Medical Digital Telepathology Market Size (2024-2030)

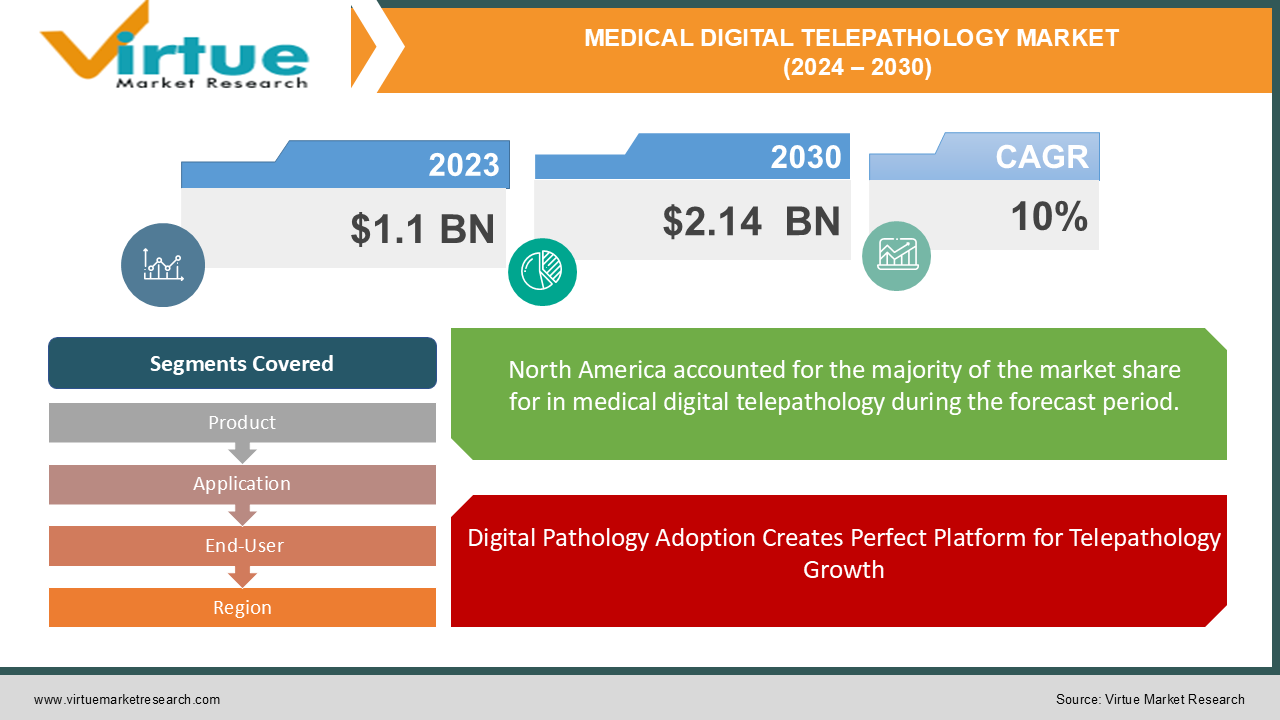

The Medical Digital Telepathology Market was valued at USD 1.1 billion in 2023 and is projected to reach a market size of USD 2.14 billion by the end of 2030. Over the cast period of 2024 – 2030, the figure for requests is projected to grow at a CAGR of 10%.

The medical digital telepathology market is flourishing, driven by several key trends. The rising adoption of digital pathology in labs lays the groundwork for telepathology's success. This technology allows pathologists to remotely analyze digitized slides, addressing the growing demand for remote diagnostics. Factors like a shortage of pathologists, the rise of telemedicine, and the recent pandemic have all highlighted the need for such solutions.

Key Market Insights:

-

This technology allows pathologists to remotely analyze digitized slides, addressing the critical need for remote diagnostics. The shortage of pathologists, particularly in underserved areas, and the rise of telemedicine highlight this need. Telepathology effectively bridges this gap by enabling remote analysis, potentially improving access to care for millions of patients.

-

Beyond improved access, telepathology offers a range of benefits. It streamlines workflows in pathology labs by eliminating physical slide transportation, saving valuable time and resources. Specialists can collaborate on complex cases regardless of location, fostering knowledge sharing and potentially leading to better diagnoses. High-resolution digital slides enable detailed analysis and consultation with other pathologists, which could contribute to improved diagnostic accuracy.

-

With continuous advancements in technology, such as artificial intelligence, and the rising adoption of digital pathology workflows, the future of medical digital telepathology appears promising. The market is expected to reach up to USD 1.8-2.1 billion by a projected year. As technology evolves and the need for remote diagnostics grows, medical digital telepathology is poised to play an increasingly important role in modern healthcare delivery.

The Medical Digital Telepathology Market Drivers:

Digital Pathology Adoption Creates Perfect Platform for Telepathology Growth

The increasing adoption of digital pathology in pathology labs, estimated to be growing at a rate of 8% annually, lays the groundwork for the success of telepathology. As pathology labs transition to digital workflows, they create digitized versions of slides that can be easily analyzed remotely. This synergy between digital pathology and telepathology creates a powerful ecosystem where the adoption of one fuels the growth of the other.

Telepathology Bridges the Gap in Remote Diagnostics for Underserved Areas

The demand for remote diagnostic solutions is being driven by a critical shortage of pathologists, particularly in underserved and geographically remote areas. This lack of qualified professionals creates a barrier to timely and accurate diagnoses for patients in these regions. Telepathology effectively bridges this gap by allowing qualified pathologists to analyze digitized slides remotely, regardless of the patient's location. This not only improves access to care for millions but also helps address healthcare disparities.

Elimination of Physical Slide Transport Boosts Workflow Efficiency in Labs

Telepathology streamlines workflows within pathology labs by eliminating the need for physical slide transportation. This translates to significant time and resource savings. Pathologists can spend less time waiting for physical slides to arrive and dedicate more time to crucial diagnostic tasks. Additionally, labs can eliminate costs associated with the transportation and logistics of physical slides, leading to overall operational cost reductions.

Remote Collaboration and High-Resolution Slides Enhance Diagnostic Potential

Telepathology fosters collaboration among specialists by enabling remote consultations on complex cases. Pathologists can consult with colleagues regardless of location, facilitating knowledge sharing and fostering a collaborative diagnostic environment. This exchange of expertise can lead to more informed decision-making, potentially resulting in improved diagnostic accuracy. Furthermore, telepathology utilizes high-resolution digital slides that allow for detailed analysis. The ability to share these detailed images with other pathologists can further enhance the diagnostic process and potentially contribute to a reduction in diagnostic errors.

The Medical Digital Telepathology Market Restraints and Challenges:

Despite its promising growth, the medical digital telepathology market faces some challenges. The initial investment can be significant, as labs need digital pathology scanners, image analysis software, and secure communication systems. This can be a hurdle, particularly for developing countries with limited healthcare budgets. Additionally, reimbursement policies for telepathology services might not be well-established, creating further barriers to adoption.

Regulations pose another challenge. Telepathology operates at the intersection of medicine and technology, leading to a complex regulatory landscape. Data privacy, security standards for telepathology workflows, and licensing requirements for remote pathologists can vary significantly between countries. These variations create uncertainty and hinder market growth. Security and privacy concerns are also paramount. Transferring sensitive patient data, including digital pathology slides, requires robust cybersecurity measures to prevent unauthorized access or data breaches. Clear data privacy regulations are crucial to ensure patient information remains protected.

The Medical Digital Telepathology Market Opportunities:

The future of medical digital telepathology is brimming with exciting opportunities. Developing countries, often lacking sufficient pathologists, represent a significant growth prospect. Telepathology can bridge this gap by enabling remote consultations with specialists, improving access to quality healthcare in these regions. Furthermore, the integration of Artificial Intelligence (AI) with telepathology holds immense potential. AI can assist pathologists in numerous ways, such as automating tasks, highlighting areas of concern in slides, and even offering preliminary diagnoses. This collaboration can improve efficiency, potentially reduce errors, and allow pathologists to focus on more complex cases. The rising popularity of telemedicine creates a natural synergy with telepathology. By integrating these services, healthcare providers can offer a more comprehensive remote diagnostic experience for patients. Additionally, the focus on personalized medicine, which relies on detailed analysis of patient data including pathology slides, aligns perfectly with telepathology. Sharing digital slides with a wider network of specialists through telepathology can potentially lead to more informed treatment decisions and improved patient outcomes. Finally, continuous advancements in technology, such as high-speed internet, robust cybersecurity solutions, and user-friendly interfaces for telepathology systems, will further propel market growth.

MEDICAL DIGITAL TELEPATHOLOGY MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

10% |

|

Segments Covered

|

By Product, Application, End-User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Abbott Laboratories, F. Hoffmann-La Roche Ltd, Leica Biosystems, Koninklijke Philips N.V., Siemens Healthineers AG, Hamamatsu Photonics, Inc., Olympus Corporation, GE Healthcare, Illumina, Inc., PerkinElmer Inc., Inspirata, Inc.

|

The Medical Digital Telepathology Market Segmentation: By Product

-

Hardware

-

Software

-

Services

The dominant segment in the Medical Digital Telepathology Market by Product is likely Software. The software offers functionalities for image analysis, workflow management, and teleconferencing, crucial for telepathology workflows. The fastest-growing segment is expected to be Services. The growing demand for remote slide interpretation, digital image archiving, and data security solutions is driving the Services segment.

The Medical Digital Telepathology Market Segmentation: By Application

The most dominant segment by application in the Medical Digital Telepathology Market is likely Disease Diagnosis. This segment addresses a vast range of illnesses, making it crucial for daily healthcare operations. On the other hand, the fastest-growing segment is expected to be Drug Discovery & Development. The pharmaceutical industry's continuous research and development efforts, along with the growing adoption of telepathology, are fueling this segment's rapid expansion.

The Medical Digital Telepathology Market Segmentation: By End-User

Hospitals are the dominant segment in the medical digital telepathology market due to the high volume of pathology cases they handle. However, the fastest-growing segment is expected to be in developing countries within the Rest of the World sector. This growth is driven by the increasing need for improved healthcare access in these regions, along with government initiatives to bridge this gap.

The Medical Digital Telepathology Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

Currently, North America holds the dominant position in the medical digital telepathology market. This dominance is fuelled by factors like high healthcare spending, early adoption of digital pathology technologies, and a well-established healthcare infrastructure. Additionally, the presence of major market players and favorable government regulations further solidify North America's leading role.

Europe represents a strong market for medical digital telepathology due to its well-established healthcare system and growing awareness of the benefits telepathology offers. Government initiatives promoting digital health advancements and a focus on improving diagnostic efficiency are driving market growth in this region.

The Asia-Pacific region boasts the fastest growth potential in the medical digital telepathology market. This surge is driven by a rapidly expanding healthcare sector, increasing government investments in healthcare infrastructure, and a growing middle class with rising disposable income. Furthermore, the significant shortage of pathologists in this region makes telepathology a highly attractive solution for bridging the access gap.

COVID-19 Impact Analysis on the Medical Digital Telepathology Market:

The COVID-19 pandemic served as a significant turning point for the medical digital telepathology market, acting as a major accelerator for its adoption. The need for social distancing and minimizing in-person contact during the pandemic fuelled the demand for remote diagnostic solutions. Telepathology emerged as a safe and effective answer, enabling remote analysis of slides, and reducing the risk of exposure for pathologists. Furthermore, with limitations on physical movement due to lockdowns, telepathology ensured uninterrupted pathology services by allowing pathologists to continue diagnoses remotely, preventing delays in patient care. Additionally, telepathology streamlined workflows in pathology labs facing staffing shortages caused by the pandemic. Eliminating the need for physical slide transportation saved valuable time and resources for these strained labs. Beyond general diagnostics, telepathology even played a role in analysing lung tissue samples remotely to aid in faster diagnosis and treatment decisions for COVID-19 cases.

Latest Trends/ Developments:

The medical digital telepathology market is buzzing with exciting new developments. One major trend is the integration of Artificial Intelligence (AI). AI algorithms are becoming powerful allies for pathologists, automating routine tasks like image analysis and flagging potential areas of concern in slides. This frees up valuable time for pathologists to focus on complex cases and potentially improves diagnostic accuracy by providing a second layer of analysis. Cloud-based telepathology solutions are also gaining traction. These offer scalability and flexibility for labs, allowing them to easily adjust their services based on demand. Additionally, cloud solutions eliminate the need for expensive upfront hardware and software investments, making telepathology more accessible. User-friendly interfaces and mobile applications are further enhancing the user experience for pathologists, allowing them to review slides and collaborate with colleagues remotely with greater ease. Beyond traditional pathology, the remote analysis of cell samples, is a growing area within telepathology, offering improved access to cytopathology expertise in underserved regions.

Key Players:

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd

-

Leica Biosystems

-

Koninklijke Philips N.V.

-

Siemens Healthineers AG

-

Hamamatsu Photonics, Inc.

-

Olympus Corporation

-

GE Healthcare

-

Illumina, Inc.

-

PerkinElmer Inc.

-

Inspirata, Inc.