GLOBAL GALLBLADDER CANCER MARKET (2024 - 2030)

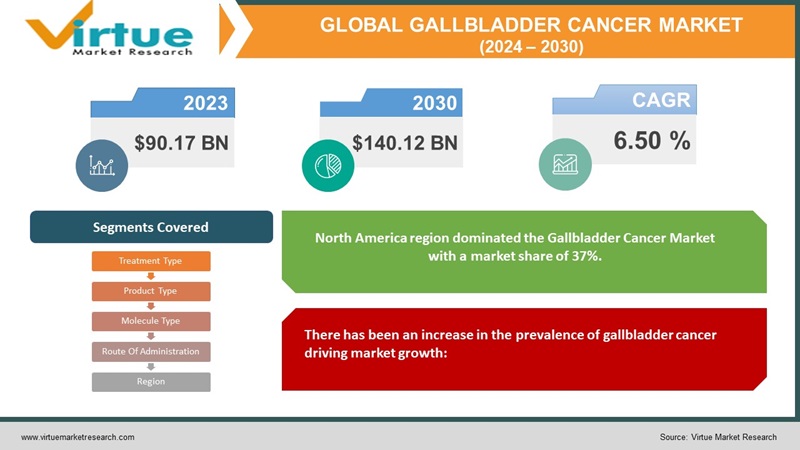

The Gallbladder Cancer Market was valued at USD 90.17 million in 2023 and is projected to reach a market size of USD 140.12 million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CThe lackAGR of 6.50%.

The gallbladder is a small pear-shaped organ located below the liver of an individual. This organ allows bile to be transferred through a duct into the small intestine. A lot of people get affected by gallbladder disorders every year and millions of cases have turned fatal.

Key Market Insights:

A mass called a tumour is formed when healthy cells in the gallbladder start growing rapidly. A benign tumor will not spread. Malignant cells are found in the tissues of the gallbladder, which is a rare disease. The symptoms include nausea, vomiting, and pain in the abdomen. Blood tests, scans, and other tests can be used to diagnose bladder cancer.

Lack of a comprehensive treatment method for gallbladder cancer, along with the longer duration of the treatment, are some of the major factors restraining the growth of the global gallbladder cancer treatment market.

According to the Centers for Disease and Control Prevention, Cigarette smoking remains the most primary and common cause of preventable disease such as cancer, disability, and death in the United States. In 2023, it released a report which stated that of those who ever tried e-cigarettes, approximately half the population of them are currently using them, indicating that they remain e-cigarette users contributing to the global cancer market.

Gallbladder Cancer Market Drivers:

There has been an increase in the prevalence of gallbladder cancer driving market growth:

The gallbladder cancer market is growing due to the rising incidence of the disease. Rates have been rising over the past few decades for a relatively rare cancer. According to data published by the Cancer Council Victoria, there were almost 300 cases of gallbladder cancer in the state. There were 140 males and 148 females.

The geriatric population is growing increasing the prevalence of diseases and cancer risks:

The growing geriatric population is driving the gallbladder cancer market. Incidence rates peak in the sixth and seventh decade of life for bladder cancer. The global population of people over the age of 65 is projected to grow to 50 billion by the year 2050, according to the United Nations. Increasing demand for gallbladder cancer diagnostics and treatments is expected to be driven by the rapidly aging global population.

Gallbladder Cancer Market Restraints and Challenges:

According to statistics from the World Health Organization, gallbladder and biliary tract cancers are among the 10 most expensive cancers to treat in terms of initial workup and primary treatment costs. Depending on the extent of surgery and hospitalization charges in different countries, a surgery to remove the gallbladder alone costs anywhere between US$ 20,000 to US$ 50,000. The costs of pre- surgical tests can cumulatively exceed US $10,000. Patients need treatment after surgery. The cost of a single cycle of gemcitabine is between US$ 3000 and US$ 10,000. Patients need 20 to 30 sessions of radiation therapy and the cost is between 100 and 500 dollars per session. The hospital stays add to the costs.

The US FDA and European Medicines Agency have approved limited targeted agents for this indication despite research into the causes of gallbladder cancer. Despite the prevalence of FGFR fusions, only one FGFR inhibitor has been approved so far. It is not widely used to identify potential targets. Market growth is hindered by lack of regulatory approved targeted therapies for advanced gallbladder cancer cases.

Gallbladder Cancer Market Opportunities:

There is a lot of unmet need. According to the data published by the American Society of Clinical Oncology, there will be 4,510 deaths from gallbladder and other biliary cancers in the US in 2023.

Increase in healthcare manufacture and growing medical tourism in emerging markets provides multiple significant growth for gallbladder cancer treatment manufactures.

Individualized treatments based on the genetic profile of individual patients are possible with the advancement of precision medicine. Treatments for gallbladder cancer can be improved with the development of targeted therapies.

GLOBAL GALLBLADDER CANCER MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6.50%

|

|

Segments Covered

|

By Product Type, Treatment Type, Route Of Administration, Molecule Type and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Eli Lilly and Company, Bristol-Myers Squibb

Roche, Pfizer, Novartis, Merck & Co., Inc.

Sanofi, AstraZeneca, AbbVie, Gilead Sciences

|

Gallbladder Cancer Market Segmentation:

Market Segmentation: By Product Type:

- Mono Therapy

- Combination Therapy

- Mono/Combination Therapy

Combination therapy is the leading segment and fastest growing segment is Mono therapy. Gemcitabine-cisplatin (Gem/Cis) is the most used combination therapy with market share around 50% in 2023. Overall survival and response rates have been shown to be superior with this combination.

There are factors contributing to dominance:

Efficacy is proven: The adoption of Gem/Cis as the standard of care for advanced gallbladder cancer is due to its consistent and superior efficacy in clinical trials.

There are synergistic effects: The combination of gemcitabine, a nucleoside analog, and cisplatin, a Platinum-based agent, produces synergistic effects, enhancing tumor cell killing.

There is a tolerability profile: Gem/Cis is suitable for a broader patient population because it is well-tolerated and has manageable side effects.

Guidelines are established: Gem/Cis is recommended as the first-line treatment for advanced gallbladder cancer, solidifying its dominance in the market.

Combination therapy consist of combining two or more drugs or different type of therapies. By discovering clever new combinations that aim to treat cancer in different ways, we can stop it from developing resistance early on. Drug resistance is one of the biggest challenges we face in cancer research. New targeted drugs have helped improve the lives of cancer patients. Cancer can become resistant to these drugs; we need to find different methods and ways to make them work. One way to see if different combinations of treatments will work better is to give them at the same time. This can include treating patients with several drugs that work by different mechanisms or re-sensitizing cancer to an original treatment by giving the patient another therapy.

The combination of gemcitabine and cisplatin has changed the treatment of gallbladder cancer. The overall treatment landscape has been impacted by its dominance in the market and has set an standard for the treatment expectations as a result patients now have more hope that they can recover faster as a result it creates a positive market for the key players.

Mono therapies are often effective as for first line of treatment, and combination therapies are typically reserved for the patients. Since the treatment by mono/combination therapy is very expensive as a result people cannot afford it and leads to less adoption of curing method.

Market Segmentation: By Treatment Type:

- Surgery

- Radiation therapy

- Chemotherapy

- Immunotherapy

- Targeted Therapy

Chemotherapy is the leading segment in gallbladder cancer and fastest growing segment is Targeted Therapy. The factors responsible are prevalence of cancer in the entire world, as number of cases for cancer is growing across the globe which leads to bring advancement in the treatment of cancer.

Chemotherapy kills cancer cells wherever they are in the body with a combination of drugs. Chemo may be given before surgery to shrink a gallbladder tumour. Neoadjuvant therapy is a type of therapy.

With an estimated 50% share, gemcitabine is the leading chemotherapy agent for gallbladder cancer. Its dominance is due to its consistent and superior efficacy in clinical trials, favorable tolerability profile, and cost-effectiveness. Treatment decisions, clinical research, treatment cost dynamics, and patient treatment expectations have been influenced by Gemcitabine's position as the standard of care.

With an estimated market share of 15% in 2023, peclitaxel has emerged as a rapid-growing targeted therapy for gallbladder cancer. Its dominance is due to its synergistic effect with gemcitabine.

A paradigm shifts in gallbladder cancer treatment, influenced clinical trial design, raised patient treatment expectations, and driven healthcare resource allocation are some of the things that Paclitaxel has contributed to.

Market Segmentation: By Route of Administration:

- Oral

- Intramuscular

- Intravenous

- Intertumoral (IT)

IVs are most common way to give treatment to cancer patient as the drug directly goes through vein and mix with blood stream and thus takes less time to show its effect on cancer patient’s body. Oral is the fastest growing segment, secondly drug given orally are digested by digestive system and can reach cancer cells throughout the body. Intra tumoral is method where drugs are directly injected into tumor such treatment is preferred only when tumor is small and confined to gallbladder.

IV administration has emerged as the dominant route of administration for gallbladder cancer treatment due to its uniform drug distribution, controlled dose delivery, convenience, and established efficacy. Drug development, clinical trial design, and healthcare resources have been influenced by this dominance.

Due to its convenience, reduced treatment burden, and emerging treatment options, oral administration for gallbladder cancer is gaining traction.

Market Segmentation: By Molecule Type:

- Monoclonal Antibody

- Peptides

- Polymer

- Small molecule

Monoclonal Antibody (mABs) are proteins that are man-made which specifically target and bind to particular molecule cancer cell. Their role is to deliver toxins directly to cancer cells this type of mAB is known as antibody-drug conjugate (ADC). The attached toxin kills the cancer cell when the mAB binds with them. mABs are the fastest growing segment.

Small Molecules have emerged as the dominant force in the market for gallbladder cancer treatment, taking 80% of the market share. Their dominance is due to a combination of favorable properties that have made them the preferred choice for patients and oncologists.

The advantage of small molecule drugs is that they allow for convenient administration without the need for injections. Their delivery mechanism reduces side effects and improves treatment efficacy.

Small molecule types have a cost-effective advantage compared to other molecule types, making them an attractive option for healthcare providers and payers. Small molecules have demonstrated superior efficacy in clinical trials, solidifying their position as the standard of care for gallbladder cancer treatment.

Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

In 2023, North America region dominated the Gallbladder Cancer Market with a market share of 37%. The high rate of gallbladder disease in North America, combined with the presence of advanced treatment choices and favourable reimbursement policies, is driving business sector development around here.

The interplay of clinical considerations, patient preferences, and healthcare resource utilization can affect treatment dominance in US gallbladder cancer. Clinical factors include proven efficacy, manageable side effects, disease stage, and patient comorbidities. Patient preferences are influenced by convenience, cost-effectiveness, informed consent, and provider expertise.

Resource utilization is determined by availability, accessibility, reimbursement, and provider expertise. Understanding these factors can help healthcare professionals make better treatment decisions.

However, the Asia-Pacific region is anticipated to grow at the fastest CAGR of about 6.50% during the forecast period. Asian countries are seen as the top choice for medical tourism and travel owing to the low cost of treatments. As a result, it is boosting the growth of the market in the Asia-Pacific region. The Asia-Pacific gallbladder cancer treatment market is projected to surge due to rising incidence, improved diagnostics, growing awareness, expanding healthcare infrastructure, and economic growth. Diagnostic techniques and new treatment options are extending the lifespan of patients.

COVID-19 Impact Analysis on the Gallbladder Cancer Market:

The outbreak of the COVID-19 Pandemic in the US led to radical changes in medical procedures and treatments. Clinical trials related to gallbladder cancer were negatively affected by the Pandemic. Cancer therapy is an essential treatment. Vendors were compelled to develop new business strategies due to the outbreak. The market growth in North America will be driven by the relaxation of restrictions in various countries in the region.

People with gallstones are more likely to have gangrene in COVID patients. Because gallbladder cells have a high concentration of ACE2 and are similar to bile duct cells, they can be a target for the body's immune response to the virus. This isn't the first time that gangrene has been reported. During the peak of the second wave, there were cases of gangrene discovered in patients who had recovered from COVID. The lungs are the primary site of COVID-19 because they have the most ACE2 receptors, which the virus uses to bind human cells. Doctor issued warning stating that high level of inflammation unleashed by the SARS-COV-2 virus increases the risk of gangrene.

Latest Trends/ Developments:

The market players are increasing their research and development activities.

The market is expected to grow due to increasing research and development activities by the market players. On September 5, 2022, a pharmaceutical company received approval for a drug in the U.S. for the treatment of patients that are suffering from metastatic biliary tract cancer.

Key Players:

- Eli Lilly and Company

- Bristol-Myers Squibb

- Roche

- Pfizer

- Novartis

- Merck & Co., Inc.

- Sanofi

- AstraZeneca

- AbbVie

- Gilead Sciences

- In October 2023, Regeneron Pharmaceuticals, Inc., a pharmaceutical company, announced regimen of PD-1 inhibitor Libtayo (cemiplimab) as a neoadjuvant monotherapy for stage II to IV resectable Cutaneous Squamous Cell Carcinoma (CSCC).

In June 2023, Sirnaomics announced the advancement of STP705 for the treatment of isSCC in situ into late-stage clinical development.