Solar Backsheet Market Size (2025 – 2030)

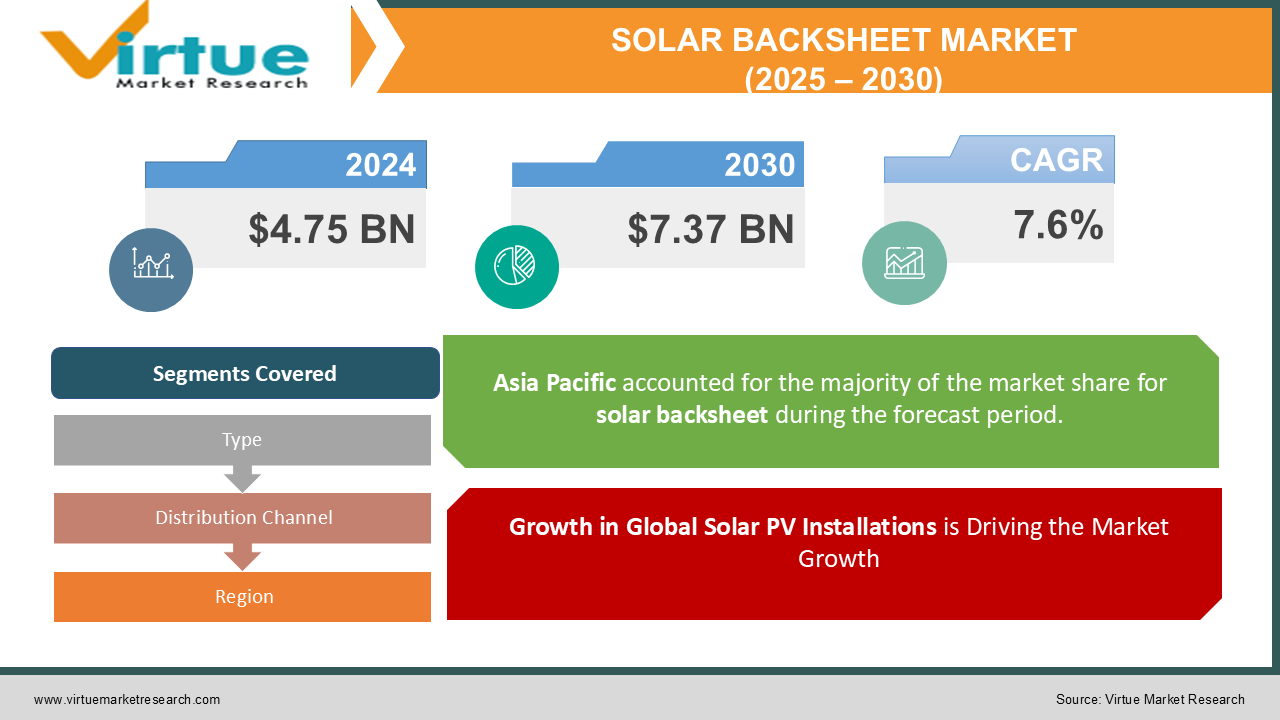

The Solar Backsheet Market was valued at USD 4.75 Billion in 2024 and is projected to reach a market size of USD 7.37 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 7.6%.

The solar backsheet market is a crucial component of the photovoltaic (PV) industry. Solar backsheets are protective layers located on the rear side of solar panels, providing electrical insulation, mechanical protection, and resistance against environmental factors such as moisture, UV radiation, and temperature fluctuations. These backsheets play a vital role in ensuring the long-term performance, reliability, and durability of solar panels, ultimately impacting their energy output and return on investment. The market for solar backsheets is intrinsically linked to the growth of the global solar energy industry, driven by increasing demand for renewable energy sources, government incentives, and decreasing solar energy costs. The market has witnessed significant advancements in backsheet materials and technologies, with a shift towards more durable, high-performance, and cost-effective solutions. The market caters to a diverse range of solar panel manufacturers and installers, with varying requirements for backsheet performance and specifications. The market is characterized by a mix of established material suppliers, specialized backsheet manufacturers, and vertically integrated solar panel manufacturers. The market is also influenced by trends in solar panel technology, such as the increasing adoption of bifacial solar panels, which require specialized backsheet designs. The growing focus on sustainability and recyclability in the solar industry is also impacting the backsheet market, driving demand for more eco-friendly materials and manufacturing processes. The solar backsheet market is a critical enabler of the widespread adoption of solar energy, contributing to a cleaner and more sustainable energy future.

Key Market Insights:

-

65% of solar backsheets utilized fluoropolymer-based materials for enhanced durability.

-

Non-fluoropolymer backsheets accounted for 35% of the total production.

-

Utility-scale installations dominated the market, comprising 58% of the total demand.

-

Residential solar installations contributed to 27% of the backsheet demand.

-

Commercial applications accounted for the remaining 15% of market demand.

-

The average lifespan of backsheets reached 25–30 years, enhancing PV panel durability.

-

Over 72% of manufacturers incorporated recyclable materials in backsheet production.

-

Smart solar panels drove 18% of the demand for advanced backsheets.

-

Anti-reflective coatings were included in 42% of backsheets for efficiency improvement.

-

The market saw a 9% increase in backsheet production compared to 2022.

-

Polyvinyl fluoride (PVF) was the primary material in 47% of backsheets.

-

Ethylene vinyl acetate (EVA) usage grew by 11% in 2023.

-

Monocrystalline solar panels utilized 60% of the backsheets produced.

-

Polycrystalline panels accounted for 35% of backsheet consumption.

-

Thin-film panels used the remaining 5% of backsheets.

-

Over 800,000 tons of polymer materials were utilized in backsheet manufacturing.

-

Asia-Pacific accounted for 56% of global backsheet production.

-

More than 65% of solar panel manufacturers partnered with backsheet suppliers in 2023.

-

The average cost of solar backsheets decreased by 7% compared to 2022.

Market Drivers:

Growth in Global Solar PV Installations is Driving the Market Growth:

The increasing global demand for renewable energy sources, driven by concerns about climate change and energy security, is a major driver for the solar backsheet market. The declining cost of solar energy has made it increasingly competitive with traditional energy sources, leading to rapid growth in solar PV installations worldwide. Government policies, incentives, and targets for renewable energy adoption further accelerate market growth. The increasing awareness of the environmental benefits of solar energy also contributes to market demand. The development of new solar panel technologies and applications further expands the market for solar backsheets. The increasing investment in solar energy infrastructure globally further drives the market for backsheet materials.

Increasing Focus on Solar Panel Durability and Reliability:

The long-term performance and reliability of solar panels are critical factors for their widespread adoption. Solar backsheets play a crucial role in ensuring the durability and longevity of solar panels by protecting them from harsh environmental conditions. The increasing demand for high-performance and long-lasting solar panels is driving innovation in backsheet materials and technologies. The desire to minimize maintenance costs and maximize energy output over the lifespan of solar panels further contributes to the market's growth. The development of advanced testing methods and quality control standards for backsheets also drives market demand. The increasing focus on reducing the levelized cost of energy (LCOE) of solar power further emphasizes the importance of backsheet durability and reliability.

Market Restraints and Challenges:

The solar industry is characterized by intense price pressure and cost competition, which impacts the solar backsheet market. Solar panel manufacturers are constantly seeking to reduce costs across their supply chain, including backsheet materials. This price pressure can squeeze profit margins for backsheet manufacturers and limit investment in research and development. The availability of low-cost backsheet options from emerging markets further intensifies price competition. The need to balance cost-effectiveness with performance and durability is a key challenge for backsheet manufacturers. Solar backsheets must meet stringent technical requirements to ensure long-term performance and reliability in harsh environmental conditions. Challenges include resistance to UV radiation, moisture penetration, temperature fluctuations, and mechanical stress. Developing backsheets that can withstand these challenges while remaining cost-effective is a significant technical hurdle. The increasing adoption of new solar panel technologies, such as bifacial panels and flexible panels, also presents new technical challenges for backsheet manufacturers. The need for continuous innovation and improvement in backsheet materials and manufacturing processes is crucial for addressing these technical challenges.

Market Opportunities:

There are significant opportunities for developing advanced backsheet materials with improved performance characteristics, such as enhanced UV resistance, higher reflectivity, and better thermal management. These advanced materials can improve the efficiency and durability of solar panels, creating new market opportunities. The development of more sustainable and recyclable backsheet materials also presents a significant opportunity. The use of nanotechnology and other advanced technologies can further enhance backsheet performance. The increasing adoption of bifacial solar panels, which generate electricity from both sides, is creating new market opportunities for specialized backsheet designs. Transparent or highly reflective backsheets are required for bifacial panels to maximize energy generation. The development of cost-effective and high-performance backsheets for bifacial panels is a key area of focus for backsheet manufacturers. The increasing deployment of bifacial solar panels in utility-scale projects further drives the demand for specialized backsheets.

SOLAR BACKSHEET MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

7.6% |

|

Segments Covered

|

By Type, Distribution Channel and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Toray Industries, DuPont, Honeywell, Toyo Aluminium K.K., Jolywood, CNBM, SFC, SKC Haas, Innovolt, Dunmore Corporation, Mitsubishi Chemical Corporation, Arkema, Covestro, 3M, Hanwha Advanced Materials

|

Solar Backsheet Market Segmentation: by Type

-

Fluoropolymer Backsheets

-

PET Backsheets

-

Composite Backsheets

-

Glass Backsheets

Most Dominant Type: Fluoropolymer backsheets are currently the most dominant type due to their superior performance and long-term reliability.

Fastest-Growing Type: Transparent backsheets for bifacial solar panels are experiencing rapid growth due to the increasing adoption of this technology.

Solar Backsheet Market Segmentation: by Distribution Channel

-

Direct Sales

-

Distributors

-

Online Platforms

Most Dominant Distribution Channel: Direct sales are the most dominant channel due to the large volumes of backsheets purchased by major solar panel manufacturers.

Fastest-Growing Distribution Channel: Online platforms and e-commerce are gradually increasing in importance, particularly for smaller customers and for accessing specialized backsheet types.

Solar Backsheet Market Segmentation: by Regional Analysis

-

North America

-

Europe

-

Asia Pacific

-

South America

-

Middle East and Africa

Most Dominant Region: The Asia Pacific region is the most dominant region due to its large-scale solar panel manufacturing capacity and high deployment rates.

Fastest-Growing Region: The Asia Pacific region is also the fastest-growing due to ongoing government support, increasing energy demand, and declining solar energy costs. The Asia Pacific region is the largest and fastest-growing market for solar energy, driven by rapid economic growth, increasing energy demand, and government initiatives promoting solar power.

COVID-19 Impact Analysis on the Market:

The COVID-19 pandemic had a mixed impact on the solar backsheet market. Initially, lockdowns and supply chain disruptions caused delays in manufacturing and project installations. However, as economies recovered and governments focused on green recovery initiatives, the solar industry rebounded strongly. The pandemic also highlighted the importance of energy security and resilience, which further contributed to the demand for renewable energy sources like solar. The increasing focus on sustainability and climate change mitigation also accelerated the adoption of solar energy. As the world transitions towards a cleaner energy future, the solar backsheet market is expected to continue its growth trajectory. The pandemic has also emphasized the importance of supply chain diversification and resilience, which has prompted some solar panel manufacturers to consider diversifying their backsheet suppliers.

Latest Trends and Developments:

The integration of sensors and other technologies into backsheets to monitor panel performance and detect potential issues is an emerging trend. There is a growing emphasis on developing recyclable and biodegradable backsheets to reduce environmental impact and promote a circular economy in the solar industry. Ongoing research and development are focused on enhancing the weatherability, UV resistance, and overall durability of backsheets to extend the lifespan of solar panels. Manufacturers are continuously working to reduce the cost of backsheets while improving their performance and efficiency. The use of new materials, such as polyolefins and other advanced polymers, and innovative manufacturing processes are driving innovation in the backsheet market.

Key Players in the Market:

-

Toray Industries

-

DuPont

-

Honeywell

-

Toyo Aluminium K.K.

-

Jolywood

-

CNBM

-

SFC

-

SKC Haas

-

Innovolt

-

Dunmore Corporation

-

Mitsubishi Chemical Corporation

-

Arkema

-

Covestro

-

3M

-

Hanwha Advanced Materials