Nasal Endoscopic Devices Market Size (2024 – 2030)

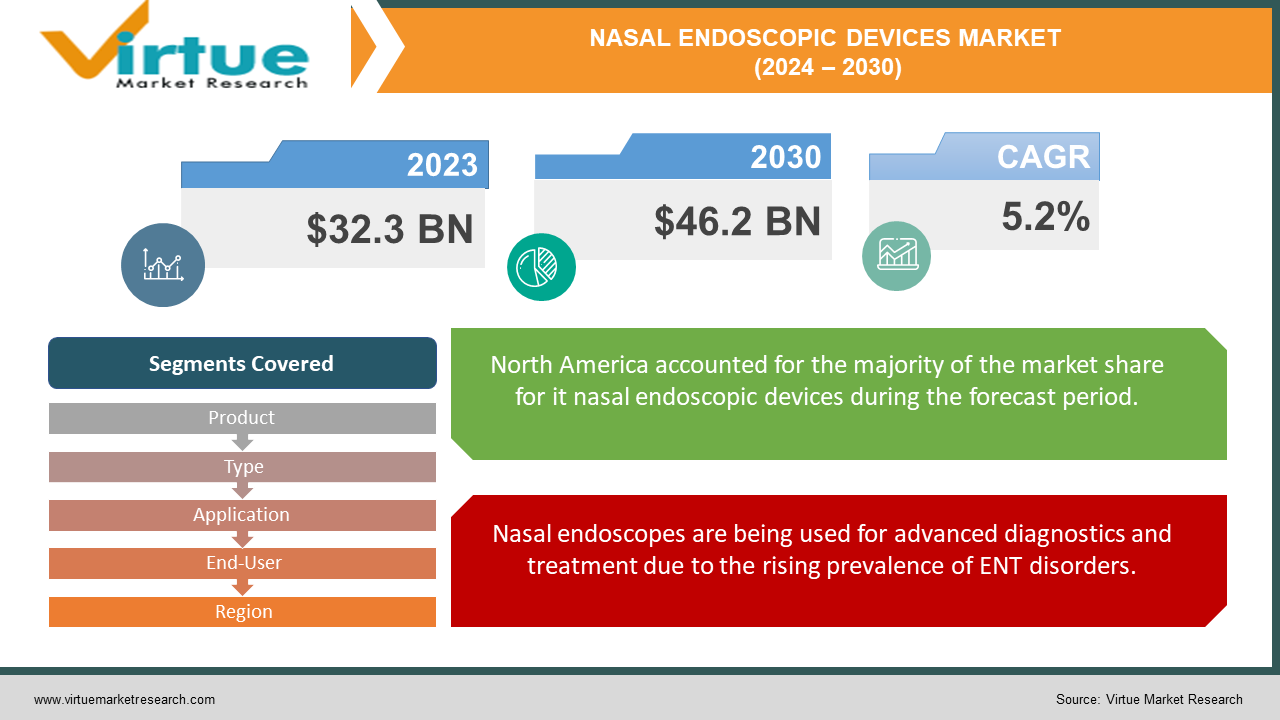

The Global Nasal Endoscopic Devices Market was valued at USD 32.3 billion in 2023 and is projected to reach a market size of USD 46.2 billion by 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 5.2%.

A camera and light source are attached to a narrow, tube-shaped device called a nasal endoscope, which enables medical professionals to look inside your sinuses and nose. Numerous illnesses are diagnosed and treated with these minimally invasive treatments. There are two primary varieties: flexible endoscopes, which are smaller and more adept at fitting through tight spaces, and rigid endoscopes, which provide high-resolution pictures. The actual treatment, which takes place in an office, is usually painless. Doctors can identify conditions including allergies, tumors, and sinus infections by using an endoscope inserted via a nostril to inspect the interior of your nose and sinuses on a monitor. Treatment options for nasal endoscopy include polyp removal, sinus opening, and nosebleed prevention.

Key Market Insights:

The nasal endoscope market is expected to develop at the quickest rate in the Asia Pacific region. By 2032, the nasal endoscope segment of the worldwide endoscopic devices market is projected to reach USD 103.59 billion, with the Asia Pacific region exhibiting the highest compound annual growth rate (CAGR) of 7.5%. The expansion of healthcare facilities in this area, rising healthcare costs, and growing public knowledge of ENT problems are all considered contributing factors to this trend

Global Nasal Endoscopic Devices Market Drivers:

Nasal endoscopes are being used for advanced diagnostics and treatment due to the rising prevalence of ENT disorders.

The rise in ENT problems is a major factor fueling the global market for nasal endoscopic devices. As allergies, sinusitis, and nasal polyps become more common, there is an urgent need for efficient diagnostic and therapeutic approaches. Millions of people worldwide suffer from sinusitis, an infection of the sinuses that causes headaches, congestion, and face discomfort. Nasal polyps are abnormal growths in the nasal cavity that can cause infections and breathing obstructions. Airborne irritants that cause allergies can frequently set off a chain reaction of ENT symptoms, including runny nose, sneezing, and itchy eyes. If these illnesses are not identified or treated, they can worsen the quality of life in addition to posing a risk of consequences. As the prevalence of ENT problems rises, nasal endoscopes have shown to be an invaluable tool in treating them. Doctors can see the interior of the sinuses and nose in detail thanks to these minimally invasive devices. The capacity to visualize data is essential for precise ENT diagnosis. For example, a nasal endoscope can be used to identify the infected sinus and evaluate if it is the result of a viral or bacterial illness when the sinus infection is suspected. Endoscopy makes it possible to precisely assess the size and location of nasal polyps. Physicians may create individualized treatment programs with this comprehensive information, which improves patient outcomes. Thus, the growing incidence of ENT illnesses and the benefits that nasal endoscopes provide in terms of diagnosis and treatment are driving up demand for these instruments in the international market.

Centre-stage nasal endoscopy is a powerful tool for early diagnosis timely identification and efficient treatment of ENT conditions.

The early detection of ENT disorders is increasingly becoming a top priority in healthcare, and nasal endoscopes are essential to this change. In the past, identifying ENT problems may have depended on less conclusive techniques like X-rays or patient reports of symptoms. These techniques, however, are not always able to identify the precise source and location of an issue. This resulted in overlooked problems, delayed diagnosis, and even ineffective first therapies. Better treatment outcomes, however, depend on an accurate and timely diagnosis. Doctors can directly see the internal anatomy of the sinuses and nasal cavity during nasal endoscopy. A thorough inspection enables the early detection of anomalies such as polyps, tumors, or infection symptoms. Early identification allows for the most suitable course of therapy to be implemented, potentially lowering the intensity and duration of symptoms. Furthermore, consequences from neglected ENT diseases might be avoided with early detection. Prioritizing early management not only enhances patient outcomes but also lowers medical expenses related to treating ENT illnesses in their later stages. Thus, a major factor driving the need for nasal endoscopes in the worldwide market is the emphasis on early diagnosis.

Global Nasal Endoscopic Devices Market Restraints and Challenges:

Notwithstanding the market expansion for nasal endoscopic devices, challenges still need to be addressed. These sophisticated gadgets may be expensive to buy and operate, which can be a hardship for healthcare organizations with tight budgets. Inadequate reimbursement for nasal endoscopic treatments might potentially deter uptake. A further problem is the lack of qualified personnel who are proficient in the use of nasal endoscopes. Tight laws have the potential to impede the adoption of cutting-edge technology, and the market is highly competitive due to worries about fake goods endangering consumers' safety. To guarantee greater accessibility to nasal endoscopic operations and sustained market expansion, these obstacles must be overcome.

Global Nasal Endoscopic Devices Market Opportunities:

The market for nasal endoscopic equipment has a promising future. Numerous elements provide stimulating prospects. The advantages of nasal endoscopy over standard surgery for ENT disorders completely fit with patients' demand for least invasive methods. This pattern fosters market expansion, as does the rise of developing economies and their rising healthcare spending. Another important factor is technological development, which promises increased effectiveness, precision, and cost in treatments. Examples of these breakthroughs include disposable endoscopes, AI-powered diagnostics, and even robot-assisted surgeries. Furthermore, the need for nasal endoscopes is expected to increase due to a greater emphasis on early detection of ENT illnesses and increased public awareness of these disorders. The global market for nasal endoscopic devices has the potential to grow in the next years if these possibilities are taken advantage of.

NASAL ENDOSCOPIC DEVICES MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

5.2%

|

|

Segments Covered

|

By Product, Type, Application, End-User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Ambu A/S, B. Braun Melsungen AG, Boston Scientific Corporation, Cook Medical, Fujifilm Holdings Corporation, HOYA Corporation, Johnson & Johnson (Ethicon Endo-Surgery), KARL STORZ SE & Co. KG, Medtronic plc, Olympus Corporation, PENTAX Medical, Richard Wolf GmbH, Stryker Corporation

|

Global Nasal Endoscopic Devices Market Segmentation: By Product Type

Three product categories can be identified by breaking down the worldwide nasal endoscopic devices market by product type: rigid endoscopes for high-resolution imaging, flexible endoscopes for squeezing through tight spaces, and disposable endoscopes. Because they reduce the danger of contamination and do away with the necessity for reprocessing, disposable endoscopes are notably growing at the quickest rate in infection control measures.

Global Nasal Endoscopic Devices Market Segmentation: By Application

-

Diagnostic Endoscopes

-

Therapeutic Endoscopes

Two groups emerge from the application-based segmentation of the global nasal endoscopic devices market: therapeutic and diagnostic endoscopes. Given the increasing emphasis on early intervention, diagnostic endoscopes—which are essential for assessing the nasal cavity and assisting in the early detection of ENT conditions—are probably the most popular and may expand at the quickest rate. There are also therapeutic endoscopes on the market that are utilized in surgical treatments.

Global Nasal Endoscopic Devices Market Segmentation: By End-User

End users may be used to segment the worldwide market for nasal endoscopic devices. Because they undertake so many different types of therapeutic and diagnostic operations that call for nasal endoscopes, hospitals, and clinics probably make up the largest portion. However, the usage of these devices in ENT clinics and ambulatory surgical centers is also increasing, especially for less complicated operations.

Global Nasal Endoscopic Devices Market Segmentation: By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

Due to its sophisticated healthcare system and high incidence of ENT problems, North America presently holds the top position in the worldwide nasal endoscopic devices market. However, due to rising healthcare costs, increased public awareness of ENT problems, and the construction of healthcare facilities in the area, the Asia Pacific region is anticipated to have the greatest growth in this market. The worldwide market is additionally influenced by the Middle East, Africa, South America, and Europe.

COVID-19 Impact Analysis on the Global Nasal Endoscopic Devices Market:

The initial spike in COVID-19 cases overwhelmed the healthcare system, delaying elective nasal endoscopies and resulting in a drop in demand for the actual equipment. Device availability was further restricted by the disruptions caused by lockdowns to global commerce channels and production. Furthermore, the pandemic's emphasis on allocating resources may have resulted in a decrease in the number of referrals for ENT physicians who use nasal endoscopes. Positive advances were seen. Although it is not a conclusive method of diagnosis, the potential use of nasal endoscopy to see COVID-19 symptoms in the nasal cavity has rekindled interest in the technique. The market may have eventually benefited indirectly from the growth of telemedicine during the epidemic. Consultations via telemedicine may result in increased referrals for treatments using nasal endoscopy when judged required. Although the pandemic's first shock produced a brief setback, the long-term effects are probably less severe.

Recent Trends and Developments in the Global Nasal Endoscopic Devices Market:

Technology is one major area of improvement; disposable endoscopes are becoming more popular for better infection management, and more recent endoscopes use high-definition cameras for better visualization. Even in the medical field, artificial intelligence is becoming more prevalent. AI-driven tools let physicians analyze endoscopic pictures in real-time, which may result in more accurate diagnoses. According to a preliminary study, robotic assistance may eventually be used in treatments, providing even more accuracy for delicate nose surgery. Beyond technology, the industry is being pushed by a rising need for less intrusive operations, which is exactly what nasal endoscopes are good for. Emerging areas are offering noteworthy prospects for expansion as they allocate resources toward healthcare infrastructure and integrate novel technology. Public awareness initiatives that inform the public about ENT problems and the advantages of early diagnosis with nasal endoscopy are driving the market even more.

Key Players:

-

Ambu A/S

-

B. Braun Melsungen AG

-

Boston Scientific Corporation

-

Cook Medical

-

Fujifilm Holdings Corporation

-

HOYA Corporation

-

Johnson & Johnson (Ethicon Endo-Surgery)

-

KARL STORZ SE & Co. KG

-

Medtronic plc

-

Olympus Corporation

-

PENTAX Medical

-

Richard Wolf GmbH

-

Stryker Corporation