Europe District Cooling Market Size (2024-2030)

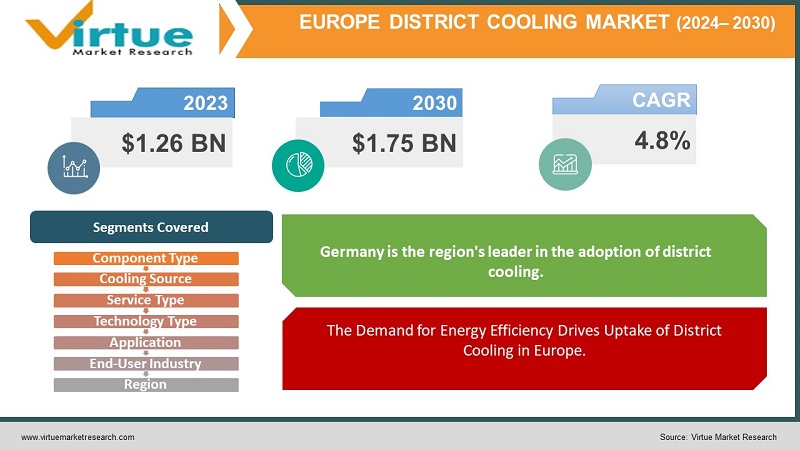

The market for Europe district cooling market is expanding quickly; it was estimated to be worth USD 1.26 billion in 2023 and is expected to increase to USD 1.75 billion by 2030, with a projected compound annual growth rate (CAGR) of 4.8% from 2024 to 2030.

To meet the continent's growing demand for efficient and durable cooling solutions, the European district cooling market is a thriving and rapidly expanding sector of the economy. With the increased focus on energy efficiency, urban planning, and environmental sustainability, district cooling systems have gained popularity in commercial, industrial, and residential contexts. The industry encompasses a wide range of components, such as pumps, pipelines, chillers, and thermal energy storage, and serves several end-user sectors, including apartment buildings, retail stores, and industrial facilities. Moreover, district cooling systems that use renewable energy sources align with Europe's goal of reducing carbon emissions and promoting green technologies. The market is influenced by governmental regulations, technological advancements, and the ongoing transition to more environmentally friendly energy sources.

Key Market Insights:

A complete understanding of the market dynamics both now and in the future is provided by significant market insights into the European district cooling industry. The market's notable rise may be attributed to several factors, including the growing need for cooling systems across various industries, government initiatives encouraging energy-efficient solutions, and rising environmental consciousness. The end-user industries—commercial, industrial, and residential—are used to segment the market, revealing distinct trends and preferences within each industry. Using renewable energy sources is one significant trend in district cooling infrastructure that is expanding. This trend is in keeping with the greater European objectives of minimising carbon footprints. Enhancements in technology for components such as pumps, pipes, and chillers also contribute to optimising

system performance.

Policies and regulatory frameworks play a critical role in shaping the market, influencing investment decisions, and promoting innovation. As the market grows, the frequency of strategic alliances, mergers, and acquisitions is increasing, signifying the industry's efforts to integrate and take advantage of new prospects. To make informed decisions, adapt to evolving trends, and support the sustainable development of the European district cooling business, stakeholders must continuously keep an eye on these critical market insights.

Europe District Cooling Market Drivers:

The Demand for Energy Efficiency Drives Uptake of District Cooling in Europe.

Policies and regulatory frameworks play a critical role in shaping the market, influencing investment decisions, and promoting innovation. As the market grows, the frequency of strategic alliances, mergers, and acquisitions is increasing, signifying the industry's efforts to integrate and take advantage of new prospects. To make informed decisions, adapt to evolving trends, and support the sustainable development of the European district cooling business, stakeholders must continuously keep an eye on these critical market insights.

Smart Cities Succeed The Contribution of District Cooling to Europe's Urban Renaissance.

Towns around Europe are starting to embrace the idea of "smart cities," and district cooling systems are thought to be crucial to the development of effective, networked urban settings. The infrastructure, which serves the demands of business districts, industrial zones, and densely populated areas, guarantees a sustainable and centralised approach to cooling. This strategic integration contributes to the rehabilitation of European metropolitan landscapes, in keeping with contemporary principles in urban planning.

Driven by Climate Resilience and Economic Viability, Europe's District Cooling Movement.

In Europe, district cooling systems are being adopted primarily due to their economic feasibility and climate resilience. Because of economies of scale, these systems not only provide a climate-resilient infrastructure but also yield significant financial and operational savings. The reliability and stability of district cooling will play a major role in how resilient European cities are to climate change, especially if extreme weather events become more common.

Europe District Cooling Market Restraints and Challenges:

Overcoming Financial Obstacles: Europe's District Cooling Industry Faces a Struggle Due to High Startup Expenses.

The potential growth trajectory of the district cooling market in Europe is impeded by high initial capital expenditures. Despite the long-term benefits of district cooling systems, their widespread availability is limited by the high initial expenses of infrastructure development. The sector has to work hard to attract stakeholders and investors who could be turned off by the substantial financial commitment. To overcome this challenge and make district cooling projects financially viable and attractive to sponsors, innovative funding methods and collaborative efforts will be needed.

Retrofitting Reality: Europe's District Cooling Market Struggles to Take Advantage of Limited Reuse of Current Infrastructure.

A significant barrier to the ambitious integration of district cooling systems into the current European infrastructure is the lack of retrofitting possibilities. The integration of district cooling is hindered by the financial and technical challenges that come with upgrading major urban regions and older structures. As cities strive for sustainability, retrofitting faces more and more difficulties that require innovative solutions and caution when balancing modernization with historic urban areas.

Climate Control Complexity: Seasonal Demand Fluctuations in Europe's District Cooling Market Addressed.

Managing seasonal variations in demand poses a distinct challenge to the European district cooling sector. The cooling sector has to deal with the challenges of supply and demand balancing throughout the year because cooling needs rise in the summer and decrease in the winter. Since controlling the complexity of seasonal variations is essential to preserving the district cooling systems' economic viability and efficient use, the industry is looking for ways to increase resilience and adaptation.

Europe District Cooling Market Opportunities:

Redefining Sustainability: The Integration of Renewable Energy Into Europe's District Cooling Market.

By seizing the opportunity to integrate sustainable energy sources, the European district cooling industry is taking a big step in the direction of sustainability. District cooling systems are beginning to contribute significantly to the reduction of carbon footprints and the achievement of Europe's ambitious clean energy targets. These systems utilise biomass, geothermal, and solar technology. In addition to having a positive impact on the environment, this paradigm-shifting action makes district cooling an essential part of the continent's transition to renewable energy sources.

Redefining Smart Cities: Europe's District Cooling Systems Leading the Way in Urban Efficiency.

The European district cooling market is redefining smart city concepts by implementing state-of-the-art technologies. Urban efficiency is raised when district cooling system integration is incorporated into smart city initiatives. Adaptive controls, predictive maintenance, and real-time monitoring are helping urban constructions become more energy-efficient and sustainable overall. Intelligent and sustainable urban living has advanced significantly with the combination of district cooling and smart cities.

Pioneering Energy Efficiency: Europe's District Cooling Market Explores Technological Advancements.

Thanks to continuous advancements in technology, the European district cooling industry is setting the standard for energy efficiency. The industry is investigating new types of chillers, pipe materials, and state-of-the-art control systems to significantly increase operating efficiency. By implementing these improvements, district cooling becomes a more enticing choice for consumers and aligns with Europe's larger focus on energy efficiency and sustainable development.

EUROPE DISTRICT COOLING MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

4.8%

|

|

Segments Covered

|

By Component Type, Cooling Source , Service Type, Technology Type , Application , End-User Industry , and Region

|

|

Various Analyses Covered

|

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

UK, Germany, France, Italy, Spain, Rest of Europe |

|

Key Companies Profiled

|

Siemens, Fortum, Helen Oy, Alfa level, Engie, Rasmboll A/S, Veolia, Goteborg Energy, Vattenfall AB, Wien Engine

|

Market Segmentation of Europe District Cooling Market:

Europe District Cooling Market Segmentation: By Component Type:

- Chillers

- Pipes

- Pumps

- Thermal Energy Storage

Pumps, pipes, thermal energy storage, and chillers are among the fundamental components that split the European district cooling market into multiple categories. The essential element of the cooling process, the chillers, remove heat from the circulated water or coolant. Pipes, the backbone of the district cooling system, enable the chilled water conveyance from the central cooling plant to the end users. Pumps are necessary to maintain the flow and pressure of chilled water throughout the system to offer efficient cooling. By storing excess energy during periods of low demand and utilising it during peak hours, thermal energy storage systems can enhance flexibility by boosting overall system resilience and efficiency.

Among these components, pumps stand out as being particularly important to preserving the effectiveness of the district cooling system. Pumps are essential for maintaining the optimum flow and circulation of chilled water, which optimises energy transfer and system performance. Pump performance optimisation reduces energy consumption and operational costs while raising system reliability as a whole. The choice and placement of appropriate pump technology within the district cooling network have a significant influence on the entire system's longevity and efficacy. The requirement for sustainable and energy-efficient solutions is driving up the importance of pumps in district cooling infrastructure efficiency.

Europe District Cooling Market Segmentation: By Cooling Source:

- Conventional District Cooling

- Renewable Energy-Based District Cooling

The European district cooling market is split into two parts based on the cooling source: conventional district cooling and district cooling fueled by renewable energy. Conventional district cooling relies on traditional energy sources like electricity and fossil fuels to provide centralised cooling services for residential, commercial, and industrial buildings. Conversely, district cooling that is driven by renewable energy sources powers its cooling infrastructure with sustainable and eco-friendly energy from sources like solar, geothermal, or biomass energy. This classification is consistent with the greater movement towards green technologies and shows the industry's dedication to reducing environmental impact and carbon footprints.

Among these, district cooling supplied by renewable energy is the most economical and ecologically friendly. By utilising energy from renewable sources, these technologies significantly reduce reliance on non-renewable energy sources and contribute to reducing greenhouse gas emissions. When district cooling is combined with energy from solar, geothermal, or biomass sources, it not only meets severe environmental regulations but also positions itself as a key player in Europe's energy transition toward a more resilient and sustainable future. When renewable energy sources are used, the market becomes more attractive to environmentally conscious customers and businesses searching for more sustainable and efficient cooling solutions.

Europe District Cooling Market Segmentation: By Service Type:

- Design and Engineering

- Installation Operation and maintenance

The European district cooling market is segmented into multiple groups based on service categories, such as design and engineering, installation, and operation and maintenance. The supply of design and engineering services, which include the meticulous planning and architectural considerations necessary for a cooling infrastructure that is both sustainable and functional, is a crucial component of the district cooling ecosystem. The installation services encompass the physical implementation of the intended system, which involves installing pipes and chillers as well as configuring the district cooling network as a whole. The continuous performance and optimisation of the system depend on operation and maintenance services, which include regular monitoring, troubleshooting, and ensuring that every component operates as efficiently as possible.

The best types of services to ensure the durability and continued performance of district cooling systems are operation and maintenance. Even after the infrastructure is constructed, maintaining system reliability and meeting end-user needs depend on constant operating efficiency. The district cooling system's lifespan is extended and potential issues are averted with routine maintenance. These duties consist of performance optimisations, repairs, and inspections. Efficient system operation and maintenance contribute to long-term cost-effectiveness and enhance overall performance, making it a crucial service area for ensuring the sustainability and viability of district cooling systems.

Europe District Cooling Market Segmentation: By Technology Type

- Cooling

- Absorption Cooling

- Electric Chillers

Among the several types of technologies that distinguish the European district cooling market are electric chillers, absorption cooling, and cooling. Regular refrigeration cycles are used by conventional cooling systems, commonly referred to as compression or mechanical cooling, to produce the desired cooling effect. On the other hand, absorption cooling generates cooling by the utilisation of heat-driven processes and heat sources like natural gas or waste heat. Electric chillers offer a more conventional but efficient approach by producing the necessary chilling effect through the use of electricity. This segmentation reflects the range of technologies utilised in district cooling systems, each having specific advantages and considerations based on project specifications and sustainability goals.

Among these methods, absorption cooling is unquestionably the finest choice available, particularly in terms of promoting sustainability and energy efficiency. By utilising waste heat or renewable heat sources, absorption cooling systems are consistent with the broader trend of employing green technologies in district cooling. Because absorption cooling uses heat-driven processes instead of merely electricity, it is a more energy- and environmentally-friendly cooling solution. This technique is particularly helpful in applications where waste heat is readily accessible or in places where reducing carbon footprints is a top goal. The application of absorption cooling aligns with Europe's transition to sustainable practices and more ecologically friendly cooling solutions.

Europe District Cooling Market Segmentation: By Application

- Government Buildings

- Educational Institution

- Healthcare Facilities

- Data Centers

- Others

To meet the different cooling requirements of different industries, the European district cooling market is divided into segments depending on a variety of applications. Centralised cooling systems can help government buildings, schools, and medical facilities maintain the optimal interior climates for their residents. Due to their large heat generation, data centers discover that district cooling solutions are essential for effectively reducing thermal loads. The diversity of uses for district cooling technology across a range of industries is shown in the "Others" category, which includes retail stores, housing complexes, and industrial buildings. This section shows how adaptable district cooling systems are in many types of settings and how they can be tailored to fit the specific cooling needs of different kinds of applications.

Among these applications, data centers are one of the finest sectors to deploy district cooling technology in. Data centers are notorious for emitting a lot of heat due to their continuous processing activity. District cooling provides a scalable and efficient way to meet the cooling needs of large data centers. By centralising the cooling infrastructure, district cooling systems offer a dependable and energy-efficient means of distributing heat, ensuring optimal operating conditions for essential data center equipment. District cooling in data centers is effective in promoting general energy sustainability and efficiency in addition to fulfilling the specific needs of the industry. This is in line with the growing demand for environmentally friendly solutions in the digital age.

Europe District Cooling Market Segmentation: By End-User Industry:

- Residential

- Commercial

- Industrial

The European district cooling market is segmented based on end-user industries to cater to the varying cooling requirements of the commercial, industrial, and residential domains. In residential settings, district cooling provides a centralised, energy-efficient method of cooling multiple apartment buildings or complexes. Scalability and affordability are two benefits that district cooling systems provide to commercial spaces, including public areas, retail establishments, and office buildings. The industrial sector employs district cooling for large-scale cooling requirements in data centers, manufacturing plants, and other industrial facilities. This section emphasises how district cooling may be used in residential, commercial, and industrial contexts and how flexible it is to meet the needs of different end users.

Among these end-users, the industrial sector is one of the most important and prosperous ones for district cooling. Industrial plants and data centers are typical examples of buildings with high cooling requirements. District cooling systems provide a centralised and efficient way to meet the considerable cooling requirements of big organisations. Maintaining a precise and steady temperature throughout industrial operations contributes to sustainability and energy conservation goals in addition to increasing overall productivity. The industrial sector's use of district cooling highlights the technology's critical role in maintaining critical processes, reducing environmental impact, and advancing overall energy efficiency in industrial applications on a large scale.

Europe District Cooling Market Segmentation: Regional Analysis:

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

The distribution of the district cooling market in Europe is varied, with notable market shares in several major countries. With a substantial 35% market share, Germany is the region's leader in the adoption of district cooling. This is explained by Germany's commitment to energy efficiency and sustainability. With a 20 percent market share, the United Kingdom is not far behind. There, district cooling systems are gaining traction, especially in commercial and metropolitan areas. France exhibits its commitment to centralised cooling solutions for both residential and commercial markets, as evidenced by its substantial 15% market share. Italy and Spain each contribute 7% and 8%, illustrating the range of market penetration in Southern Europe. The remaining 15%, attributed to the remainder of Europe, highlights the existence and potential growth of smaller markets. This distribution highlights the differences in adoption and market dynamics, which represent the evolving district cooling scenario in Europe.

COVID-19 Impact Analysis on the Europe District Cooling Market :

The European district cooling business has faced obstacles as well as opportunities as a result of the COVID-19 outbreak. District cooling system deployment was hampered in the early stages of the epidemic by supply chain disruptions and lockdowns, which also delayed construction and infrastructure projects. New companies faced obstacles due to uncertain economic conditions and a decrease in capital expenditures by governments and businesses. On the other hand, as the area works through the post-pandemic recovery, it is becoming increasingly evident how important district cooling is for improving energy efficiency and promoting sustainable urban growth. The district cooling industry is currently in a better position to support post-COVID recovery initiatives because of the increased emphasis on long-term, ecologically friendly solutions.

In the wake of the pandemic, adaptability and resilience have emerged as major themes. District cooling systems, with their centralized and effective design, are a good fit for these ideas. District cooling may become more popular in both business and residential settings as a result of the pandemic's aftermath the emphasis on better indoor air quality and the demand for energy-efficient solutions. It's possible that upgrading existing buildings with cutting-edge, environmentally friendly cooling systems may increase in the post-COVID age. The district cooling industry is anticipated to grow again as the European economy improves and environmental sustainability continues to be a top concern. By utilizing the knowledge gained from the pandemic, this market will help to create a more resilient and sustainable future.

Latest Trends/ Developments:

European district cooling is exhibiting dynamic trends and advancements that reflect the industry's ongoing shift toward sustainability and innovation. The increasing application of smart technology in district cooling systems, which enables real-time monitoring, adaptive control, and predictive maintenance, is an important advance. This enhances operating efficiency and aligns with the broader goals of the region's smart city initiatives. Furthermore, it's becoming more and more crucial to incorporate renewable energy sources into the district cooling system. Projects that reduce their carbon footprints through the use of biomass, geothermal, and solar energy are examples of this.

Furthermore, the industry is shifting towards decentralised and modular district cooling systems, which provide more flexibility and scalability to suit a variety of metropolitan contexts. The focus on energy efficiency is driving advancements in components like pumps, pipes, and chillers that contribute to the overall system's optimisation. As environmental sustainability becomes increasingly important, district cooling systems are being employed more frequently in new construction projects and retrofitted into existing buildings to meet strict energy efficiency rules. When considered collectively, these patterns demonstrate how the market is embracing technological innovations and sustainable practices with great vigor to meet the evolving needs of climate responsibility and urban growth.

Key Players:

- Siemens

- Fortum

- Helen Oy

- Alfa level

- Engie

- Rasmboll A/S

- Veolia

- Goteborg Energy

- Vattenfall AB

- Wien Engine

The European district cooling industry is defined by several significant businesses that are at the forefront of innovation and environmental standards. Siemens, a pioneer in infrastructure and technology worldwide, advances the development of intelligent and efficient cooling systems by sharing its expertise with the district cooling sector. With a focus on renewable energy, Fortum is a well-known business that actively provides sustainable district cooling services. Helen Oy, a Finnish company, is well-known for its commitment to renewable energy and has had a significant influence on the district cooling industry throughout the Nordic region. Alfa Level, Engie, and Ramboll A/S also play significant roles; each offers unique qualities to the market in the form of technology solutions, full engineering and consulting services, and so on.

Veolia, a global provider of environmental services, is well-known for its all-encompassing approach to district cooling, which strongly emphasises environmental sustainability and circular economy principles. The region's commitment to sustainable urban planning is exemplified by Goteborg Energy and Vattenfall AB, two major players in the development and administration of district cooling systems in Sweden. Lastly, Wien Energie is a well-known company in Austria that develops efficient district cooling systems in keeping with the goals of the country's energy revolution. When united, these noteworthy individuals form a diverse and influential group that drives the growth of the European district cooling industry.