Oncology PET-CT Scanner Devices Market Size (2024–2030)

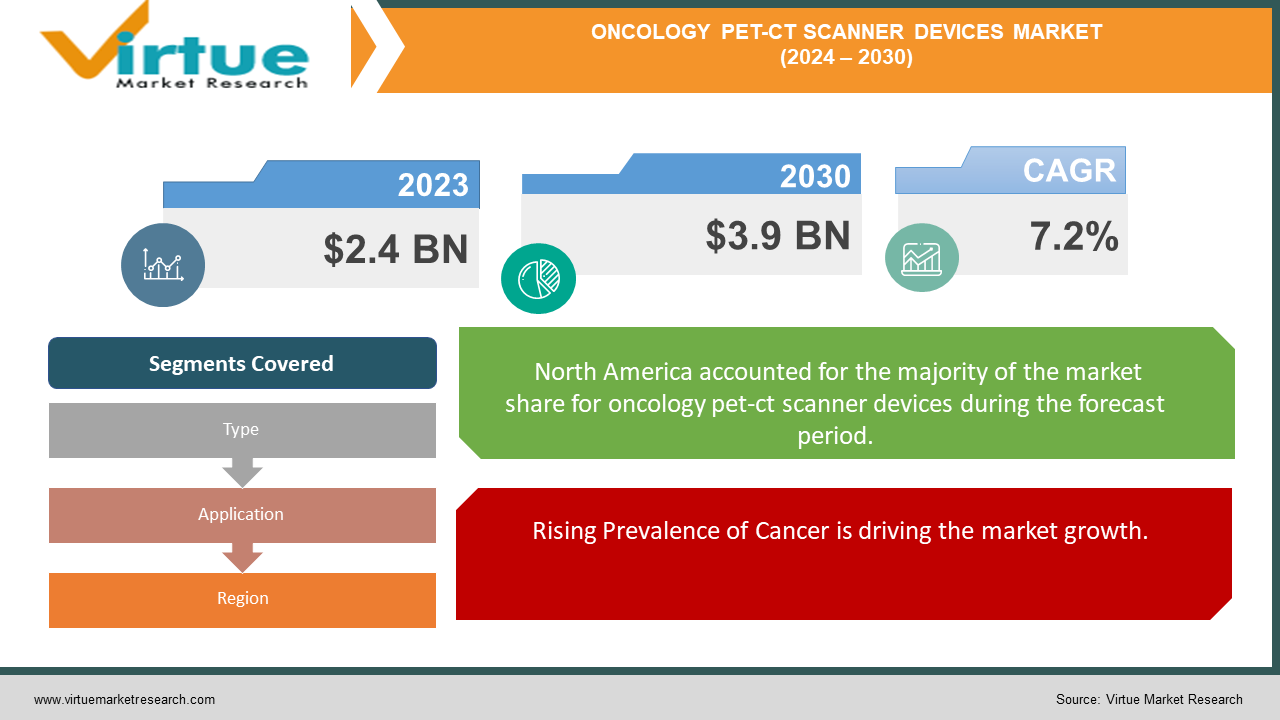

The global oncology PET-CT scanner devices market was US$ 2.4 billion in 2023 and is likely to exhibit a CAGR of 7.2% during 2024-2030. Presumably, the market is likely to grow to US$ 3.9 billion by 2030.

Oncology PET-CT scanners are in high requirement, especially in accurate diagnosis, staging, and monitoring of cancer that permits effectual design of treatment with better results in patients. It is also being driven by the rise in cancer cases, coupled with advancements in imaging modalities and greater adoption of PET-CT scanners across developing countries.

Key Market Insights:

The hospital segment is most obvious and projected to head the end-user segment, considering that advanced diagnostic imaging found a lot of applications in hospitals.

North America dominates the oncology PET-CT scanner devices market, followed closely by Europe and then Asia-Pacific.

A rise in cancer cases and improving imaging technology drive the market's growth to a great extent.

Ongoing research and development activities aimed at enhancing the performance and performance capabilities of PET-CT scanners foster their adoption in oncology.

Global Oncology PET-CT Scanner Devices Market Drivers:

Rising Prevalence of Cancer is driving the market growth.

The rising prevalence of cancer globally is a major driver of the Oncology PET-CT Scanner Devices Market. Cancer is rated among the top killer diseases globally, and it has registered an increase year after year. Therefore, early detection and diagnosis of cancer patients with a PET-CT scanner are very important in terms of staging and following up for effective treatment planning with better outcomes. The rising burden of cancer increases the demand for advanced diagnostic imaging technologies such as PET-CT scanners for better management and care of patients with cancer. On the other hand, the increase in the aging population, coupled with changes in lifestyle and environment, are some of the factors contributing to a rise in cancer incidence, hence raising the demand for oncology PET-CT scanners.

Improved Imaging Technologies are driving the market growth.

The improvement in imaging technologies is another key driver of the Oncology PET-CT Scanner Devices Market. Inventions and continued improvements in technological gadgets, such as PET-CT scanners, improve their accuracy, sensitivity, and specificity in detecting cancerous lesions. Expert system software, with advancements in imaging techniques in terms of artificial intelligence and machine learning, further optimized the image quality, shortened examination time, and made possible the accurate quantitation of metabolic activity in the tumors. These advancements in technology are enabling healthcare providers to ensure better diagnostic accuracy and find customized treatment protocols for cancer patients.

Rising Adoption in Emerging Markets is driving market growth.

Growing adoption of oncology PET-CT scanner devices in emerging countries is also paving the pathway of growth for this market. With growing healthcare infrastructure in emerging economies, especially in the Asia-Pacific and Latin American regions, along with investments in advanced medical technologies, demand for PET-CT scanners keeps increasing due to the rise in health expenditure and awareness of early cancer detection in these regions. Apart from that, increasing access to health care and the presence of more patients in the developing markets are offering lucrative conditions for market participants to expand their presence and meet the surging demand for oncology PET-CT scanners.

Global Oncology PET-CT Scanner Devices Market Challenges and Restraints:

The high cost of PET-CT Scanner Devices is restricting the market growth.

The high price of PET-CT scanner devices is one major challenge to the growth of oncology PET-CT scanner devices. Of course, sophisticated technology and advanced features give definite reasons as to why PET-CT scanners would be highly-priced, both in purchase and maintenance. That essentially means it is going to turn out to be an entry barrier for a lot of healthcare facilities, more so in developing regions and smaller healthcare institutions. These cost constraints to the adoption of PET-CT scanners can consequently restrict the widespread setting-up of these devices, particularly in resource-limited settings. Moreover, healthcare providers' reimbursement policies and budgetary constraints may influence the affordability and accessibility of the PET-CT scanner device, thus acting as a growth deterrent.

Regulatory and Reimbursement Challenges are restricting the market growth.

One more factor that is going to restrain the Oncology PET-CT Scanner Devices Market is regulatory and reimbursement challenges. The strict regulatory requirement for approval and commercialization of medical imaging devices makes it complex and increases the time to market for new PET-CT scanners. Compliance with such standard-setting regulations and obtaining appropriate certifications may be time-consuming and expensive for manufacturers. Besides, different regions and health care system have their policies of reimbursement numbers for PET-CT scanning would impact the adoption and utilization of these devices. These reimbursement challenges can decrease the financial sustainability of healthcare providers and reduce access of patients to new, innovative diagnostic imaging technologies, thus acting as a growth constraint.

Market Opportunities

The global oncology PET-CT scanner device market holds immense growth and innovative potential. Some of the major opportunities include the expanding applications of PET-CT scanners in personalized medicine and targeted therapies. As such, PET-CT scanners form an integral part of the course of developing patient management plans in that they are capable of providing useful information to the treating team about tumor biology and its response to treatment. This need thus heightens with advanced imaging techniques like PET-CT scanners, especially in guiding therapy decisions and monitoring therapeutical efficiency. Another opportunity could be in compact and portable PET-CT scanner devices. There is an emerging market in mobile imaging solutions and point-of-care diagnostic tools; therefore, a manufacturer has the opportunity to produce new portable PET-CTs usable in any healthcare setting. Besides, increasing research and development activities for developing high sensitivity, high resolution, and cost-effective PET-CT scanners have opened a window of opportunities for market participants to introduce more advanced and cost-effective imaging techniques. Overall, key factors contributing to growth were expanding applications of imaging techniques in personalized medicine, portable device development, and advancements in imaging technology.

ONCOLOGY PET-CT SCANNER DEVICES MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

7.2% |

|

Segments Covered

|

By Type, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Siemens Healthineers AG, GE Healthcare, Koninklijke Philips N.V., Canon Medical Systems Corporation, Shimadzu Corporation, Hitachi, Ltd., United Imaging Healthcare Co., Ltd., Neusoft Medical Systems Co., Ltd., Fujifilm Holdings Corporation, Carestream Health, Inc.

|

Oncology PET-CT Scanner Devices Market Segmentation - by Type

Full-ring PET-CT scanners dominate the Oncology PET-CT Scanner Devices Market. Full-ring PET-CT scanners offer finer resolution images and are preferred for oncology applications with high diagnosis accuracy. They have offered comprehensive imaging capabilities, which help in the exact localization and characterization of cancerous lesions.

Oncology PET-CT Scanner Devices Market Segmentation - by Application

-

Hospitals

-

Diagnostic Centers

-

Research Institutes

The hospital segment is considered the most dominant application area in the Oncology PET-CT Scanner Devices Market. This is because hospitals are better positioned in terms of structure and manpower to invest in novel diagnostic image technology, such as a PET-CT scanner. A high volume of patients and the need for the diagnosis and planning of cancer treatment drive the demand for a PET-CT scanner from hospitals.

Oncology PET-CT Scanner Devices Market Segmentation - by Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

North America dominates the Oncology PET-CT Scanner Devices Market owing to developed healthcare infrastructure and high cancer prevalence that raises demand for PET-CT scanners in the region. Furthermore, the presence of key market players and advanced research and development activities support the growth of the oncology PET-CT scanner device market in North America.

COVID–19 Impact Analysis on Oncology PET-CT Scanner Devices Market:

The COVID-19 pandemic has had both positive and negative impacts on the Global Oncology PET-CT Scanner Devices Market. Initially, during the phases of the outbreak, the market witnessed several disruptions to supply chains, manufacturing, and installations due to lockdowns and restrictions. Non-urgent medical procedures, including cancer screenings and diagnostic imaging, were put off, creating a short-term slump in the demand for PET-CT scanners. However, as healthcare systems also learned to live with the reality of the pandemic, the importance of accurate diagnosis and monitoring of cancer began to show. The demand for PET-CT scanners was based on timely and precise cancer imaging guiding treatment decisions. There should be good demand for advanced diagnostic imaging technologies like PET-CT scanners in the post-pandemic time frame when healthcare providers can work through the accumulated backlog of cancer screenings and diagnosis procedures.

Latest Trends/Developments:

Some trends and developments the oncology PET-CT scanner devices market has been witnessing include the integration of artificial intelligence with PET-CT imaging. Currently under development, AI-powered algorithms would enhance image reconstruction, allow improved lesion detection, and provide quantitative analysis of tumor characteristics. These new advancements improve the accuracy of PET-CT scans and, hence, better futurist and personalized treatment planning possibilities with their efficiency. Another key trend is the development of hybrid imaging systems that integrate PET-CT with other image modalities, like Magnetic Resonance Imaging or Single Photon Emission Computed Tomography, to ensure comprehensive and multi-parametric imaging in cancer. Hybrid imaging systems offer advanced anatomic and functional details and thus enhance diagnostic accuracy and treatment outcomes. Besides, the increasing focus on product innovation through research and development activities to increase sensitivity, resolution, and cost-effectiveness is boosting innovations in the market. Digital PET-CT technology with high-quality images and faster scan times is gaining momentum in oncology. In general, owing to the integration of AI, the development of hybrid imaging systems, and improvements in digital PET-CT technology, this overall oncology PET-CT scanner devices market is becoming one characterized by rapid technological developments and product innovations.

Key Players:

-

Siemens Healthineers AG

-

GE Healthcare

-

Koninklijke Philips N.V.

-

Canon Medical Systems Corporation

-

Shimadzu Corporation

-

Hitachi, Ltd.

-

United Imaging Healthcare Co., Ltd.

-

Neusoft Medical Systems Co., Ltd.

-

Fujifilm Holdings Corporation

-

Carestream Health, Inc.