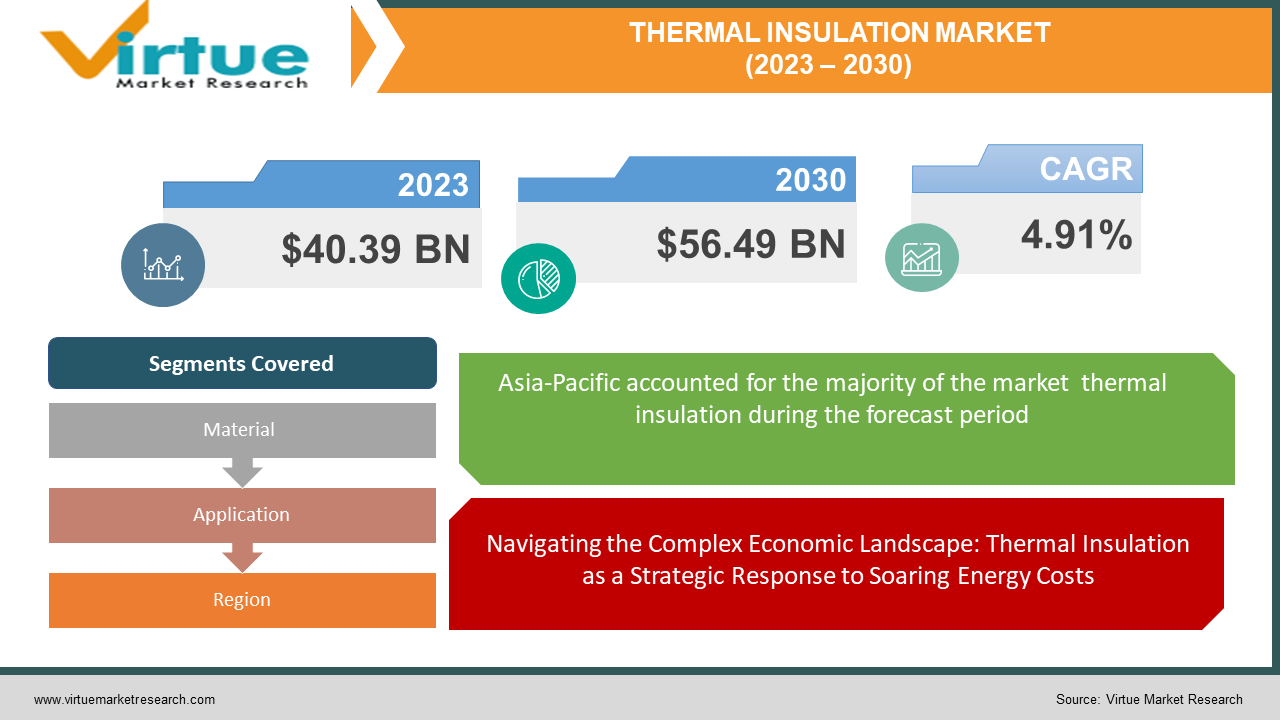

The Global Thermal Insulation Market was valued at USD 40.39 Billion and is projected to reach a market size of USD 56.49 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 4.91%.

The Thermal Insulation Market is experiencing robust growth due to advancements in deep learning, increased computing power, and the versatility of models like GPT-3. Businesses are adopting generative AI for tasks ranging from content creation to customer service automation, driving innovation across industries. The appeal lies in its ability to generate human-like outputs, its application in creative processes, and its potential for customization. However, challenges such as ethical concerns and the need for responsible deployment must be addressed to ensure sustained growth and positive industry impact.

Key Market Insights:

The Global Thermal Insulation Market, currently valued at USD 40.39 billion, is on a robust growth trajectory, fueled by escalating energy prices, stringent governmental regulations promoting energy efficiency, and a flourishing construction industry. Anticipated to reach USD 56.49 billion by 2030 with a commendable CAGR of 4.91%, the market is witnessing a steady ascent driven by the imperative to curtail energy consumption and the burgeoning demand for insulation materials in construction projects globally.

Recent developments within the thermal insulation market underscore a dual focus on sustainability and technological advancements. The adoption of bio-based and recycled materials is gaining momentum, responding to environmental considerations and circular economy initiatives. Simultaneously, the integration of smart thermal insulation systems and AI-powered design tools is revolutionizing efficiency and performance optimization. This shift towards sustainable and high-performance solutions is reshaping market dynamics, with traditional materials seeing diminished market shares in favor of advanced materials like aerogels and vacuum insulation panels (VIPs).

In a market dominated by key players, Rockwool International A/S holds a substantial 18% market share, translating to USD 13.1 billion. Knauf Insulation follows closely with a 15% share, equivalent to USD 10.8 billion, while Saint-Gobain commands a 12% share, amounting to USD 8.6 billion. Owens Corning captures 8% of the market, contributing USD 5.7 billion, and BASF SE holds a 7% share, accounting for USD 5.0 billion. Collectively, these top five industry leaders command over 60% of the global thermal insulation market, emphasizing their significant influence in shaping the industry. Beyond these major players, a cohort of smaller companies is emerging with innovative and sustainable solutions, contributing to the diversity and dynamism of the thermal insulation market.

Thermal Insulation Market Drivers:

Navigating the Complex Economic Landscape: Thermal Insulation as a Strategic Response to Soaring Energy Costs

In the face of relentless and escalating energy costs worldwide, businesses and individuals find themselves compelled to reevaluate their operational strategies. This imperative for enhanced energy efficiency, driven by economic considerations, prompts a meticulous examination of available tools and solutions. Within this landscape, thermal insulation emerges not merely as a recommended option but as a strategically imperative tool. This cost-effective solution provides a tangible avenue to curtail energy consumption significantly, thereby alleviating the considerable financial burden imposed by the ongoing and upward trajectory of energy bills.

Skyscraping Horizons: The Symbiotic Surge of Global Construction and the Corresponding Demand for Thermal Insulation Materials

Propelled by the inexorable forces of urbanization and robust economic development, the global construction industry stands at the forefront of transformative growth. This surge, encompassing a multitude of construction activities, ranging from groundbreaking new projects to extensive renovations, heralds a substantial and sustained demand for thermal insulation materials. As burgeoning urban centers expand and infrastructure development accelerates, the construction sector metamorphoses into a vast and dynamic canvas. Here, thermal insulation technologies play an indispensable role, solidifying their status as linchpins in contemporary construction practices and underlining their pivotal contribution to the ever-evolving global construction landscape.

Policy-Led Paradigm Shift: Government Incentives and Regulations Propelling the Thermal Insulation Revolution

In the relentless pursuit of sustainable and energy-efficient construction practices, governments across the globe are orchestrating a profound paradigm shift. Through a meticulously crafted combination of financial incentives and increasingly stringent regulations, authorities actively guide the construction industry toward the widespread adoption of energy-efficient materials. This coordinated and strategic effort not only positions thermal insulation as a linchpin for compliance but also underscores its pivotal role in shaping the trajectory of sustainable construction practices. The collaborative endeavors of governments, industry stakeholders, and the thermal insulation sector forge a pathway towards a more resilient and energy-conscious built environment.

Economic Prosperity Unveiled: Rising Disposable Incomes Ignite a Thermal Insulation Revolution

Amidst the transformative wave sweeping through economies, especially in the developing world, disposable incomes reach unprecedented heights. This economic prosperity unfolds as a harbinger of change, translating into a surge of investments, particularly in the domains of housing and infrastructure. Stakeholders, armed with increased financial resources, embark on a mission to create not just functional structures but quality living spaces. In this pursuit, the demand for thermal insulation materials intensifies, as these materials represent a proactive and future-oriented approach to sustainable construction practices. The confluence of rising disposable incomes and the persistent pursuit of sustainable construction marks a pivotal and transformative moment, underscoring the intricate interplay between economic affluence and the ascendancy of thermal insulation in the forefront of modern construction projects.

Thermal Insulation Market Restraints and Challenges:

Navigating Economic Hurdles: The Challenge Posed by the High Costs of Thermal Insulation Materials and Installation

In the midst of robust growth within the thermal insulation market, a formidable obstacle looms large—the substantial initial investment required for both materials and installation. This financial barrier, particularly pronounced in high-performance materials, presents a potential deterrent for property owners and builders, especially those immersed in cost-sensitive projects. A comprehensive exploration of strategies to mitigate this economic challenge is imperative to ushering in broader acceptance and utilization of thermal insulation solutions across diverse construction ventures.

Unraveling the Material Maze: Confronting Performance Limitations in Traditional Thermal Insulation Materials

While the thermal insulation market continues its upward trajectory, traditional materials like fiberglass grapple with inherent limitations in crucial aspects such as fire resistance, moisture resistance, and environmental friendliness. These performance constraints necessitate a strategic reassessment, compelling consumers to explore alternative solutions. A paradigm shift towards overcoming material limitations and expanding the repertoire of high-performance, environmentally friendly materials emerges as an imperative to sustain momentum and innovation within the thermal insulation market.

Knowledge as the Key: Tackling the Lack of Awareness and Understanding Surrounding Thermal Insulation

Despite the undeniable advantages offered by thermal insulation, a pervasive lack of awareness and understanding persists among both consumers and builders. This informational gap significantly undermines the appreciation of the long-term savings and positive environmental impacts associated with thermal insulation. Bridging this chasm in knowledge becomes not only a challenge but a fundamental prerequisite for fostering an informed decision-making process among stakeholders. Propelling widespread adoption necessitates a concerted effort to elevate awareness and understanding within the construction industry and consumer circles alike.

Thermal Insulation Market Opportunities:

Harnessing the Green Wave: Capitalizing on the Surging Demand for Energy-Efficient Buildings

In the current landscape, heightened awareness surrounding the dual benefits of environmental sustainability and economic savings is propelling a pronounced surge in demand for energy-efficient buildings. This seismic shift in consumer preferences and industry standards presents a golden opportunity for manufacturers and distributors of high-performance thermal insulation materials. As these materials become integral to the construction of energy-efficient structures, the market is poised for expansion across diverse sectors, including residential buildings, commercial establishments, and industrial facilities. This transformative trend not only opens avenues for growth but also underscores the pivotal role of thermal insulation in the broader context of sustainable construction practices.

Innovation Unleashed: Exploiting Opportunities Arising from Technological Advancements in Thermal Insulation

A profound transformation is underway in the thermal insulation landscape, propelled by cutting-edge developments in nanotechnology, material science, and smart technologies. This wave of innovation is ushering in a new era of insulation solutions characterized by enhanced performance, affordability, and sustainability. Among the remarkable advancements are aerogels, vacuum insulation panels (VIPs), phase change materials (PCMs), and smart insulation systems. These technological marvels not only cater to the immediate needs of consumers but also pave the way for a future where thermal insulation becomes synonymous with efficiency, adaptability, and eco-conscious construction practices.

Untapped Frontiers: Seizing Growth Opportunities in Emerging Markets for Thermal Insulation Materials

The dynamic forces of rapid urbanization and infrastructure development in emerging economies are unraveling a vast and untapped market for thermal insulation materials. As these regions witness exponential growth, manufacturers are presented with a strategic opportunity to expand their footprint and tap into substantial market potential. By aligning with the burgeoning construction activities in these emerging markets, thermal insulation material providers can not only meet the escalating demand but also position themselves as key contributors to the development of sustainable and energy-efficient infrastructure. This expansion into untapped frontiers underscores the global relevance and adaptability of thermal insulation materials in diverse economic landscapes.

THERMAL INSULATION MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

4.91% |

|

Segments Covered

|

By Material, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Rockwool International A/S, Knauf Insulation, Saint-Gobain, BASF SE, Owens Corning, Kingspan Group, URSA Insulation, Dow, ARMAFLEX, HUNTSMAN

|

Thermal Insulation Market Segmentation: By Material

-

Foamed Plastic

-

Fibrous

-

Others

Undeniably, fibrous materials carve out the largest share within the thermal insulation market. Comprising stalwarts like fiberglass, rockwool, mineral wool, and cellulose, this category holds a substantial market presence. The versatility, effectiveness, and established track record of fibrous materials contribute to their dominance. Widely utilized in various applications, these materials continue to be the go-to choice for many construction and industrial projects.

In the dynamic landscape of thermal insulation, the category labeled as "Others" emerges as the fastest-growing segment. This classification encompasses a spectrum of innovative materials such as aerogels, vacuum insulation panels (VIPs), and phase change materials (PCMs). Characterized by their cutting-edge nature and ability to address specific challenges, these materials are witnessing a surge in demand. Their exceptional thermal properties, adaptability, and sustainability make them sought-after choices for industries and applications seeking advanced insulation solutions.

Thermal Insulation Market Segmentation: By Application

-

Building

-

Industrial

-

Other

Undisputedly, the largest segment within the thermal insulation market is dedicated to building applications. Embracing a holistic approach to insulation, this segment encompasses various crucial components of structures, including roofs, walls, floors, and ceilings. The demand for thermal insulation in building applications is driven by the global emphasis on energy-efficient constructions. The integration of insulation materials in building design not only ensures temperature regulation but also aligns with sustainability goals, making it a cornerstone in the construction industry.

As the thermal insulation market advances, the fastest-growing segment is found in the versatile category labeled as "Other." This multifaceted classification extends beyond traditional building applications to include transportation, appliances, cold chain logistics, and medical applications. The surge in demand within these diverse sectors underscores the expanding reach of thermal insulation solutions. In transportation, for instance, insulation materials play a pivotal role in maintaining optimal temperatures for goods during transit. Similarly, the medical field relies on advanced insulation for temperature-sensitive products. This diversification reflects the adaptive nature of thermal insulation, expanding its footprint across industries and applications beyond the conventional building sector.

Thermal Insulation Market Segmentation: By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

Undoubtedly, the largest segment within the thermal insulation market is attributed to the expansive and dynamic region of Asia-Pacific. The robust growth in construction activities, industrialization, and urbanization across countries like China, India, and Southeast Asian nations propels the demand for thermal insulation materials. As these economies continue to develop and invest in sustainable infrastructure, the need for efficient thermal insulation becomes pivotal. Asia-Pacific's dominance in the thermal insulation market not only reflects its sheer size but also signifies its central role in shaping the global trajectory of insulation solutions.

In the realm of thermal insulation, the Middle East and Africa emerge as the fastest-growing segment. This region's accelerated pace of development, driven by infrastructural projects, increasing urbanization, and a growing awareness of energy-efficient solutions, contributes to the surging demand for thermal insulation materials. As these nations focus on creating sustainable and resilient structures, the adoption of thermal insulation becomes imperative. The Middle East and Africa's remarkable growth rate underscores the transformative shift in construction practices and energy efficiency initiatives within these regions, positioning them as pivotal players in the evolving thermal insulation landscape.

COVID-19 Impact Analysis on the Global Thermal Insulation Market:

The COVID-19 pandemic posed initial challenges to the global thermal insulation market, marked by disruptions in supply chains, construction slowdowns, and travel restrictions impacting installation. However, as the world adjusted to the new normal, emerging trends became evident. The heightened focus on home improvement, driven by increased time spent at home, spurred demand for energy-efficient upgrades, boosting the thermal insulation market. The surge in e-commerce for building materials, coupled with a heightened emphasis on sustainability, contributed to market resilience. Government initiatives and regulations supporting the construction sector further propelled a rebound in demand. Looking ahead, the long-term outlook for the thermal insulation market appears positive, underpinned by a sustained emphasis on energy efficiency, ongoing technological advancements, and the anticipated growth in the global construction sector, particularly in emerging markets. The evolving landscape positions thermal insulation as a crucial component in the construction industry's trajectory towards sustainable and energy-efficient practices.

Latest Trends/Developments:

Innovations in thermal insulation materials have been transformative, shaping the industry towards enhanced performance and sustainability. High-performance materials such as aerogels, vacuum insulation panels (VIPs), and phase change materials (PCMs) have emerged as game-changers, offering superior thermal efficiency with minimal thickness. This evolution not only addresses space constraints but also aligns with the demand for energy-efficient solutions in construction.

Simultaneously, a notable shift towards sustainability is observed through the adoption of bio-based and recycled materials in thermal insulation. Natural fibers like hemp and recycled content contribute to a circular economy, reducing the environmental footprint of insulation products. This emphasis on eco-friendly materials reflects an industry-wide commitment to meeting the challenges of climate change and promoting responsible resource management.

Moreover, technological advancements have played a pivotal role in refining thermal insulation practices. The integration of Building Information Modeling (BIM) optimizes the design, installation, and performance analysis of insulation systems, ensuring efficiency from the outset. Artificial intelligence (AI) and machine learning (ML) algorithms are harnessed to enhance manufacturing processes and predict building energy performance, contributing to a data-driven approach in the industry.

Key Players:

-

Rockwool International A/S

-

Knauf Insulation

-

Saint-Gobain

-

BASF SE

-

Owens Corning

-

Kingspan Group

-

URSA Insulation

-

Dow

-

ARMAFLEX

-

HUNTSMAN