Structural Health Monitoring Market Size (2024-2030)

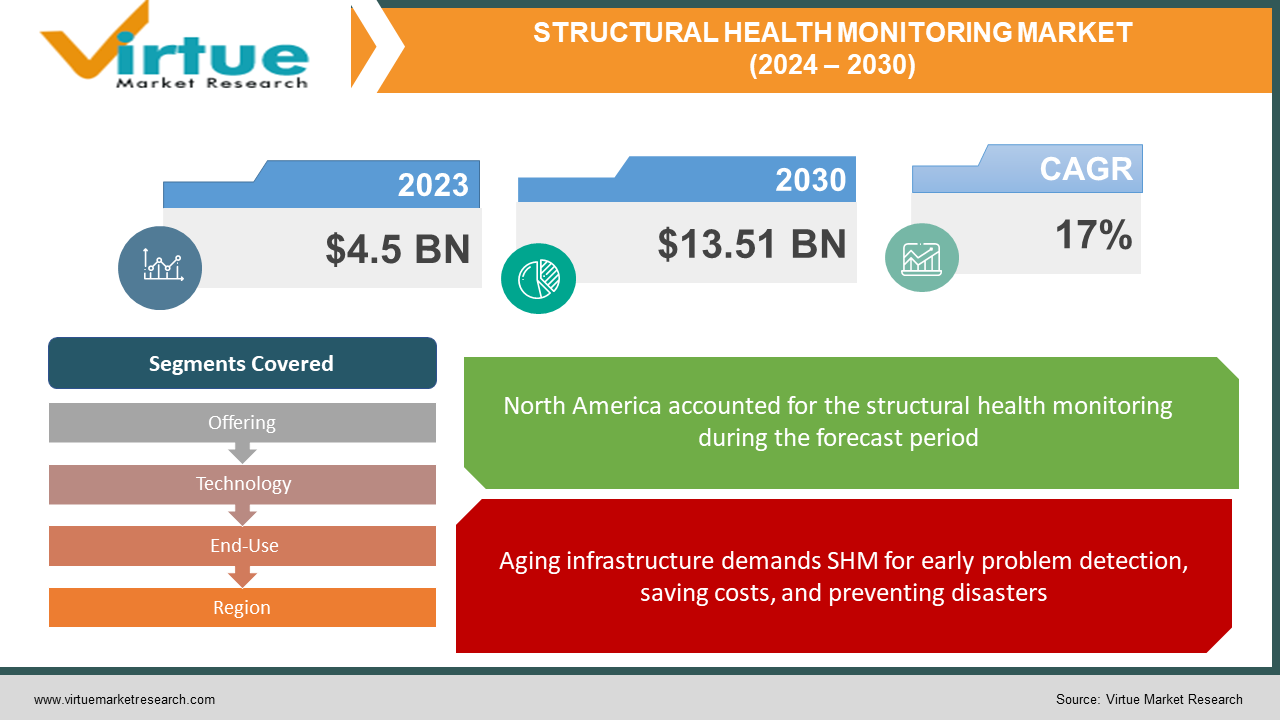

The Structural Health Monitoring Market was valued at USD 4.5 billion in 2023 and is projected to reach a market size of USD 13.51 billion by the end of 2030. Over the cast period of 2024 – 2030, the figure for requests is projected to grow at a CAGR of 17%.

The structural health monitoring (SHM) market is experiencing a surge in growth. This is driven by a pressing need to maintain aging infrastructure like bridges and buildings. Advancements in wireless sensor technology are making SHM systems easier to install and manage, while stricter safety regulations are pushing for their adoption. Additionally, the decreasing cost of sensors makes SHM more accessible. The benefits are clear: early detection of structural issues saves money on repairs, improves safety, and extends the lifespan of structures. The SHM market itself is divided into segments based on what's offered (hardware, software, services), the technology used (wired or wireless), and the industry it serves (civil infrastructure, aerospace, energy, mining).

Key Market Insights:

The structural health monitoring (SHM) market is experiencing a boom driven by the critical need to address our aging infrastructure. Bridges, buildings, and other structures are reaching the end of their lifespan, and SHM offers a proactive approach to maintenance. This translates to early detection of problems, preventing costly repairs and potential disasters. Advancements in wireless sensor technology are making SHM systems easier to use and install. Additionally, the decreasing cost of sensors is making this technology more accessible for a wider range of structures.

Looking beyond cost savings, SHM offers a treasure trove of data. This data allows for data-driven decision-making on maintenance and repairs, optimizing resource allocation. Furthermore, stricter regulations for infrastructure safety are pushing for the adoption of SHM systems. The market itself is segmented to cater to various needs, with offerings like hardware, software, and services, alongside wired and wireless technology options. While civil infrastructure currently dominates the market, the future belongs to wireless SHM due to its convenience and affordability.

The future of SHM is packed with exciting possibilities. The Internet of Things (IoT) will enable remote monitoring of structures, while cloud computing will streamline data management. Most importantly, new sensor technologies promise enhanced accuracy and affordability, making SHM an even more attractive option. Ultimately, SHM offers a win-win for both infrastructure owners and society.

The Structural Health Monitoring Market Drivers:

Aging infrastructure demands SHM for early problem detection, saving costs, and preventing disasters.

A significant portion of the world's infrastructure, like bridges, buildings, and dams, is nearing its twilight year. SHM offers a preventative approach, allowing for early detection of issues that could lead to costly repairs or even catastrophic failures. This translates to significant cost savings and improved public safety.

Advancements in wireless sensor technology make SHM easier to use and install, increasing affordability and reach.

The development of wireless sensor technology is revolutionizing SHM. These sensors are easier and cheaper to install compared to traditional wired systems, making SHM more accessible and cost-effective. Additionally, the decreasing cost of sensors themselves broadens the range of structures that can benefit from SHM.

Stricter regulations for infrastructure safety push for the adoption of SHM systems.

Governments are enacting stricter regulations regarding infrastructure sustainability and public safety. SHM plays a crucial role in ensuring structures comply with these regulations, prompting wider adoption of the technology.

Data from SHM systems allows for data-driven decisions on maintenance, and optimizing resource allocation.

SHM systems provide real-time data on the health of a structure. This valuable information empowers infrastructure owners to make data-driven decisions regarding maintenance and repairs, optimizing resource allocation, and ensuring the longevity of their assets.

The Structural Health Monitoring Market Restraints and Challenges:

Despite the promising growth of the structural health monitoring (SHM) market, some challenges need to be addressed. A major restraint is the upfront cost of installation and ongoing monitoring. While sensor costs are decreasing, implementing, and maintaining SHM systems can still be a significant financial burden, particularly for smaller structures or those with limited budgets. Additionally, a skilled workforce is needed to interpret the data collected by SHM systems. A lack of qualified professionals can hinder the effective utilization of SHM and limit its wider adoption.

Security concerns also pose a challenge. Since SHM systems rely on data transmission, they are vulnerable to cyberattacks. Malicious actors could potentially tamper with data or disrupt monitoring systems, jeopardizing the integrity of the collected information, and potentially compromising structural safety.

Finally, harsh environmental conditions can present practical limitations. Extreme temperatures, dust, or moisture can damage sensors or interfere with data transmission, hindering the effectiveness of SHM systems in certain environments. Addressing these challenges through innovative sensor design, improved data security measures, and workforce training will be crucial for the continued growth and widespread adoption of SHM technology.

The Structural Health Monitoring Market Opportunities:

The structural health monitoring (SHM) market presents a vibrant landscape brimming with opportunities for innovation and growth. Integration with the Internet of Things (IoT) stands as a pivotal force, enabling seamless remote monitoring of structures. This translates to real-time data collection and analysis from any location, empowering faster response times to potential issues and fostering a proactive approach to infrastructure management. Furthermore, advancements in sensor technology offer a glimpse into a future where enhanced capabilities unlock new possibilities. Imagine sensors with improved accuracy, capable of detecting even the subtlest structural changes. Imagine durable sensors that can withstand harsh environmental conditions, extending the reach of SHM to previously inaccessible environments. These advancements will undoubtedly revolutionize the field, expanding the range of applications and environments where SHM can be effectively deployed.

Finally, as SHM technology sheds its cost barrier and becomes more user-friendly, its application can extend far beyond traditional civil infrastructure. Imagine a future where SHM safeguards not just bridges and buildings, but also residential structures, transportation networks, and even historical landmarks. This opens doors to entirely new market segments, fostering a more comprehensive approach to structural health and safety. By capitalizing on these opportunities, the SHM market has the potential to not only ensure the safety and reliability of our infrastructure but also usher in an era of efficient, sustainable, and data-driven management of our built environment.

STRUCTURAL HEALTH MONITORING MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

17% |

|

Segments Covered

|

By Offering, Technology, End-Use, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Honeywell International Inc., Siemens AG, Parker Hannifin Corporation, National Instruments Corporation, GE Aviation, Nova Metrix (UK) Limited, Geokon, Campbell Scientific Inc., COWI, Geocomp

|

Structural Health Monitoring Market Segmentation: By Offering

-

Hardware

-

Software

-

Services

Within the 'By Offering' segment of the structural health monitoring market, hardware currently holds the dominant position. This is due to the crucial role of sensors and data acquisition systems in collecting vital structural data. However, the segment experiencing the fastest growth is wireless technology. The ease of installation and lower costs associated with wireless SHM systems are making them increasingly attractive, paving the way for wider market adoption.

Structural Health Monitoring Market Segmentation: By Technology

In the technology sector of the structural health monitoring market, wired systems are currently the most dominant segment due to their reliable data transmission over long distances. However, wireless technology is expected to be the fastest-growing segment owing to its ease of installation and lower costs. This makes wireless SHM systems more attractive, particularly for applications where ease of use and cost-effectiveness are key considerations.

Structural Health Monitoring Market Segmentation: By End-Use

-

Civil Infrastructure

-

Aerospace & Defense

-

Energy

-

Mining

The civil infrastructure segment reigns supreme in the structural health monitoring market, encompassing bridges, buildings, and dams. This focus on aging infrastructure plays a critical role in ensuring public safety. However, the wireless technology segment is experiencing the most explosive growth. Wireless SHM systems are gaining significant traction due to their ease of installation and lower costs compared to traditional wired systems.

Structural Health Monitoring Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

North America: Currently holding the top spot, North America boasts a well-established SHM market fueled by several factors. Stringent safety regulations, a culture of embracing advanced technologies, and a vast network of aging infrastructure all contribute to the high demand for SHM solutions. The need to address these aging structures presents a significant opportunity for the SHM market to flourish in North America.

Europe: A seasoned player in the SHM arena, Europe prioritizes safety and sustainability in infrastructure management. This focus is further bolstered by government initiatives that promote these aspects. With a well-developed infrastructure base and a strong emphasis on responsible practices, Europe represents a mature market for SHM with continued growth potential.

Asia-Pacific: Buckle up for the fastest growth trajectory! The Asia-Pacific region is poised for explosive expansion in the SHM market. This is driven by a confluence of factors: rapid urbanization leading to a surge in infrastructure development, massive government investments in SHM technology, and a growing awareness of its benefits. China, Japan, and India are the frontrunners in this region, spearheading the adoption of SHM for their rapidly evolving infrastructure landscape.

South America: While still in its early stages, the SHM market in South America is on the rise. Growing awareness of the advantages of SHM, coupled with increasing investments in infrastructure development, paints a promising picture for future growth. As the understanding of SHM's value proposition expands, South America presents an exciting emerging market with significant potential.

Middle East and Africa: Similar to South America, the SHM market in the Middle East and Africa is still evolving. However, the economic growth in these regions, coupled with a growing focus on infrastructure development, is expected to propel the adoption of SHM technology in the coming years. As these regions prioritize advancements in infrastructure, SHM offers a valuable tool for ensuring the safety and longevity of their structures.

COVID-19 Impact Analysis on the Structural Health Monitoring Market:

The COVID-19 pandemic undeniably left its mark on the structural health monitoring (SHM) market. Lockdowns and restrictions disrupted construction projects, causing delays in implementing new SHM systems, particularly for civil infrastructure. Supply chain disruptions also created shortages of key components, hindering production and installation. Budgetary tightening due to the economic downturn might have led to postponements or cancellations of planned projects, impacting short-term market growth.

However, the pandemic also presented some unforeseen opportunities. The renewed focus on infrastructure resilience during the pandemic could drive the long-term adoption of SHM for existing structures, as a preventive maintenance strategy. Social distancing measures highlighted the importance of remote monitoring capabilities, potentially increasing demand for wireless SHM solutions. The pandemic's emphasis on public safety might also lead to stricter regulations and government initiatives promoting SHM for critical structures, further boosting market growth.

In conclusion, while the initial shock of COVID-19 caused a temporary setback, the long-term outlook for the SHM market remains positive. As the global economy recovers and infrastructure resilience becomes a priority, the demand for SHM solutions is expected to rebound. The pandemic's emphasis on remote monitoring and safety regulations presents exciting new opportunities for the SHM market to evolve and meet the ever-changing needs of the infrastructure sector.

Latest Trends/ Developments:

The structural health monitoring (SHM) market is on a roll, constantly innovating and pushing the boundaries. One of the hottest trends is the marriage of SHM with artificial intelligence (AI) and machine learning (ML). By analyzing sensor data in real time, these powerful tools can identify trends, predict potential failures, and even recommend preventative measures. This allows for a proactive approach to infrastructure maintenance, preventing problems before they snowball. Another exciting development is the concept of digital twins. Imagine a virtual replica of a real structure, constantly updated with real-time monitoring data. This digital twin allows engineers to simulate various scenarios and predict how the structure would respond to different stresses.

Furthermore, SHM is shaking hands with the Internet of Things (IoT), enabling remote monitoring of structures from anywhere in the world. This translates to faster response times to potential issues and facilitates data collection from geographically dispersed structures. The focus on sustainability is another exciting trend. By optimizing maintenance schedules and extending the lifespan of structures, SHM reduces the need for new construction, minimizing the environmental impact associated with construction activities.

In conclusion, the future of SHM is bright. With the integration of AI, advanced sensors, and the IoT, SHM systems will become more intelligent, predictive, and efficient. This technological revolution will undoubtedly transform the way we monitor and maintain our infrastructure, ensuring a safer and more sustainable built environment for the future.

Key Players:

-

Honeywell International Inc.

-

Siemens AG

-

Parker Hannifin Corporation

-

National Instruments Corporation

-

GE Aviation

-

Nova Metrix (UK) Limited

-

Geokon

-

Campbell Scientific Inc.

-

COWI

-

Geocomp