GLOBAL HEPATOCELLULAR CARCINOMA MARKET (2024 - 2030)

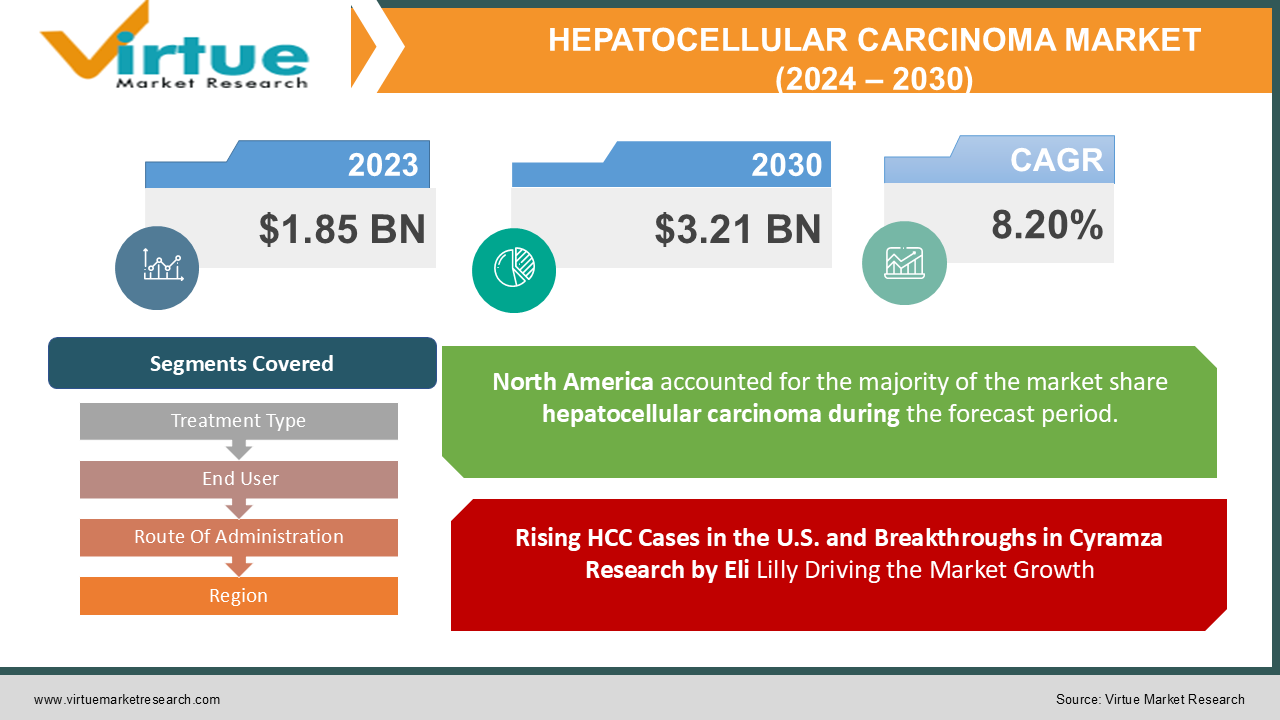

The Hepatocellular Carcinoma Market was valued at USD 1.85 billion in 2023 and is projected to reach a market size of USD 3.21 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 8.20%.

There is a type of primary cancer that arises from the hepatocytes. The disease is more prevalent in people with diabetes. The majority of the diagnosis of this condition is done by several tests. Targeted drug therapy is included in the treatment. Patients with end-stage of liver function have majority of HCC.

Key Market Insights:

- The major cause of death in patients with chronic liver diseases and cirrhosis is hepatocellular carcinoma, also known as HCC. The tumors grow in the local area and then spread to other parts of the body. Almost 40,000 people were affected with bile duct cancer in the US in 2022. There are a number of risks associated with Hepatocellular Carcinoma. Eli Lilly and Company completed a Phase 3 research study of a single agent in the second-line treatment of people with hepatocellular carcinoma.

- The growth of the global hepatocellular carcinoma treatment market can be attributed to the technological advancement in the detection and treatment of the disease. Increasing incidence of hepatocellular carcinoma and high exposure to toxins are some of the factors driving the growth of Global Hepatocellular Carcinoma Treatment Market. The low success rate in clinical trials for drugs is one of the factors that is expected to affect the growth of the market.

Hepatocellular Carcinoma Market Drivers:

Rising HCC Cases in the U.S. and Breakthroughs in Cyramza Research by Eli Lilly Driving the Market Growth

According to the survey by the Health Science Department, the University of California, Los Angeles, has found that HCC is the most common type of cancer in the U.S. More than 28,000 deaths are reported from the disease, with almost 40,000 Americans diagnosed with it in the last year. Eli Lilly and Company completed Phase 3 research study of Cyramza as a single agent in the second-line treatment of people suffering from hepatocellular carcinoma.

Novel drugs are getting approval driving market growth:

The approval of novel drugs by the regulatory agencies for the treatment of hepatocellular carcinoma is enhancing the growth of the market. In April of last year, the U.S. Regorafenib was expanded by the FDA for the treatment of patients with hepatocellular carcinoma. After the failure of standard treatments, the therapy improved survival for patients. In 2017, the U.S. The FDA granted accelerated approval for the drug nivolumab.

A recent wave of biologic products prescribed for treating HCC is likely to create a lucrative opportunity for market growth. There is still room for improvement in the treatment of HCC, despite the plethora of therapies currently available to patients.

Adoption of biological therapies is increasing driving market growth:

Immune-targeted therapies are used to treat hepatocellular carcinoma. There is a demand for therapies with novel MOAs after Nivolumab was approved for hepatocellular carcinoma.

Over the next few years, many new classes of therapies are looking to enter the global hepatocellular carcinoma treatment market. The market for programmed cell death 1 (PD-1) and programmed cell death ligand 1 (PD-L1) is growing due to their better clinical profile.

Hepatocellular Carcinoma Market Restraints and Challenges:

The market growth is hampered by the lack of drug approvals. There are no FDA-approved drugs to treat it. The limited availability of treatment processes can limit market growth.

The market growth is hampered by the rising expenditure associated with the various medications. The market's growth is hampered by several diagnostic procedures.

This hepatocellular carcinoma drugs marketplace record gives details of new current trends, trade guidelines, import-export evaluation, manufacturing analysis, cost chain optimization, market percentage, effect of domestic and localized marketplace players, analyses opportunities in terms of rising sales wallet, adjustments in marketplace policies, strategic market increase analysis, market size, class marketplace growths, utility niches and dominance, product approvals, product launches, geographic expansions, technological innovations within the market.

Hepatocellular Carcinoma Market Opportunities:

The manufactures are focused on several strategic collaborations to develop and sell immunotherapies that are indicated to treat wide range of tumors. Bristol-Myers Squibb Company & Ono Pharmaceutical Co. In order to address the unmet medical needs of patients with cancer in Japan, South Korea and Taiwan, a strategic collaboration agreement was made with Opdivo. The Phase 2 trials to compare the safety and efficacy of dovitinib and sorafenib in adult patients for treating advanced hepatocellular carcinoma was initiated in 2015.

According to the International Journal of Cancer Research and Treatment, the sixth most common type of cancer worldwide and a third most common cause of death worldwide, is HCC. More than 5% of all cancers are caused by the disease i.e., HCC (Hepatocellular Carcinoma).

GLOBAL HEPATOCELLULAR CARCINOMA MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

8.20 %

|

|

Segments Covered

|

By Treatment Type, End User, route Of Administration and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Bayer AG, Amgen Inc., Bristol-Myers Squibb Company, Eisai Co., Ltd., Eli Lilly and Company, Merck & Co., Inc., Novartis AG, Pfizer Inc.

|

Hepatocellular Carcinoma Market Segmentation:

Market Segmentation: By Treatment Type:

- Surgery

- Targeted Therapy

- Chemotherapy

- Radiology

- Immunotherapy

Based on the treatment type, the radiology treatment segment accounted for the largest revenue share and has led the market. Several other factors such as rising patient awareness, growing demand for various anti-aging treatments, and the surging cost of cosmetic treatments in developed nations are propelling the market growth for radiation therapy. While the demand for immunotherapy is increasing across the globe because of the checkpoint inhibitors has shown strong anti-tumour activity in HCC patients and the result it brings on table is quite acknowledgeable. the combination of the anti-PDL1 antibody atezolizumab and the VEGF-neutralizing antibody bevacizumab will soon become the standard of care as a first-line therapy for HCC. Immunotherapy is the fastest growing segment by treatment type.

Chemotherapy is used to treat advanced hepatocellular carcinoma. The results of two pivotal Phase III placebo-controlled studies show that sorafenib is the standard therapeutic agent for advanced HCC. After the introduction of sorafenib for the treatment of HCC, Phase III trials of other agents as first-line or second-line chemotherapy have been conducted to determine if any of them offer superior survival benefit to sorafenib.

Market Segmentation: By End-User

- Hospitals

- Cancer centers

- Clinics

Hospitals are the largest segment. The fastest-growing segment may be ambulatory surgery centres, which provide specialized treatments like TACE and RFA with convenience and cost-effectiveness. Clinics are the fastest growing segment.

Hospitals are the leading segment due to their comprehensive facilities, advanced diagnostic capabilities, diverse treatment options, and supportive care infrastructure. They offer a centralized setting for diagnosis, staging, treatment, and follow-up, with access to a multidisciplinary team of specialists and advanced diagnostic tools. Hospitals offer a wide range of treatment options and supportive care services to help patients manage their symptoms and improve their quality of life.

Clinics are emerging as the fastest-growing segment for HCC treatment due to several factors that enhance patient convenience, accessibility, and cost-effectiveness. Clinics offer an outpatient setting that gives flexibility and reduces the need for lengthy hospital stays for patients with early-stage HCC. Individualized care tailored to the specific needs of patients is provided by specialized HCC clinics, while technological advancement such as Fibro Scan and Ultrasonic elastography allow non-invasive assessment and diagnosis of HCC. Effective management in clinics has been made possible by the availability of targeted therapies. Continuation of care and improved patient outcomes are provided by clinics.

Market Segmentation: Route of Administration:

Injectables are the leading segment and fastest growing segment is Oral. As injectables are faster to show effects on patients as compared to oral methodology. The leading route of administration for the market is IVs, accounting for 45% of the market share. This is followed by oral administration with a third of the market share. The preferred route of administration for systemic therapies is intravenous administration. Systemic therapies can reach cancer cells throughout the body to prevent them from growing. Targeted therapies are drugs that are designed to target specific cancer cells to prevent them from growing. Regional therapies are treatments that are delivered directly to the liver.

Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

North America has a well-developed healthcare infrastructure, advanced diagnostic capabilities, and robust research and development initiatives. The region accounts for over 40% of the total market revenue and is expected to continue growing at a steady pace due to the introduction of new and more effective treatment options. Hospitals and research institutions are leading the development and adoption of innovative therapies, including targeted therapies, immunotherapy, and combination therapies. Patient outcomes and survival rates have improved. Leading researchers and pharmaceutical companies from around the world come to NA for clinical research and trials.

The Asia-Pacific region is rapidly emerging as a major player in the global HCC market, spurred by its burgeoning population, escalating prevalence of HCC risk factors, and expanding healthcare infrastructure. The region is poised to surpass North America in terms of revenue share. The growth trajectory is fuelled by factors such as the widespread prevalence of hepatitis B and C infections, the rapidly aging population, and the active pursuit of innovative therapeutic approaches. Increased market share, enhanced research and development efforts, and expanded opportunities for pharmaceutical companies will result from the Asia-Pacific region's growing prominence. As the region continues to innovate and lead in HCC management, it will undoubtedly remain a driving force in the global market.

COVID-19 Impact Analysis on the Global Hepatocellular Carcinoma Market:

The COVID-19 pandemic has considerably impacted the hepatocellular carcinoma marketplace. As in keeping with studies look at titled "Impacts of COVID-19 on Liver Cancers: During and after the Pandemic", published within the National Library of Medicine in May 2020, hepatocellular carcinoma (HCC) patients are extra susceptible to the outcomes of COVID-19 than other most cancers patients as the hepatic damage caused by SARS-CoV-2 may want to complicate the prevailing hepatitis virus infection and cirrhosis. Further, boundaries to having access to cancer tablets at some stage in the COVID-19 pandemic endangered the steadiness and integrity of pharmaceutical deliver chains, thus limiting the supply of medicine throughout healthcare centers. Thus, the COVID-19 pandemic has altered healthcare priorities, which may additionally adversely impact HCC control.

People with comorbidities were more likely to develop the virus if the diagnostic and treatment processes were delayed. The number of people visiting hospitals for treatment is reduced by these factors. With fewer COVID-19 instances and large-scale vaccination campaigns, the liver cancer treatments market will likely reach its full potential throughout the forecast period.

Latest Trends/ Developments:

The global Hepatocellular Carcinoma Market is reasonably split and fragmented with the existence of several global companies. These players are motivated to achieve higher market share by implementing different strategies, such as acquisitions, partnerships, and investments. Companies are also spending heftily on the development of improved products and infrastructure facilities alongside maintaining competitive pricing. This has further resulted in increased government engagement and the advancement of medical infrastructure.

There is a therapy called Immunotherapy. A type of cancer treatment that harnesses the body's immune system is called immunotherapy. Several clinical trials are currently underway evaluating the efficacy of immunotherapy for the treatment of HCC, and it is showing promise in the treatment of the disease.

Precision medicine. The approach to cancer treatment that tailor’s treatment to the individual patient's genetics is called precision medicine. It is hoped that precision medicine will lead to more effective and personalized treatment options in the future.

Early detection of HCC is crucial for improving the survival chances of the patient. With the help of advancement in technologies and medicine there have been few treatments or techniques to detect HCC are contrast-enhanced ultrasound (CEUS) and Gadoxetate (Gd-EOB-DTPA), Magnetic Resonance Imaging (MRI) is the most common technique for early detection of HCC in the patient.

The research and development of novel treatment alternatives and studying the combination treatment effects of drugs is being done by pharmaceutical companies. AVEO Pharmaceuticals, Inc. The trials of tivozanib plus durvalumab are being conducted in patients with advanced hepatocellular carcinoma.

Key Players:

- Bayer AG

- Amgen Inc.

- Bristol-Myers Squibb Company

- Eisai Co., Ltd.

- Eli Lilly and Company

- Merck & Co., Inc.

- Novartis AG

- Pfizer Inc.

- In February 2022, Eureka Therapeutics Inc. announced the U.S. Food and Drug Administration granted orphan drug status to two drugs named as ET140203 and ECT204 for the treatment of hepatocellular carcinoma, which is the most common form of cancer.