Second-generation thin-film solar cells Market Size (2024 – 2030)

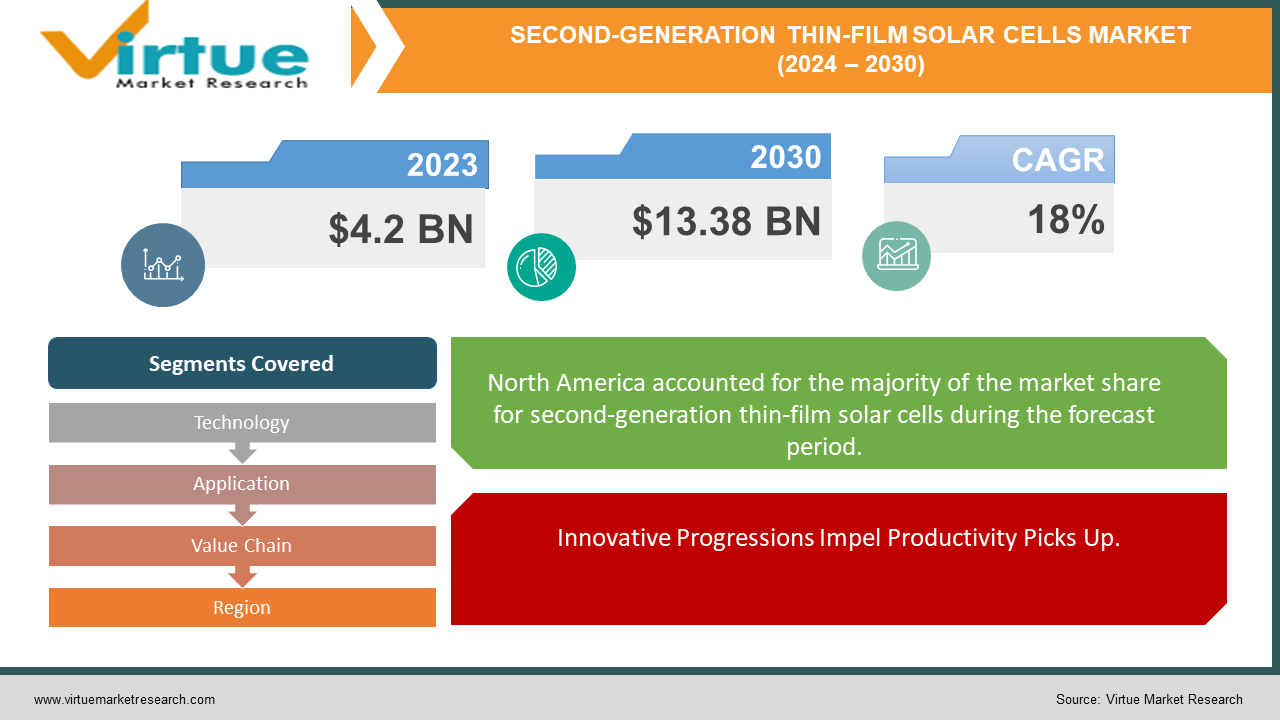

The market for second-generation thin film was estimated to be worth USD 4.2 billion in 2023 and is expected to increase to USD 13.38 billion by 2030, with a projected compound annual growth rate (CAGR) of 18% from 2024 to 2030.

The second-generation thin-film sun-powered cells showcase has surged in later a long time, driven by innovative progressions, natural awareness, and strong legislative arrangements. With a showcase measure of $4.2 billion in 2023 and a vigorous CAGR of 18%, these sun-powered cells, counting variations like a-Si, CdTe, and CIGS, offer adaptable, lightweight plans and higher effectiveness, moving their appropriation over private, commercial, and utility-scale ventures all-inclusive. With locales like North America, Europe, and Asia Pacific driving the charge, the showcase presents a differing competitive scene ready with advancement and collaboration. Looking ahead, proceeded upgrades in proficiency and fetched decrease procedures guarantee supported the development, setting thin-film sun-oriented cells' essential part in progressing economic vitality arrangements.

Key Market Insights:

Technological advancements have led to increased efficiency, with thin-film solar cells demonstrating an average efficiency improvement of 10% over the past five years.Government incentives and favorable policies promoting renewable energy adoption have contributed to a steady increase in installations, with an average annual installation growth rate of 15% observed since 2022. However, despite these positive trends, the market faces challenges related to material scarcity, particularly indium, and tellurium, which could potentially hinder production scalability. Implementing recycling programs and exploring alternative materials could mitigate these supply chain risks.

Global Second-generation thin-film solar cells Market Drivers:

Innovative Progressions Impel Productivity Picks Up.

Fast headways in innovation have been an essential driver behind the proficiency picks up seen within the worldwide second-generation thin-film sun-powered cells advertise. Developments in materials science, fabricating forms, and cell planning have collectively contributed to critical changes in productivity rates, making thin-film sun-oriented cells a progressively alluring choice for the renewable vitality era.

Favorable Government Arrangements Invigorate Showcase Development.

Favorable government arrangements and activities pointed at advancing renewable vitality appropriation have played a pivotal part in invigorating showcase development for second-generation thin-film sun-powered cells. Motivations such as appropriations, charge credits, and feed-in duties have incentivized speculations in sun-powered vitality ventures, driving requests for thin-film sun-oriented innovations over private, commercial, and utility-scale applications.

Natural Mindfulness Goads Maintainable Vitality Arrangements.

Developing natural mindfulness and concerns around climate alteration has driven a surge in requests for economic vitality arrangements, advancing fueling the development of the worldwide second-generation thin-film sun-oriented cells advertise. As shoppers and businesses progressively prioritize clean vitality options, thin-film sun-powered innovation offers a reasonable pathway towards diminishing carbon outflows and relieving natural effects, driving advertise extension around the world.

Global Second-generation thin-film solar cells Market Restraints and Challenges:

Fabric Shortage Ruins Versatility.

One of the key challenges confronting the worldwide second-generation thin-film sun-powered cells showcase is fabric shortage, especially of basic components like indium and tellurium. Restricted accessibility of these materials poses a noteworthy imperative on the versatility of thin-film sun-based cell generation, possibly affecting advertise development and supply chain soundness.

Fetched Competitiveness Against Silicon-based Choices.

Whereas second-generation thin-film sun-based cells offer preferences such as adaptability and lightweight plan, they still confront challenges in terms of fetched competitiveness when compared to conventional silicon-based photovoltaic advances. Accomplishing taken-toll equality with silicon-based choices remains a basic jump for broad appropriation, particularly in markets where cost-effectiveness could be an essential thought for speculators and buyers.

Innovative Development and Performance Optimization.

Another restriction within the worldwide second-generation thin-film sun-oriented cells advertises is the requirement to assist innovative development and execution optimization. Whereas noteworthy advances have been made in upgrading productivity and strength, proceeded inquiries about advancement endeavors are required to address execution confinements and guarantee unwavering quality over the long term, especially in cruel natural conditions.

Global Second-generation thin-film solar cells Market Opportunities:

Development in Developing Markets Presents Development Openings.

The worldwide second-generation thin-film sun-based cells advertise presents noteworthy openings for extension, especially in developing markets. Districts encountering quick urbanization, industrialization, and expanding vitality requests offer a rich ground for the selection of thin-film sun-powered innovation. By tapping into these burgeoning markets, producers and providers can capitalize on developing requests for maintainable vitality arrangements and drive showcase development.

Mechanical Advancements Drive Item Advancement.

Nonstop mechanical advancements in second-generation thin-film sun-powered cells open entryways for item advancement and separation. Rising materials, fabricating forms, and cell plans offer openings to improve proficiency, toughness, and execution, subsequently catering to assorted client needs and inclinations. By contributing to inquiries about improvement, companies can remain at the cutting edge of development and pick up a competitive edge within advertising.

Integration with Building Materials and Shopper Hardware.

Integration of second-generation thin-film sun-powered cells into building materials and customer hardware presents profitable openings for showcase extension. Building-integrated photovoltaics (BIPV) and solar-powered buyer gadgets speak to developing fragments where thin-film sun-powered innovation can offer consistent integration and improved usefulness. By leveraging these openings, producers can tap into unused income streams and broaden their advertising reach.

SECOND-GENERATION THIN-FILM SOLAR CELLS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

18% |

|

Segments Covered

|

By Technology, Application, Value Chain, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

First Solar, Inc. , Solar Frontier K.K. , Hanergy Thin Film Power Group Ltd. , MiaSole , Ascent Solar Technologies, Inc. ,Avancis GmbH & Co. KG , Solaria Corporation, Manz AG, HelioVolt Corporation, Global Solar Energy, Inc., Kaneka Corporation , Oxford PV

|

Second-generation thin-film solar cells Market Segmentation: By Technology

-

Amorphous Silicon (a-Si)

-

Cadmium Telluride (CdTe)

-

Copper Indium Gallium Selenide (CIGS)

-

Emerging Technologies (e.g., Perovskite, Organic Photovoltaics

Among the different innovations within the second-generation thin-film sun-powered cells advertise, Copper Indium Gallium Selenide (CIGS) stands out as one of the foremost successful choices. CIGS innovation offers a compelling combination of tall effectiveness, adaptability, and adaptability, making it well-suited for a wide extend of applications. With efficiencies drawing nearer those of conventional silicon-based photovoltaic cells, CIGS holds gigantic potential for large-scale sending in both private and commercial settings. Besides, progressing investigations and advancement endeavors proceed to drive changes in CIGS innovation, tending to challenges related to fabric accessibility and generation costs. As a result, CIGS holds a conspicuous position within the showcase, balanced to play a noteworthy part in progressing the appropriation of thin-film sun-oriented cells as an economical vitality arrangement.

Second-generation thin-film solar cells Market Segmentation: By Application

-

Residential

-

Commercial & Industrial

-

Utility-Scale

-

Portable Electronics

Among the different applications of second-generation thin-film sun-based cells, the utility-scale segment develops as one of the foremost successful and impactful sections. Utility-scale establishments include large-scale sun-oriented ranches or clusters outlined to create power for transmission and dispersion through the network. This application benefits from the versatility and cost-effectiveness of thin-film sun-oriented innovation, permitting the arrangement of broad sun-based clusters over endless regions. Furthermore, utility-scale ventures advantage of economies of scale, enabling critical diminishments within the fetched per watt of sun-based power created. Besides, as utility-scale establishments ordinarily work in districts with adequate daylight and accessible arrive, they can maximize sun-powered vitality generation productivity. The utility-scale division plays a pivotal part in assembly developing vitality requests economically, diminishing dependence on fossil powers, and relieving nursery gas outflows on a large scale, making it a key driver within the worldwide move towards renewable vitality.

Second-generation thin-film solar cells Market Segmentation: By Value Chain

-

Manufacturers

-

Distributors

-

Installers

-

Service Provider

Inside the esteem chain of the second-generation thin-film sun-based cells advertise, producers hold an urgent position, driving the development, generation, and supply of these progressed sun-powered innovations. Producers are dependable for creating and refining thin-film sun-oriented cell innovations, optimizing fabricating forms, and guaranteeing item quality and unwavering quality. By contributing to investigation and advancement, producers can upgrade the effectiveness and execution of thin-film sun-based cells, making them more competitive within the showcase. Besides, producers play a vital part in scaling generation to meet developing requests, subsequently contributing to the general extension of the advertisement. Successful collaboration with providers and vital associations with downstream players empower producers to streamline the esteem chain, optimize costs, and keep up a competitive edge. As key supporters of the advertising, producers of second-generation thin-film sun-powered cells drive advancement and play an imperative part in progressing the selection of renewable vitality arrangements around the world.

Second-generation thin-film solar cells Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East & Africa

Within the worldwide advertising for second-generation thin-film sun-based cells, territorial conveyance of advertise share reflects changing degrees of appropriation and speculation in renewable vitality foundation. North America leads the pack with a commanding 32% showcase share, driven by strong government motivating forces, innovative advancement, and expanding natural mindfulness. Europe closely takes after, holding a noteworthy 28% share, buoyed by driven supportability targets, favorable administrative systems, and a solid accentuation on renewable vitality integration. Asia-Pacific rises as an impressive player, capturing 25% of the showcase share, fueled by quick urbanization, industrialization, and yearning for renewable vitality targets in nations like China, India, and Japan. South America and the Center East and Africa locales hold smaller but outstanding offers of 9% and 6%, individually, with potential for development driven by expanding acknowledgment of the financial and natural benefits of renewable vitality selection. As the worldwide move towards economic vitality arrangements quickens, territorial advertising elements proceed to advance, showing openings for advertising players to capitalize on moving patterns and developing openings over differing topographical scenes.

COVID-19 Impact Analysis on the Global Second-generation thin-film solar cells Market:

The COVID-19 widespread has had a blended effect on the worldwide second-generation thin-film sun-powered cells advertise. Whereas the beginning disturbance caused by lockdowns and supply chain disturbances driven to delays in extended timelines and fabricating exercises, the widespread too catalyzed quickening the move towards renewable vitality. As governments around the world actualized jolt bundles and recuperation plans to restore economies, there has been a developing accentuation on green recuperation techniques, driving ventures in a clean vitality framework. Furthermore, the widespread highlighted the powerlessness of conventional vitality sources and the requirement for versatile and economical options, advance boosting requests for second-generation thin-film sun-based cells. Additionally, the move towards further work and digitalization has expanded the request for convenient gadgets fueled by sun-powered vitality, displaying modern openings for advertising development. In general, whereas COVID-19 is widespread at first posed challenges, it has eventually strengthened the significance of renewable vitality arrangements, situating the second-generation thin-film sun-powered cells showcase for long-term development and strength.

Latest Trends/ Developments:

The second-generation thin-film sun-powered cells showcase is seeing energetic patterns and improvements that are reshaping the industry scene. One outstanding drift is the expanding selection of developing innovations such as perovskite and natural photovoltaics, which offer the potential for higher efficiencies and lower generation costs compared to conventional thin-film innovations. Besides, there's a developing center on upgrading the supportability and natural effect of thin-film sun-oriented cells, with endeavors underway to progress fabric reusing forms and diminish the utilization of uncommon or harmful components. Another noteworthy slant is the integration of thin-film sun-based cells into building materials and customer gadgets, empowering consistent joining of the sun-based vitality era into regular items and frameworks. Also, progressions in fabricating forms, such as roll-to-roll generation and adaptable substrate innovations, are driving down generation costs and extending the extent of applications for thin-film sun-powered cells. In general, these patterns emphasize the industry's commitment to advancement, supportability, and flexibility, situating second-generation thin-film sun-oriented cells as a key player within the worldwide move towards renewable vitality arrangements.

Key Players:

-

First Solar, Inc.

-

Solar Frontier K.K.

-

Hanergy Thin Film Power Group Ltd.

-

MiaSole

-

Ascent Solar Technologies, Inc.

-

Avancis GmbH & Co. KG

-

Solaria Corporation

-

Manz AG

-

HelioVolt Corporation

-

Global Solar Energy, Inc.

-

Kaneka Corporation

-

Oxford PV