Gastric Cancer Market Size (2025 – 2030)

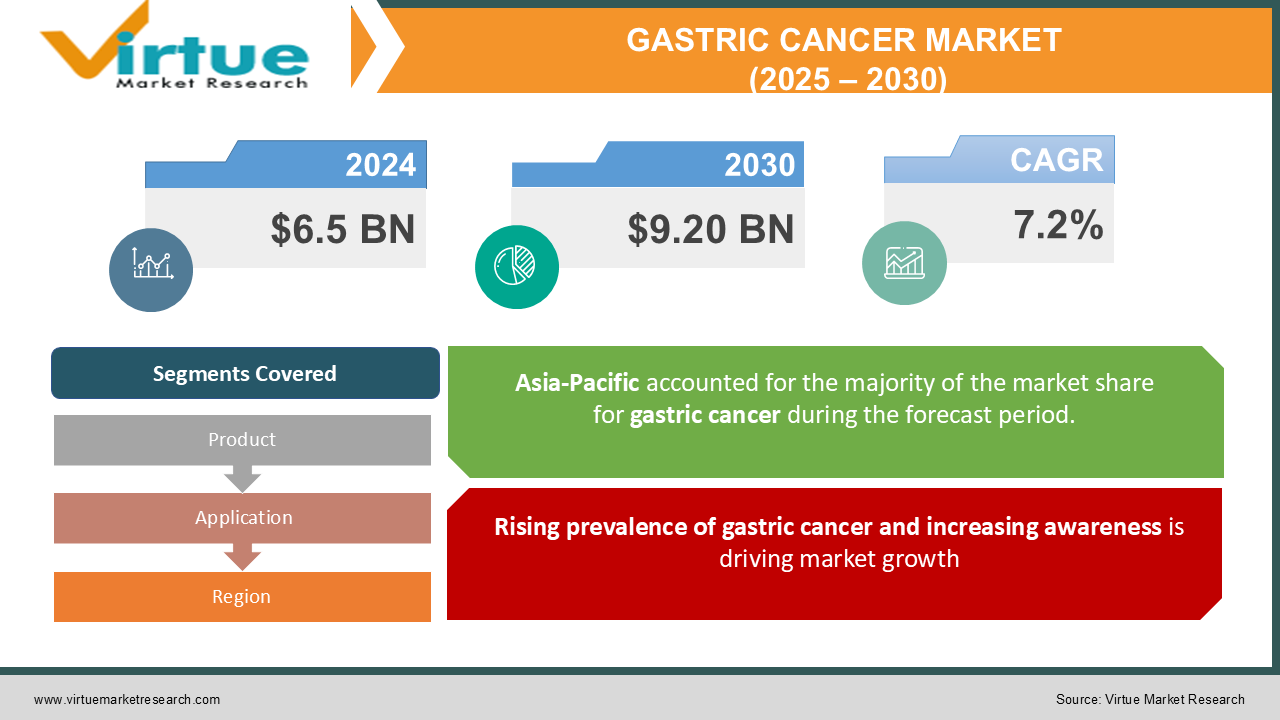

The Global Gastric Cancer Market was valued at USD 6.5 billion in 2024 and will grow at a CAGR of 7.2% from 2025 to 2030. The market is expected to reach USD 9.20 billion by 2030.

The Gastric Cancer Market focuses on the diagnosis, treatment, and management of gastric cancer, also known as stomach cancer. This market is driven by the increasing prevalence of gastric cancer, advancements in treatment methods, and rising awareness about early detection. The demand for targeted therapies, immunotherapies, and precision medicine approaches is expected to significantly influence market growth over the forecast period. With an aging global population and the rising burden of gastrointestinal diseases, the gastric cancer market is expected to expand as healthcare providers and pharmaceutical companies continue to develop innovative treatment solutions.

Key Market Insights

-

The prevalence of gastric cancer is rising worldwide, with over one million new cases diagnosed annually. The disease remains one of the leading causes of cancer-related deaths, particularly in East Asia, where incidence rates are the highest.

-

Immunotherapy has emerged as a key breakthrough in gastric cancer treatment, with checkpoint inhibitors such as pembrolizumab (Keytruda) and nivolumab (Opdivo) gaining regulatory approvals and demonstrating improved survival rates in clinical trials.

-

The market is witnessing a shift toward precision medicine, with molecular profiling and biomarker-based targeted therapies becoming more prevalent. HER2-positive gastric cancer treatments, such as trastuzumab (Herceptin), have gained significant traction.

-

The adoption of robotic and minimally invasive surgeries for gastric cancer treatment is increasing, leading to improved patient outcomes, shorter hospital stays, and reduced post-operative complications.

-

Asia-Pacific dominates the gastric cancer market due to the high disease burden, increasing healthcare expenditure, and government initiatives promoting cancer screening programs in countries like China, Japan, and South Korea.

-

Combination therapies, including chemotherapy combined with immunotherapy or targeted agents, are becoming standard practice, showing better response rates and prolonged survival in gastric cancer patients.

-

The high cost of advanced therapies and limited access to innovative treatments in developing regions remain significant challenges, creating disparities in patient outcomes.

-

Ongoing research and development efforts are focusing on novel drug candidates, with multiple pipeline drugs in phase II and III clinical trials aimed at improving efficacy and reducing toxicity.

Global Gastric Cancer Market Drivers

Rising prevalence of gastric cancer and increasing awareness is driving market growth:

The increasing incidence of gastric cancer worldwide is a significant driver of the market. The disease remains one of the most common malignancies, particularly in high-risk regions such as East Asia and Eastern Europe. Factors such as Helicobacter pylori infection, dietary habits, smoking, and genetic predisposition contribute to its rising prevalence. Efforts to increase public awareness and early detection through screening programs have led to improved diagnosis rates. Government initiatives and non-profit organizations have played a crucial role in promoting cancer screening and preventive measures. The growing understanding of risk factors and symptoms is encouraging individuals to seek medical attention earlier, thereby positively impacting the demand for diagnostic and treatment solutions.

Advancements in targeted therapies and immunotherapy is driving market growth:

The evolution of cancer treatment from traditional chemotherapy to targeted therapies and immunotherapy has transformed the landscape of gastric cancer treatment. Targeted therapies such as HER2 inhibitors (trastuzumab) and VEGF inhibitors (ramucirumab) have significantly improved patient survival rates. Immunotherapies like PD-1/PD-L1 inhibitors have demonstrated promising results, leading to regulatory approvals and increasing adoption. Research in molecular profiling and biomarker identification has enabled the development of personalized treatment approaches, further fueling market growth. As pharmaceutical companies continue to invest in innovative drug development, the availability of more effective treatment options is expected to expand.

Technological advancements in diagnostics and treatment is driving market growth: Technological innovations in diagnostic imaging, endoscopy, and molecular testing have significantly improved the early detection of gastric cancer. Advanced imaging techniques such as PET-CT scans, AI-powered diagnostic tools, and liquid biopsy methods enable early-stage diagnosis, leading to better treatment outcomes. Furthermore, the integration of robotic-assisted surgery and laparoscopic procedures has enhanced surgical precision, reducing complications and improving recovery times. These advancements contribute to increased adoption of advanced diagnostic and treatment options, ultimately driving the gastric cancer market forward.

Global Gastric Cancer Market Challenges and Restraints

High cost of treatment and limited access to advanced therapies is restricting market growth: One of the most significant challenges facing the gastric cancer market is the high cost of advanced treatment options. Targeted therapies, immunotherapies, and innovative diagnostic tools are often expensive, making them inaccessible to a large segment of the population, particularly in low- and middle-income countries. The high cost of drug development, clinical trials, and regulatory approvals further adds to the pricing burden. Limited reimbursement policies in several regions restrict patient access to these treatments, leading to disparities in healthcare outcomes. Despite advancements in cancer care, affordability remains a critical issue that needs to be addressed through policy changes, healthcare funding, and initiatives to reduce drug pricing.

Side effects and resistance to therapy is restricting market growth: While targeted therapies and immunotherapies have revolutionized gastric cancer treatment, they are not without challenges. Many patients experience severe side effects, including immune-related adverse reactions, gastrointestinal complications, and cardiotoxicity. Additionally, tumor resistance to therapy remains a significant concern, as some patients do not respond to treatment or develop resistance over time. This challenge necessitates continuous research into new drug combinations, novel therapeutic targets, and strategies to overcome resistance mechanisms. The need for personalized treatment approaches is increasing, emphasizing the importance of biomarker-driven therapies to enhance treatment efficacy.

Market Opportunities

The gastric cancer market presents significant opportunities for growth, particularly in the development of next-generation therapies. Emerging treatment modalities such as bispecific antibodies, CAR-T cell therapy, and RNA-based therapeutics hold promise for improving patient outcomes. The increasing focus on precision medicine and molecular diagnostics is expected to enhance early detection and personalized treatment approaches. Collaborations between pharmaceutical companies and research institutions are accelerating drug discovery and clinical trials, leading to a robust pipeline of innovative therapies. Additionally, the expansion of healthcare infrastructure in developing regions and growing investments in cancer research create opportunities for market expansion. The integration of artificial intelligence in diagnostics and treatment planning is expected to improve decision-making processes and optimize therapeutic outcomes. Overall, the gastric cancer market is poised for growth, driven by scientific advancements, strategic partnerships, and evolving treatment paradigms.

GASTRIC CANCER MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

7.2% |

|

Segments Covered

|

By Product, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Merck & Co., Bristol-Myers Squibb, Roche

, Eli Lilly, Pfizer, AstraZeneca, Novartis, Amgen

|

Gastric Cancer Market Segmentation - By Product

-

Chemotherapy drugs

-

Targeted therapy drugs

-

Immunotherapy drugs

-

Surgery

-

Radiation therapy

The most dominant segment is targeted therapy drugs due to their effectiveness in improving patient survival rates. HER2 inhibitors, VEGF inhibitors, and PD-1/PD-L1 inhibitors have gained widespread adoption, offering better outcomes compared to traditional chemotherapy. With the growing emphasis on personalized medicine, targeted therapies are expected to witness continued growth.

Gastric Cancer Market Segmentation - By Application

-

Hospitals

-

Specialty clinics

-

Research institutions

The most dominant segment is hospitals, as they serve as the primary centers for gastric cancer diagnosis, treatment, and surgeries. The availability of advanced medical technologies, multidisciplinary cancer care teams, and access to clinical trials contribute to hospitals' dominant position in the market.

Gastric Cancer Market Segmentation - By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

The most dominant region is Asia-Pacific due to the high prevalence of gastric cancer, increasing healthcare investments, and government-led screening programs. Countries like China, Japan, and South Korea have a significant patient pool, and advancements in cancer treatment have driven market growth. The presence of leading pharmaceutical companies, a strong clinical trial ecosystem, and improved access to innovative therapies further bolster the market in this region.

COVID-19 Impact Analysis on the Gastric Cancer Market

The COVID-19 pandemic had a profound impact on the gastric cancer market, causing substantial disruptions in several critical areas. With hospitals focusing on COVID-19 patients, many elective procedures, including cancer screenings, diagnostic tests, and scheduled treatments, were postponed or canceled. This led to significant delays in diagnosing gastric cancer, which in turn affected timely treatment initiation. Chemotherapy sessions and surgeries were rescheduled, impacting the overall care plan for many patients. Additionally, clinical trials experienced major setbacks as restrictions on patient enrollment and supply chain disruptions hindered the progress of new therapies. The temporary halt in research and development slowed the introduction of innovative treatments and therapies that could have benefited patients. However, the pandemic also accelerated certain trends in the healthcare industry. Telemedicine, which had previously been seen as a supplementary tool, became essential for cancer consultations during the pandemic. This shift allowed patients to access medical advice remotely, reducing the burden on healthcare facilities and ensuring continued care during lockdowns. Moreover, the pandemic highlighted the crucial importance of early detection, which spurred increased awareness among both healthcare professionals and the general public about the need for regular screenings. As the world moves into the post-pandemic phase, the gastric cancer market is expected to recover. There is now a renewed emphasis on strengthening cancer screening programs, improving healthcare infrastructure, and ensuring uninterrupted access to treatments. The lessons learned from the pandemic have driven a more innovative approach to cancer care, which, along with a growing focus on patient-centered care, will likely improve outcomes in the coming years. The pandemic, while disruptive, has ultimately created an opportunity to enhance and modernize gastric cancer care.

Latest Trends/Developments

The gastric cancer market is undergoing significant advancements, particularly in immunotherapy, AI-driven diagnostics, and combination therapies. These innovations are shaping the future of treatment, offering new hope for patients. Immunotherapy, which harnesses the body's immune system to fight cancer, is becoming a prominent focus of research, showing promise in improving survival rates for gastric cancer patients. At the same time, AI-driven diagnostics are revolutionizing early detection, allowing for quicker, more accurate diagnoses and enabling doctors to implement personalized treatment plans faster. Additionally, research into microbiome-based treatments is gaining traction, as scientists explore how the gut microbiome influences cancer progression and therapy response. This emerging area may lead to new therapeutic approaches that can enhance treatment outcomes. Personalized cancer vaccines are also a significant area of research, aiming to trigger the immune system to target specific cancer cells, offering tailored treatments for individual patients. Liquid biopsy techniques, another breakthrough, allow for non-invasive cancer detection by analyzing blood samples for cancer-related biomarkers. This innovation could dramatically improve early detection and monitoring of gastric cancer without the need for invasive procedures. Furthermore, the rise of next-generation sequencing (NGS) is playing a pivotal role in enhancing molecular profiling, offering insights into the genetic makeup of tumors. NGS enables more precise, tailored treatment strategies based on the unique characteristics of each patient’s cancer. Companies are also investigating novel drug delivery systems to enhance the efficacy of treatments while minimizing side effects. These innovative delivery methods aim to ensure that drugs reach the target areas more effectively, reducing systemic toxicity and improving the overall treatment experience. Together, these advancements are transforming the gastric cancer landscape, offering promising new avenues for diagnosis and treatment.

Key Players

-

Merck & Co.

-

Bristol-Myers Squibb

-

Roche

-

Eli Lilly

-

Pfizer

-

AstraZeneca

-

Novartis

-

Amgen