Fabric Blade Wind Turbine Market Size (2024 –2030)

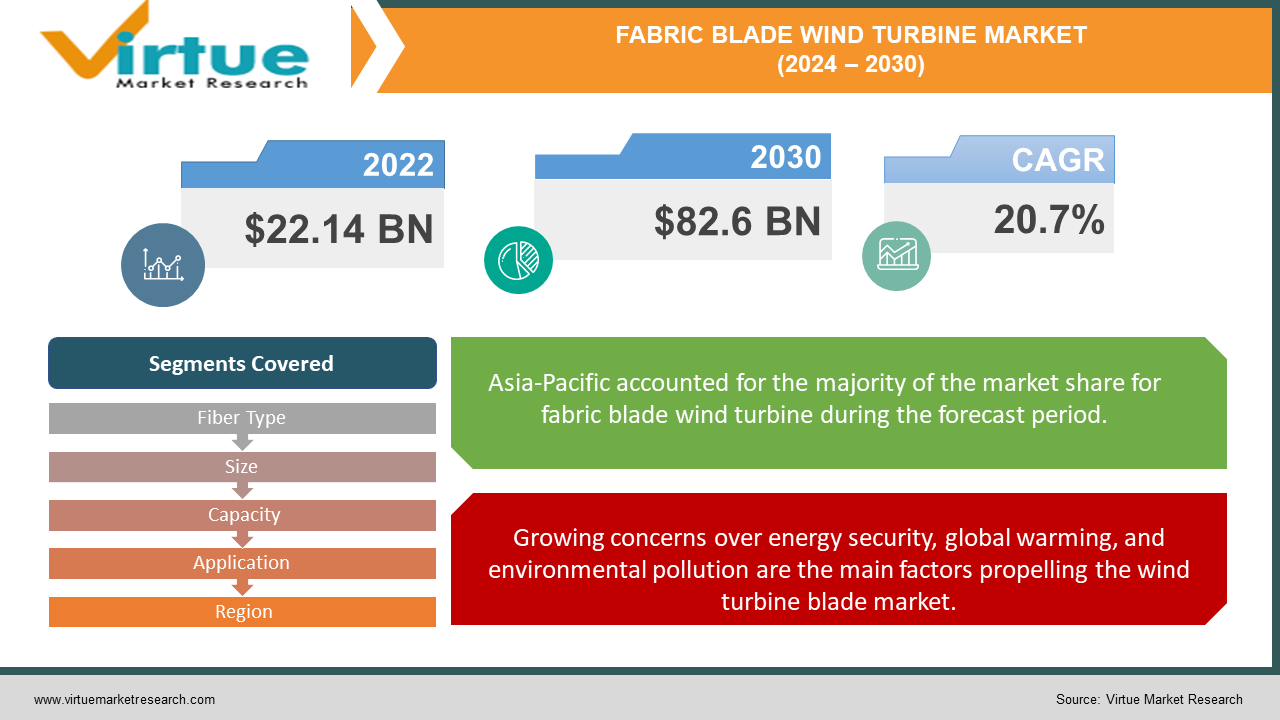

The Global Fabric Blade Wind Turbine Market was estimated to be worth USD 22.14 billion in 2023 and is projected to reach a value of USD 82.6 billion by 2030, growing at a CAGR of 20.7% during the forecast period 2024-2030.

Composite materials are essential for creating components with longer lifespans because of their lightweight and durable characteristics. These materials are especially used in the construction of nacelles, rotors, and blades, which are important components of wind turbines. The increasing number of wind turbines being installed worldwide, along with large government investments in renewable energy sources like solar and wind, is the main driver of the demand for composite materials. The industry is expanding even more thanks to government programs that highlight offshore wind energy projects. But obstacles like the exorbitant cost of carbon fiber and epoxy resin, combined with the challenges of recycling composites, might prevent the market from growing much shortly.

Key Market Insights:

Fabric blades have the potential to save wind turbine costs by 25–30% when compared to conventional fiberglass/carbon fiber blades.Prototypes of current fabric blades have shown that they can attain more than 95% of the aerodynamic efficiency of traditional rigid blades.Using fabric blades can save about 4-6 metric tons of weight per blade for a standard 2 MW wind turbine.If fabric blades prove to be economically feasible, it is projected that they could account for approximately 10% of the yearly demand for new wind turbine blades by 2030.

Global Fabric Blade Wind Turbine Market Drivers:

Growing concerns over energy security, global warming, and environmental pollution are the main factors propelling the wind turbine blade market.

Concerns about climate change and the need for sustainable power are driving up the use of renewable energy sources, which is driving up demand for wind turbine blades. Globally, governments are promoting the growth of wind energy projects by providing advantageous policies and incentives for renewable energy projects. The energy output and performance of turbines have increased due to advancements in blade technology, which include longer and more efficient blades. This has reduced the cost of wind power. Furthermore, the demand for bigger, more robust blades made especially for offshore use is being driven by investments in offshore wind projects, especially in areas with abundant wind resources.

The market for wind turbine blades benefits from increased wind power generation.

Thanks to developments in wind turbine technology, wind energy generation has emerged as a significant global source of electricity. The power, efficiency, and cost-effectiveness of wind turbines have increased, resulting in a significant rise in the global capacity for wind power. Demand for wind turbine blades, which are essential parts of wind energy systems, has increased as a result of this growth. Wind energy currently accounts for nearly half of all newly installed electricity generation capacity worldwide. The market is expanding due to government initiatives that support the use of renewable energy for environmental sustainability. Another important factor driving the growth of the wind power market is the declining cost of producing wind energy. The market for materials used in wind turbine blades is anticipated to be greatly impacted by investments in clean energy programs and incentives, which will promote the advancement of renewable energy sources.

Fabric Blade Wind Turbine Market Challenges and Restraints:

Because of their size and weight, wind turbine blades are difficult and expensive to transport, requiring specialized equipment and infrastructure. Significant upfront costs and sophisticated manufacturing techniques are also required in the production of these blades, which may hurt profitability and restrict market growth. The construction of wind turbine blades is further complicated by strict regulations on noise emissions and environmental impacts, which require strict adherence to guidelines and standards.

Fabric Blade Wind Turbine Market Opportunities:

There are numerous prospects for expansion and development in the fabric blade wind turbine market. The growing need for renewable energy sources, particularly wind power, due to environmental concerns and the need to lessen dependency on fossil fuels, represents a significant opportunity. A favorable market environment for fabric blade wind turbines is produced by this demand. Furthermore, new developments in materials science and technology present chances for creative and better fabric blade design, resulting in wind turbines that are stronger and more effective. Government programs and policies that encourage the development of renewable energy sources by offering financial incentives and subsidies for wind power projects present another opportunity. New opportunities for market expansion are also presented by the growth of offshore wind farms and the requirement for specialized fabric blades that are optimized for offshore conditions.

FABRIC BLADE WIND TURBINE MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

20.7% |

|

Segments Covered

|

By Fiber Type, Size, Capacity, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

TPI Composites Inc, Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd, LM Wind PowerNordex, Siemens Gamesa Renewable Energy, Vestas Wind Systems, MFG WindSinoma Wind Power Blade Co. Ltd, Aeris Energy, Suzlon Energy Limited, Enercon GmbH

|

Global Fabric Blade Wind Turbine Market Segmentation: By Fiber Type

Glass fiber-reinforced plastics hold a dominant market share of over 55% in the wind turbine composite materials market. Given glass fiber's superior strength, resilience to weather, lightweight nature, and weather resistance, this market is anticipated to expand rapidly over the projection period. The use of glass fiber-reinforced plastics in wind turbine manufacturing is motivated by their accessibility and affordability. Furthermore, the carbon fiber market is expected to grow significantly throughout the forecast period due to the properties of carbon fiber, which include high rigidity, low thermal expansion, heat resistance, and chemical resistance.

Global Fabric Blade Wind Turbine Market Segmentation: By Size

-

Up to 27 Meters

-

28-37 Meters

-

38-50 Meters

-

More Than 50 Meters

Four size categories make up the wind turbine blade market: up to 27 meters, 28–37 meters, 38–50 meters, and more than 50 meters. Due to their higher efficiency and lower cost, wind turbine blades larger than 50 meters in size brought in the most revenue (70.4%) of any category. However, blades up to 27 meters in size are predicted to grow at the fastest rate. Increased investment and modifications to wind energy-friendly government regulations are the main drivers of this growth.

Global Fabric Blade Wind Turbine Market Segmentation: By Capacity

-

Less Than 2 MW

-

2 MW-5 MW

-

5 MW

Based on capacity, the wind turbine blade market is divided into three segments: under 2 MW, 2 MW to 5 MW, and above 5 MW. The market is dominated by the 2 MW to 5 MW category, which makes wind power suitable for a wide range of applications, from modest residential to massive industrial setups. However, the over 5 MW segment is growing at the fastest rate due to growing environmental concerns and the shift away from fossil fuels.

Global Fabric Blade Wind Turbine Market Segmentation: By Application

Onshore and offshore are the two application segments that make up the wind turbine blade market. Because more offshore wind turbines are being used, which raises the demand for wind turbine blades, the offshore segment brought in the most revenue (70.4%). On the other hand, due mostly to the rising demand for wind energy on land, the onshore segment is anticipated to grow at the fastest rate during the forecast period.

Global Fabric Blade Wind Turbine Market Segmentation: By Region

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

The Asia-Pacific (APAC) region held the largest share of the wind turbine blade market in 2023, accounting for nearly 45% of the total, and is predicted to grow at a rapid rate in the years to come. The rising demand for renewable energy, the need for robust and lightweight materials to produce turbines, and government initiatives that encourage the development of wind power are the main drivers of this growth. Due to rising government support for renewable energy, rising wind power demand, and increased private investment, the wind turbine blade market in North America is also expected to grow significantly over the forecast period. Cost pressures, on the other hand, may present difficulties for the Americas' industry, affecting investment thresholds and economic growth.

COVID-19 Impact on the Global Fabric Blade Wind Turbine Market:

In the beginning, the COVID-19 pandemic led to supply chain problems and delays in the market for wind turbine blades. The market's long-term outlook is still favorable, though. Following the pandemic, the renewable energy sector—which includes wind energy—is anticipated to be vital to economic recovery and green stimulus initiatives. There will probably be more financing and development for wind energy projects as nations put more emphasis on decarbonization and the demand for sustainable energy sources rises, which will cause the market for wind turbine blades to grow significantly.

Latest Trend/Development:

Recent advancements in blade materials and design to increase efficiency and lower costs are among the trends and developments in the fabric blade wind turbine market. New composite materials and fabrication methods are being investigated by manufacturers to produce lighter, more robust blades that will enhance turbine performance and dependability. Larger and more effective wind turbines for offshore applications are also a growing area of focus, necessitating creative blade designs that can survive challenging marine conditions. To maximize efficiency and minimize downtime, another trend in wind turbine technology is the integration of smart technologies, such as sensors and predictive maintenance systems. In conclusion, there is a growing focus on adopting sustainable manufacturing techniques to reduce the ecological footprint associated with the production and disposal of blades. All of these trends work together to propel the fabric blade wind turbine market's expansion and sustainability.

Key Players:

-

TPI Composites Inc

-

Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

-

LM Wind PowerNordex

-

Siemens Gamesa Renewable Energy

-

Vestas Wind Systems

-

MFG WindSinoma Wind Power Blade Co. Ltd

-

Aeris Energy

-

Suzlon Energy Limited

-

Enercon GmbH

Market News:

-

Vestas delivered the first 115.5-meter blade made especially for the V236-15.0 MW offshore wind turbine with success in October 2023. This blade was made at Vestas' production facility in Nakskov, Denmark, using a mold made at their Lem plant in Denmark.

-

Hitachi Power Solutions unveiled Blade Total Service, a new range of cutting-edge services, in March 2022. This service uses drones, AI, and digital technologies to lower the risks related to installing wind turbines. It addresses problems like damage from lightning, high winds during storms, and wear and tear on blades.