Fly Ash Market Size (2024 – 2030)

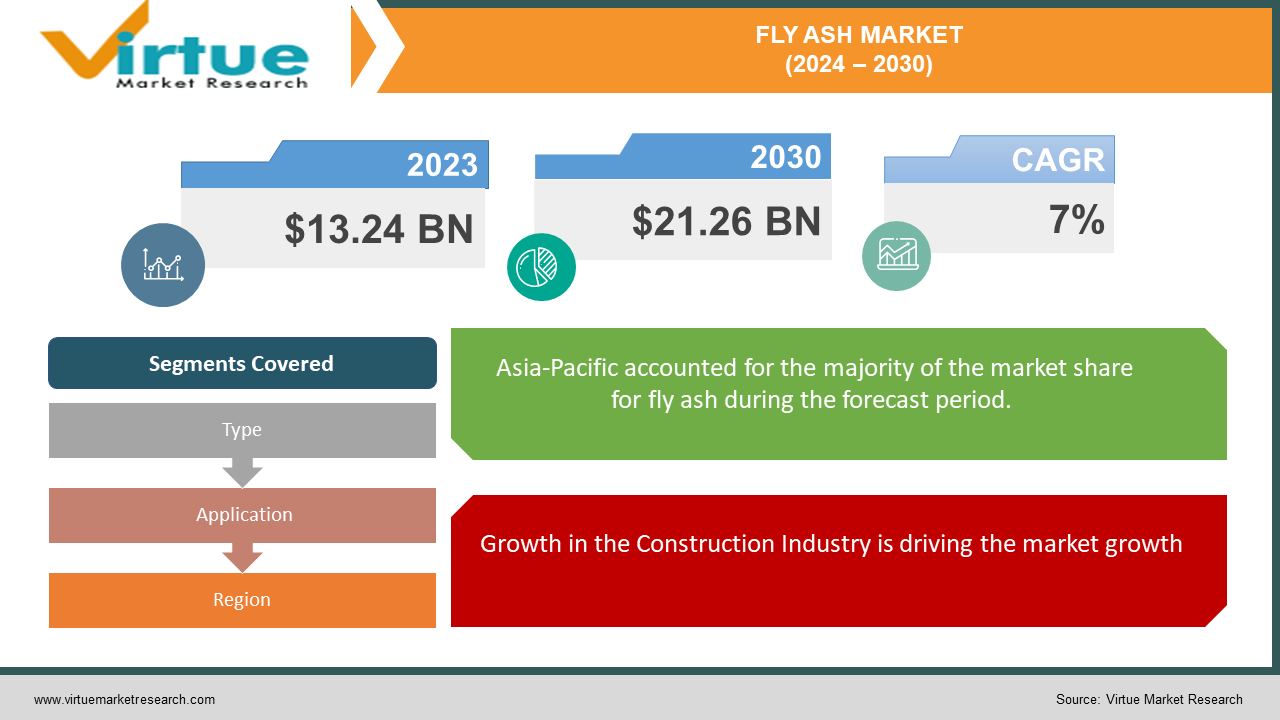

The Global Fly Ash Market was valued at USD 13.24 billion in 2023 and will row at a CAGR of 7% from 2024 to 2030. The market is expected to reach USD 21.26 billion by 2030.

The Fly Ash (DRMS) market is thriving, driven by rising energy costs and the spread of smart grids. These systems help balance electricity supply and demand by encouraging consumers to adjust their usage during peak hours. This market is expected to surpass $21 billion by 2030, with significant growth coming from Asia-Pacific regions like India and Japan.

Key Market Insights:

Asia-Pacific currently holds a 37.7% share of the fly ash market. This is due to the booming construction industry, particularly in developing giants like China and India.

Fly ash utilization offers significant environmental benefits. It helps reduce the environmental footprint of the construction industry by minimizing reliance on virgin materials like cement and also aids in managing the ever-growing amount of fly ash generated from coal-fired power plants.

Inconsistent and poor-quality fly ash can hamper market growth. This necessitates stricter regulations and quality control measures to ensure the effectiveness and reliability of fly ash in construction applications

Global Fly Ash Market Drivers:

Growth in the Construction Industry is driving the market growth

The global construction frenzy, particularly in developing economies like China and India, is a key driver propelling the fly ash market. Fly ash acts as a secret weapon for concrete, significantly enhancing its strength, workability, and durability. This translates to superior buildings, roads, and bridges that can withstand the test of time. As construction projects mushroom, the demand for fly ash rises in a proportional dance. But fly ash isn't just an inert filler; it plays a vital functional role. By filling the gaps between cement particles, fly ash improves the flow of concrete during mixing and pouring, making it easier to handle by construction crews. Once cured, concrete containing fly ash transforms into a remarkably strong and crack-resistant material, ensuring the longevity of structures. This perfect synergy between fly ash's properties and the construction industry's needs creates a mutually beneficial relationship, fueling the growth of the fly ash market.

Improved Infrastructure Development is driving the market growth

Governments worldwide are prioritizing infrastructure development, and this translates directly to a surge in fly ash demand. Think roads, bridges, dams – all these crucial structures require massive quantities of concrete. As these infrastructure projects gain momentum, fueled by government spending, the need for fly ash rises proportionally. But it's not just about quantity; fly ash offers a performance boost too. By partially replacing cement in concrete mixes, fly ash enhances the final product's strength and durability. This translates to longer-lasting infrastructure, reducing the need for frequent repairs and replacements. Furthermore, using fly ash contributes to a more sustainable approach to construction. This synergy between infrastructure development, fly ash's performance benefits, and its role in sustainable construction creates a perfect storm driving the fly ash market forward.

Cost-effectiveness is driving the market growth

One of the key drivers of the fly ash market is its cost-effectiveness. Unlike traditional concrete ingredients, fly ash isn't a virgin material; it's a byproduct of coal combustion in power plants. This translates to a significant price advantage compared to materials like Portland cement. Construction projects benefit tremendously from this cost savings. Using fly ash as a partial replacement for cement reduces the overall material cost without compromising quality. Additionally, fly ash often requires less water during concrete mixing, leading to further cost reductions. This economic benefit is particularly attractive in developing regions where infrastructure projects are booming. By utilizing fly ash, construction companies can stretch their budgets further, building more sustainable and cost-effective structures. This win-win scenario for both the environment and the construction industry paves the way for continued growth in the fly ash market.

Global Fly Ash Market challenges and restraints:

Decreasing Reliance on Coal-Fired Power Plants is restricting the market growth

The green shift is posing a challenge to the Fly Ash Market. As countries prioritize renewable energy sources like solar and wind to minimize their environmental impact, coal-fired power plants are being phased out. This directly translates to a decline in fly ash production. Fly ash is a byproduct of coal combustion, so less coal burned means less fly ash generated. This decline in supply disrupts the flow of fly ash to the construction industry, which relies on it for concrete production. Finding alternative uses or ways to utilize stockpiled fly ash will be crucial to navigate this challenge and ensure a sustainable future for the fly ash market.

Environmental and Health Concerns are restricting the market growth

Fly ash casts a double shadow. While it boasts economic and performance benefits in concrete, its environmental and health concerns are a cause for wariness. Fly ash can harbor harmful trace elements like arsenic, mercury, and lead. If not handled and disposed of properly, these toxins can be released into the environment through air or water contamination. This can pose serious health risks to nearby communities, causing respiratory problems and even impacting long-term health. Recognizing these potential dangers, stricter regulations are being imposed on fly ash use. Governments are mandating proper storage and transportation protocols to minimize the risk of exposure. Additionally, research is ongoing to develop methods for removing these harmful elements from fly ash, paving the way for its safer and more sustainable utilization in the construction industry. The future of fly ash hinges on finding a way to balance its benefits with stringent environmental and health safeguards.

Market Opportunities:

The fly ash market brims with exciting opportunities. Burgeoning infrastructure development in emerging economies presents a vast potential for fly ash utilization in concrete production. Furthermore, increasing environmental regulations are pushing construction companies towards sustainable practices, creating a significant demand for fly ash as a cost-effective and eco-friendly alternative to cement. Innovation in developing new applications for fly ash, such as lightweight aggregates and geopolymers for construction, can further expand the market's reach. Additionally, research on utilizing fly ash in soil stabilization and agricultural applications presents promising opportunities for market diversification. By addressing quality control concerns and establishing clear regulations, stakeholders can unlock the full potential of fly ash and promote its wider adoption across various industries.

FLY ASH MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

7% |

|

Segments Covered

|

By Type, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Boral Limited, Cemex S.A.B. de C.V., LafargeHolcim Ltd., Waste Management, Inc., Charah Solutions, Inc., Separation Technologies LLC (Titan America LLC), Cement Australia Pty Limited, Salt River Materials Group, Southeastern Fly Ash Company, Tarmac Holdings Limited

|

Fly Ash Market Segmentation - By Type

-

Class F Fly Ash

-

Class C Fly Ash

Class F currently reigns supreme in the market. This dominance can be attributed to several factors. Firstly, Class F's lower calcium content translates to slower setting times, which allows for better workability and easier handling of the concrete mix during construction. Secondly, the lower heat generation during curing with Class F ash minimizes the risk of cracking in large concrete structures. These advantages, coupled with the widespread availability of anthracite and bituminous coal compared to lignite or sub-bituminous sources, make Class F the more dominant choice in the fly ash market. However, it's important to note that Class C fly ash can be a viable alternative in specific scenarios where faster setting times and improved early strength development are crucial for construction projects

Fly Ash Market Segmentation - By Application

-

Cement & Concrete

-

Bricks & Blocks

-

Road Construction

-

Agriculture

Cement & Concrete segment reigns supreme in the fly ash market application landscape. This dominance stems from several key factors. Firstly, concrete production consumes a vast amount of cement, and fly ash acts as a cost-effective partial replacement, offering substantial economic benefits for construction projects. Secondly, fly ash demonstrably enhances concrete properties. Its addition improves workability, increases strength and durability, and even reduces the risk of cracking. These combined advantages make fly ash an indispensable component in modern concrete production, solidifying its position as the dominant application segment in the fly ash market. While fly ash has promising applications in other areas like bricks and road construction, their overall market share pales in comparison to the massive volume of fly ash utilized in the concrete industry.

Fly Ash Market Segmentation - Regional Analysis

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

The Asia-Pacific region reigns supreme in the Fly Ash Market. This dominance is fueled by a booming construction industry, particularly in developing giants like China and India. These countries are experiencing rapid urbanization and massive infrastructure projects, all demanding vast quantities of concrete. Fly ash, with its cost-effectiveness and concrete-enhancing properties, becomes an attractive choice for construction companies in this region. Additionally, stricter regulations on landfill use are pushing for the utilization of fly ash as a sustainable alternative in concrete production. This confluence of factors has solidified Asia-Pacific's position as the dominant market for fly ash.

COVID-19 Impact Analysis on the Global Fly Ash Market

The COVID-19 pandemic delivered a temporary blow to the Fly Ash Market in 2020. Lockdowns and restrictions on movement stalled various construction projects globally, leading to a sharp decline in demand for fly ash. This coincided with a decrease in fly ash production as some coal-fired power plants temporarily reduced operations. However, the market exhibited resilience, with a rebound in demand observed in 2021 as construction activities resumed. Government stimulus packages focused on infrastructure development in many regions further bolstered the demand for fly ash. Additionally, a growing focus on sustainable construction practices has renewed interest in fly ash as a cost-effective and eco-friendly alternative to virgin materials. While the long-term impact of the pandemic on coal consumption and fly ash production remains uncertain, the Fly Ash Market is expected to experience moderate growth in the coming years, driven by the ongoing construction boom, particularly in developing economies, and increasing environmental regulations promoting the utilization of fly ash.

Latest trends/Developments

The Fly Ash Market is experiencing a period of both opportunity and challenge. On the positive side, there's a growing appreciation for fly ash's role in sustainable construction. As awareness rises, particularly in developing economies like China and India, the construction boom is driving demand for fly ash. Here, fly ash shines as a cost-effective and performance-enhancing ingredient for concrete, translating to stronger, more durable buildings and infrastructure. Additionally, stricter regulations on landfill use are pushing for fly ash as a viable alternative, promoting its environmental credentials.

However, the market faces headwinds. The global shift towards renewable energy sources like solar and wind is leading to a decline in coal-fired power plants, the primary source of fly ash. This decrease in supply disrupts the flow of fly ash to the construction industry. Researchers are exploring ways to utilize stockpiled fly ash and develop methods to extract harmful elements like arsenic from fly ash, ensuring its safe and sustainable use. Another challenge is the environmental and health concerns surrounding fly ash. Stringent regulations are being imposed on fly ash handling and disposal to minimize the risk of exposure to toxins.

Overall, the Fly Ash Market presents a complex picture. Finding innovative ways to address these challenges will be crucial to ensure a sustainable future for this market. This might involve developing alternative uses for fly ash, creating more efficient transportation methods, and implementing stricter environmental safeguards throughout the fly ash lifecycle.

Key Players:

-

Boral Limited

-

Cemex S.A.B. de C.V.

-

LafargeHolcim Ltd.

-

Waste Management, Inc.

-

Charah Solutions, Inc.

-

Separation Technologies LLC (Titan America LLC)

-

Cement Australia Pty Limited

-

Salt River Materials Group

-

Southeastern Fly Ash Company

-

Tarmac Holdings Limited