Epoxy Structural Adhesives Market Size (2024 – 2030)

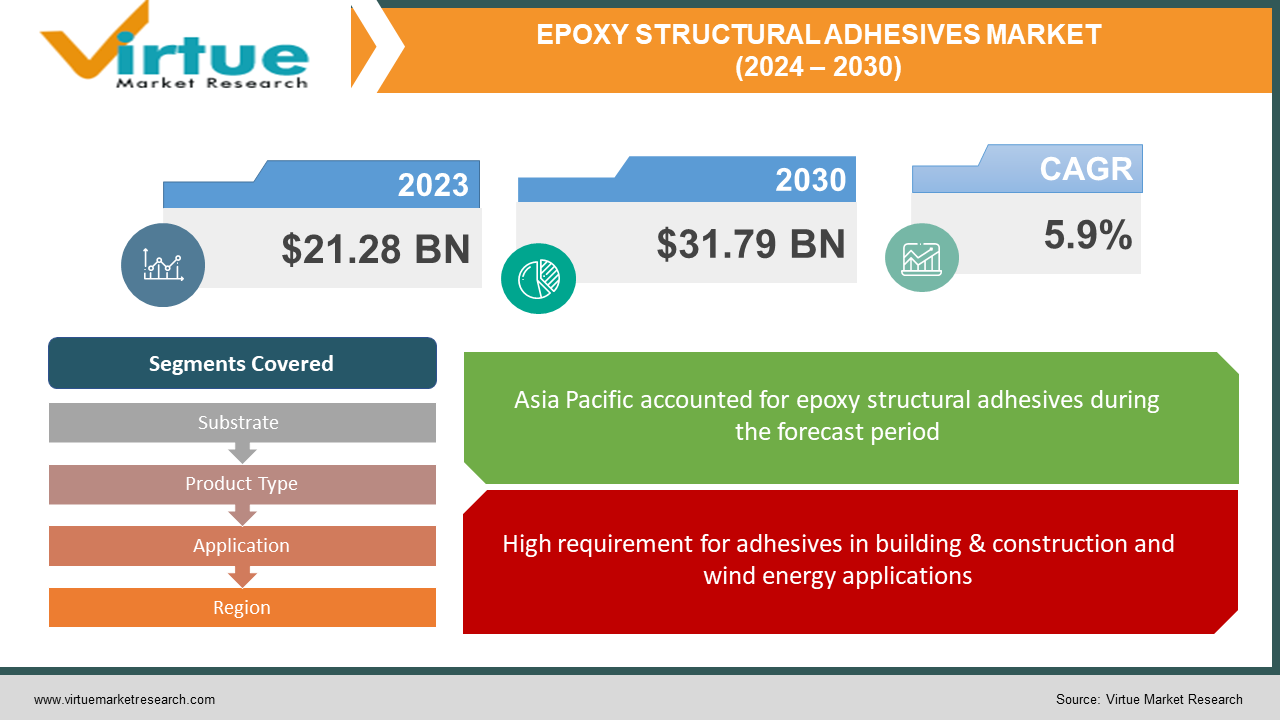

The Structural Adhesives Market was valued at USD 21.28 billion in 2023 and is projected to reach a market size of USD 31.79 billion by the end of 2030. Over the forecast period of 2024-2030, the market is estimated to grow at a CAGR of 5.9%.

Epoxy is usually used as a generic term for a structural adhesive, but epoxy adhesives are a very specific class of structural adhesives. These chemistries are durable in necessary conditions – not only against outdoor weathering but also many solvents and other conditions. Epoxy is the most widely applied structural adhesive because it can adhere to several types of materials, has high strength, less emission of Volatile Organic Compound (VOC) during the curing process, and can sustain heavy loads. They are obtainable in both one and two-component form. Epoxy structural adhesives are utilized in aerospace, buses & trucks, and railways for bonding many substrates like ceramics, metal, wood, concrete, composites, and rubber. Epoxy structural adhesives offer high strength along with mechanical, thermal, and electrical properties.

Key Market Insights:

The power and energy segment is estimated to be the fastest-growing segment in the epoxy adhesives market over the future years. Growth in wind power installations escalates the usage of epoxy adhesives; for example, wind turbine blade assemblies are made of many bonded and fastened elements.

Epoxy Structural Adhesives Market Drivers:

High requirement for adhesives in building & construction and wind energy applications

The emerging middle-class population, altering lifestyles and improving the standard of living in China, India, and Mexico is leading to growing demand for high-quality products.

New uses such as carpet adhesives, tiling adhesives, wallpapers, and exterior insulation systems in the construction industry are propelling the demand for structural adhesives in the construction sector. The key applications of construction adhesives are floor systems, interior wallboards, and panels. Application of these adhesives provides wall exteriors free from marks caused by nail or screw heads. Construction adhesives are used to contain curtain wall panels and insulating glass units in place. Enhancing demand for permanent, non-slum houses across India and other developing nations such as Brazil, China, Indonesia, and Vietnam is mainly driven by the growth in population, urbanization, and rising income in these countries.

Epoxy Structural Adhesives Market Restraints and Challenges:

Different characteristic restrictions of various adhesives

All structural adhesives have differentiating characteristics and mechanical properties. Epoxies are applied in rigid bonding with very high shear strength; polyurethane is utilized in slightly flexible bonding with high strength and acrylic is used in rigid to slightly flexible bonding with high effect and fatigue resistance. Each variety of adhesive has some limitations in its properties. So, the choice of adhesives depends on the type of application. The type of adhesives to be used relies on the type of substrate to be bonded, the strength required, environmental conditions, and others. For example, in the aerospace industry, materials that are to be used in fabricating aircraft have to go through stringent and lengthy certification procedures, and they need a higher grade of adhesives that must be heat protectant, tough, moisture-resistant, sustainable in harsh environmental conditions, and soon. Hence, the bottlenecks associated with each adhesive restrict the use of a particular adhesive in different applications.

Developed countries such as the US, Germany, the UK, Japan, and other Western European nations have a well-established infrastructure for the public, commercial, and transport sectors. The developed infrastructure in these countries represents low prospects for new construction activities as civil structures are constructed to last a lifetime. Manufacturers need to come up with creative products to capture newer markets such as the medical, agricultural, healthcare, and food packaging sectors. Therefore, sustaining and widening business is a major challenge for manufacturers in the matured markets.

Epoxy Structural Adhesives Market Opportunities:

Growing demand for non-hazardous, green, and sustainable structural adhesives

Due to the rising demand for eco-friendly or green products in various applications, the need for sustainable adhesives or those with low VOC is increasing. Strict regulations by the USEPA (United States Environmental Protection Association), Europe’s REACH (Registration, Evaluation, Authorization, and Restrictions of Chemicals), Leadership in Energy and Environmental Design (LEED), and other regional regulatory authorities have pushed manufacturers to make eco-friendly adhesives with low VOC levels. In light of these regulatory policies, there is an upcoming trend in the worldwide structural adhesives market for environment-friendly or green buildings, which offers an opportunity for the development of green and sustainable adhesive solutions. Such eco-friendly adhesive solutions are made from renewable, recycled, remanufactured, or biodegradable products health and environment-friendly.

EPOXY STRUCTURAL ADHESIVES MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

5.9% |

|

Segments Covered

|

By Substrate, Product Type, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Henkel AG & Co. KGaA, Dow, 3M, HB Fuller Company, Franklin International, Inc., Avery Dennison Corporation, Ashland Global Specialty Chemicals Inc., Lord Corporation, Arkema S.A., Scott Bader Co.

|

Epoxy Structural Adhesives Market Segmentation: By Substrate

-

Metal

-

Wood

-

Composite

-

Plastic

-

Others

The metal substrate segment was the biggest revenue generator and is expected to grow at a CAGR of 7.1% during the estimated period. Applications that need the joining of two metal parts without the use of traditional joining techniques, such as soldering and welding, can be achieved with the usage of structural adhesives. Additionally, integrating two metals is possible if the adhesive provides resistance to heat and chemicals. This factor is boosting the growth of this segment in the global market.

Epoxy Structural Adhesives Market Segmentation: By Product Type

-

Solvent-based

-

Water-based

-

Others

By product type, the water-based segment dominated the global market in recent years and is expected to grow at a CAGR of 7.2% during the forecast period. This is dedicated to the fact that attributes, such as adhesion quality, wet tackiness, enhanced adhesion with painted metal surfaces, minimal time for drying, and low flammability, are the key elements that make them congenial for a variety of end-use industries.

Epoxy Structural Adhesives Market Segmentation: By Application

-

Automotive

-

Building & Construction

-

Aerospace

-

Electrical & Electronics

-

Energy

-

Others

By application, the automotive segment dominated the global structural adhesives market in recent years and is expected to grow at a CAGR of 7.0% during the forecast period. Structural adhesives are used in automotive applications, due to flexibility and ability to provide enhanced performance in complex engineering designs. Additionally, owing to its capacity to accommodate thermal expansion and electrical conductivity, structural adhesives are proven to offer needed performance in automotive applications.

Epoxy Structural Adhesives Market Segmentation: By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

Asia Pacific dominated the structural adhesives industry with the biggest revenue share of 34.9% in recent years. The high demand in the Asia Pacific region is influenced by the growing construction industry in countries like China, India, and Japan. According to the International Trade Administration, China has the top urbanization rate in the world, and as the country grows as a greener economy, there will be more opportunities for low-carbon construction such as green buildings. This is expected to boost the development of the construction sector in the country, thereby leading to the growth of the structural adhesives industry over the estimated years.

Europe is likely to offer lucrative development opportunities for structural adhesives industry players on account of accelerating construction activities around the region, due to the rapidly growing industrial sector coupled with a high urbanization percentage. Moreover, the growing transportation sector is also estimated to augment the demand for structural adhesives in Europe. Elements such as congested roads and increasing volume of traffic are likely to push the growth of the transportation industry in the region, thereby positively affecting the market shortly.

COVID-19 Impact Analysis on the Epoxy Structural Adhesives Market:

The structural adhesives market has been detrimentally impacted in the wake of the COVID-19 pandemic, due to its dependence on automotive, aerospace, energy, and other sectors. As per the report published by Wipro, the automotive industry witnessed a 30% decline in sales in March 2020 as compared to March 2019, owing to lockdowns and shutdowns of auto plants. Several automotive companies have either shut down or narrowed their operations due to the risk of infections among the workforce where structural adhesives are utilized as a prime bonding material for hoods, grills, interior panels, and other vehicle fragments. This has temporarily affected the demand for structural adhesives amid the COVID-19 period. Stoop down the income of customers and international travel restrictions led to a contraction of the demand for structural adhesives in the Aerospace sector. COVID-19 has put a temporary pause on various aircraft manufacturing projects, which, in turn, has reduced the demand for structural adhesives among the aerospace & aviation sectors. Additionally, the structural adhesives market has experienced a downfall in demand among the construction sectors, due to a temporary halt on various building & construction projects in the COVID-19 period.

Latest Trends:

Government Programs supporting Epoxy Structural Adhesives

The demand for structural adhesives has increased in India over the recent years. The market is estimated to rise at a 6.4% CAGR. Construction in India is set to become the third-largest market in the world by the next decade. Growing disposable incomes and government smart city initiatives will encourage the market. As consumer electronics become increasingly complex, structural adhesives play a crucially important role as a way to assemble electronic components, bond conductive films, and link conductive alloys.

Adoption of Technology

Structured adhesive technology will be a primary focus for the world in the future years. The market is estimated to expand at a CAGR of 3.7% by 2030. Companies operating in the structural adhesives industry will likely find lucrative development opportunities in the United Kingdom. The rapidly building industrial sector and the high rate of urbanization are contributing to the escalation of construction activity around the region. As technology and advancements become more prevalent, the market is estimated to grow. As the transportation industry spikes, structural adhesives will also become more famous. In the aerospace industry, deployments in lightweight and efficient vehicles also drive structural adhesive consumption in the country.

Key Players:

-

Henkel AG & Co. KGaA

-

Dow

-

3M

-

HB Fuller Company

-

Franklin International, Inc.

-

Avery Dennison Corporation

-

Ashland Global Specialty Chemicals Inc.

-

Lord Corporation

-

Arkema S.A.

-

Scott Bader Co.

Recent Developments

-

October 2022- Scott Bader (Wellingborough, United Kingdom) collaborated with Elixir (Bengaluru, India) to distribute Cresta bond structural adhesives to the entire India. The announcement is consistent with the company's promise made in April 2022 to encourage the Indian composites market.

-

June 2023- Park Aerospace Corp. launched its new structural film adhesive product, Aeroadhere FAE-350-1, for bonding primary and secondary structures.