GLOBAL CRITICAL COMMUNICATION MARKET (2024 - 2030)

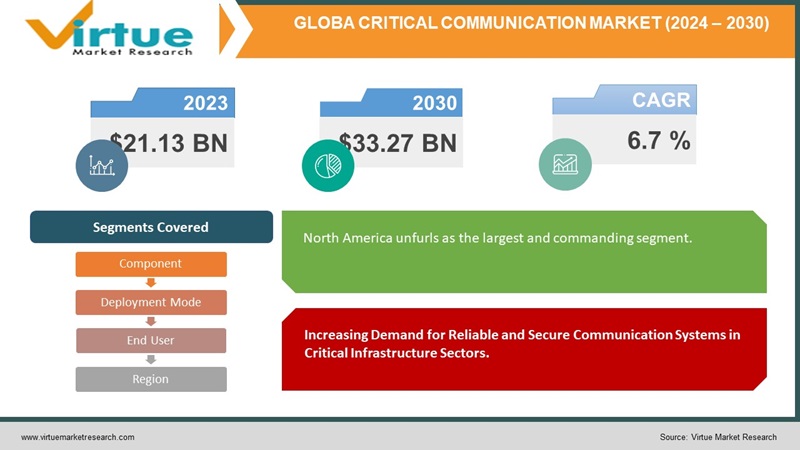

The Global Critical Communication Market was valued at USD 21.13 billion and is projected to reach a market size of USD 33.27 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 6.7%.

The Critical communication Market involves utilizing communication systems to support essential service providers such as public safety, utilities, and transportation. The market is primarily fueled by the rising requirement for secure communication in critical infrastructure sectors, driven by factors like the necessity to replace aging infrastructure, the adoption of new technologies like 5G, the surge in demand for cloud-based solutions, and an increasing focus on cybersecurity. However, the critical communication market encounters challenges, including the high costs associated with deployment and maintenance, the complexity of integrating diverse technologies, and the imperative for interoperability among different systems. Additionally, the market faces a growing threat from cybersecurity attacks, further emphasizing the need for robust security measures in this sector.

Key Market Insights:

The critical communication market is witnessing substantial growth driven by several key factors. Technological advancements, particularly the integration of 5G, artificial intelligence (AI), and machine learning (ML), are reshaping communication solutions, and enhancing reliability and security. The increasing adoption of cloud-based solutions for their scalability and flexibility further propels market expansion. This surge in demand is underlined by a commitment to innovation, exemplified by specialized offerings like Sovereign Systems' BWM Mk. 3 radio designed for military and law enforcement applications.

In November 2023, Sovereign Systems introduced its latest innovation to the market with the launch of the BWM Mk. 3 (Body Worn Mesh) radio. Tailored for military and law enforcement applications, this cutting-edge radio stands out with advanced features. Among its capabilities are high-bandwidth data connectivity, ensuring seamless communication, and the provision of secure voice and video communications. This announcement reflects Sovereign Systems' commitment to providing state-of-the-art solutions to meet the sophisticated communication needs of military and law enforcement personnel.

In the global critical communication market, a hierarchy of influential players shapes the industry's dynamics. Leading the pack is Motorola Solutions, with the largest market share at 37.0%, reflecting its pivotal role in delivering reliable and secure communication solutions. Following suit, Nokia secured a substantial 22.0%, showcasing its telecommunications expertise. Ericsson contributes significantly with a 19.0% market share, emphasizing its crucial role in shaping networking solutions. Huawei holds a noteworthy 14.0%, showcasing its technological prowess, while Hytera maintains a solid presence with an 8.0% share. These market shares encapsulate the competitive landscape, where each player plays a crucial role in meeting the evolving demands of critical communication across diverse sectors.

Global Critical Communication Market Drivers:

Increasing Demand for Reliable and Secure Communication Systems in Critical Infrastructure Sectors.

Critical infrastructure sectors, encompassing public safety, utilities, transportation, and healthcare, heavily depend on the efficacy of reliable and secure communication systems. The heightened demand for these systems is propelled by several factors. The escalating complexity of critical infrastructure networks necessitates advanced communication solutions to ensure seamless operations. The growing threat of cyberattacks underscores the importance of robust and secure communication frameworks to safeguard sensitive information. Additionally, the increasing need for real-time coordination and information sharing within and across these sectors further amplifies the demand for communication systems that guarantee reliability and security.

Replace aging infrastructure in critical communication systems due to obsolescence.

Many existing critical communication networks are grappling with the challenges posed by aging infrastructure. This imperative to replace outdated systems stems from various factors. The obsolescence of older technologies in these networks necessitates an upgrade to modern, more efficient solutions. The increasing demand for higher bandwidth, driven by the proliferation of data-intensive applications, is a key factor in the need for infrastructure renewal. Furthermore, the imperative for more secure networks, capable of addressing contemporary cybersecurity threats, adds urgency to the task of replacing aging infrastructure in critical communication systems.

Adoption of New Technologies such as 5G in Critical Communication Systems.

The adoption of next-generation wireless technology, notably 5G, stands out as a pivotal driver in the evolution of the critical communication landscape. 5G offers a spectrum of advantages over older technologies, including faster data speeds, lower latency, and increased network capacity. These inherent benefits position 5G as an ideal choice for critical communication applications. As critical infrastructure sectors increasingly recognize the need for advanced communication capabilities, the adoption of 5G becomes a strategic move to meet the evolving requirements of these sectors, ensuring more efficient and responsive communication networks.

Global Critical Communication Market Restraints and Challenges:

High Cost of Deployment and Maintenance in Critical Communication Systems:

The deployment and maintenance of critical communication systems come with a significant financial burden. These systems, vital for ensuring public safety and operational continuity, often involve substantial upfront costs. The ongoing expenses related to maintenance further contribute to the financial challenge. This high cost of entry can pose a barrier for new vendors entering the market and present difficulties for existing vendors aiming to expand their footprint.

Crucial Imperative: Addressing the Vital Need for Seamless Interoperability between Diverse Systems in Critical Communication.

In the intricate domain of critical communication, ensuring effective collaboration mandates a strategic emphasis on interoperability among diverse systems. This imperative underscores the critical requirement for different communication technologies to seamlessly integrate, fostering a unified and responsive ecosystem. However, the achievement of interoperability presents a multifaceted challenge, given the absence of standardized protocols. Consequently, innovative solutions must be harnessed to bridge this technological divide, enabling a smooth and cohesive exchange of information across the diverse landscape of critical communication systems.

Escalating Concerns: The Growing Threat of Cybersecurity Attacks in Critical Communication Systems.

As technology advances, the specter of cybersecurity attacks looms larger over critical communication systems, adding an extra layer of complexity to their operational landscape. The increasing sophistication of cyber threats poses a substantial risk, capable of disrupting or even disabling these pivotal systems. Safeguarding against these evolving threats demands continual vigilance and robust cybersecurity measures to fortify the resilience of critical communication networks, ensuring their ability to withstand and repel potential cyber adversaries in the ever-evolving digital terrain.

Global Critical Communication Market Opportunities:

Evolutionary Momentum: Unleashing Growth through the Development of Cutting-edge Critical Communication Solutions.

The dynamic landscape of the critical communication market hinges on the continuous development of novel and innovative solutions. This evolution is poised to serve as a pivotal driver, propelling market growth. The imperative lies in crafting solutions that are not only ground-breaking but also reliable, secure, and meticulously tailored to meet the distinct needs of critical infrastructure sectors. As technology advances, the strategic deployment of these solutions becomes instrumental in elevating the efficiency and resilience of critical communication networks.

5G Revolution: Capitalizing on Opportunities with the Adoption of Next-Gen Technology.

The impending adoption of 5G technology stands as a beacon of opportunity for the critical communication market. This transformative shift is anticipated to unlock significant advantages over older technologies. The promise of faster data speeds, lower latency, and increased capacity positions 5G as the quintessential technology for critical communication applications. By embracing 5G, the market can harness its potential to enhance communication capabilities, fortify responsiveness, and foster innovation within critical infrastructure sectors.

Cloud-Based Renaissance: Embracing Scalability, Flexibility, and Cost-Efficiency in Critical Communication Solutions.

A paradigm shift is underway in the critical communication market, marked by the burgeoning popularity of cloud-based solutions. This trend signifies a departure from traditional on-premises models, heralding a new era of scalability, flexibility, and cost reduction. Cloud-based solutions offer a dynamic framework, allowing critical communication systems to scale seamlessly, adapt to evolving needs, and optimize operational costs. This transformative wave is set to reshape the market, providing a strategic edge to those who navigate the cloud landscape adeptly.

Safeguarding the Future: Meeting the Rising Demand for Cybersecurity Solutions.

The escalating threat landscape of cyberattacks casts a spotlight on the indispensable role of cybersecurity solutions in the critical communication market. The rising demand for robust cybersecurity measures presents a distinct growth avenue. Critical communication providers poised to meet this demand are well-positioned to thrive by crafting and delivering cutting-edge cybersecurity solutions. These solutions stand as formidable guardians, shielding critical communication networks from potential cyber threats and ensuring the integrity and security of essential communication infrastructures.

GLOBAL CRITICAL COMMUNICATION MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6.7%

|

|

Segments Covered

|

By Component, Deployment Mode, End User and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Motorola Solutions, Inc., Ericsson, Nokia Corporation, L3Harris Technologies (formerly Harris Corporation), Hytera Communications Corporation Ltd., Airbus SE, Hexagon AB, JVCKENWOOD Corporation

Cisco Systems, Inc., ZTE Corporation

|

Global Critical Communication Market Segmentation:

Market Segmentation: By Component:

- Infrastructure

- Devices

- Services

Within the intricate fabric of the critical communication market, an exploration of its components unravels distinct and noteworthy trends. At the forefront of this analysis stands the Infrastructure segment, towering as the largest and foundational contributor. Serving as the robust backbone of critical communication systems, Infrastructure components lay the groundwork, encapsulating technologies, hardware, and network elements that collectively form the indispensable core framework.

Simultaneously, mirroring this foundation, the Services segment emerges as the dynamic and fastest-growing sector within the critical communication landscape. Services play a multifaceted role, assuming the mantle of a catalyst for growth. This sector extends a spectrum of solutions designed to elevate and optimize the functionality of critical communication systems. The remarkable growth trajectory of Services underscores an increasing acknowledgment of the value added by this segment. Embracing maintenance, support, consulting, and other critical offerings and services solidifies their significance as a linchpin in propelling the evolution and efficiency of critical communication networks.

Market Segmentation: By Deployment Type:

- Public safety networks

- Private LTE networks

- Hybrid networks

In the multifaceted arena of the critical communication market, deployment types delineate distinctive trajectories, each contributing to the intricate landscape. Foremost among these is the towering segment of Public Safety Networks, reigning as the largest and foundational contributor. These networks stand as the linchpin for crucial services, providing a dedicated and secure channel for public safety organizations, law enforcement, and emergency responders. The resilience and reliability of Public Safety Networks position them as indispensable elements, ensuring seamless communication in mission-critical scenarios.

In tandem with the stalwart presence of Public Safety Networks, the fastest-growing segment within the critical communication market unfolds in the dynamic realm of Hybrid Networks. This deployment type epitomizes adaptability, seamlessly integrating the strengths of both public and private networks. The surge in popularity of Hybrid Networks reflects a strategic response to the evolving needs of critical communication. This innovative approach offers a flexible and resilient strategy, harmoniously combining the strengths of dedicated public safety networks with the versatile and customizable nature of private solutions. In doing so, Hybrid Networks emerge as a strategic bridge, addressing the diverse requirements of the critical communication landscape while ensuring adaptability and efficiency in the face of evolving challenges.

Market Segmentation: By End User:

- Government

- Utilities

- Transportation

- Healthcare

In the intricate tapestry of the critical communication market, end-user categories emerge as vivid threads, each illuminating distinctive spheres of influence. Towering above them all is the Government, standing as the largest and central segment. Government entities wield critical communication systems as formidable tools to uphold public safety, seamlessly coordinate emergency responses, and ensure the uninterrupted operation of essential services. The expansive reach of government deployment underscores the pivotal role played by critical communication in maintaining societal order and safety.

Simultaneously, a noteworthy narrative unfolds within the domain of healthcare, representing the fastest-growing segment in this dynamic landscape. The burgeoning importance of secure and efficient communication within healthcare settings underscores an increasing recognition of technology's pivotal role in patient care, emergency response, and overall operational efficiency. The rapid adoption of critical communication solutions within the healthcare sector serves as a testament to its commitment to delivering timely and effective services, placing a paramount emphasis on patient well-being. In embracing technological advancements, the healthcare domain showcases a proactive stance toward leveraging critical communication for enhanced operational efficacy and, ultimately, the improvement of patient outcomes.

Market Segmentation: By Region:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

In the geographical tapestry of the critical communication market, North America unfurls as the largest and commanding segment. The region's pre-eminence is a testament to its advanced technological infrastructure and the strategic integration of critical communication systems. North America's leadership is etched by robust implementations spanning various sectors, solidifying the region's pivotal role in shaping the trajectory of critical communication. The nuanced interplay of technology, infrastructure, and strategic initiatives cements North America's standing as a vanguard in the evolution of critical communication solutions.

Contrastingly, the fastest-growing segment comes to life in the vibrant landscape of Asia-Pacific. This dynamic region experiences accelerated growth propelled by a convergence of factors, including rapid technological adoption, burgeoning urbanization, and an intensified focus on enhancing public safety. As Asia-Pacific embraces the transformative power of critical communication, it surges into a position of accelerated growth. This ascent is marked by a burgeoning market presence and the cultivation of innovative solutions tailored to the unique operational landscapes that characterize the diverse and rapidly evolving Asia-Pacific region. The interplay of these factors paints a vivid picture of a region not only catching up but propelling itself to the forefront of the critical communication market.

COVID-19 Impact Analysis on the Global Critical Communication Market:

In the short term, the COVID-19 pandemic posed unprecedented challenges to the global critical communication market. The crisis necessitated an immediate surge in demand for critical communication solutions, as organizations grappled with the imperative to stay connected and coordinated amid the turmoil. Public safety entities found themselves relying heavily on critical communication tools to respond to emergencies, while utilities leaned on these solutions to maintain operations and facilitate communication with customers. The urgency of the situation underscored the pivotal role of critical communication in crisis response, showcasing its indispensability during unforeseen challenges.

Looking beyond the immediate impact, the COVID-19 pandemic is shaping a transformative trajectory for the global critical communication market in the long term. Organizations, recognizing the need for heightened resilience and preparedness, are expected to accelerate the adoption of critical communication solutions. The enduring effects of the pandemic are driving innovation in the sector, fostering the development of new solutions infused with artificial intelligence and machine learning capabilities. This forward-looking approach aims to enhance not only immediate crisis response but also the overall adaptability and effectiveness of critical communication systems in the face of future challenges. The pandemic, while presenting short-term hurdles, is catalyzing a long-term evolution in the critical communication landscape, paving the way for continued growth and innovation in the years ahead.

Latest Trends/Developments:

The critical communication landscape is witnessing a paradigm shift with the increasing adoption of 5G, a next-generation wireless technology that brings forth a multitude of advantages over its predecessors. Faster data speeds, lower latency, and increased capacity position 5G as an ideal fit for critical communication applications. The technology is poised to provide a more reliable and secure platform, particularly benefiting emergency services, public safety, and critical infrastructure sectors.

The emergence of artificial intelligence (AI) and machine learning (ML) is catalyzing innovation in critical communication solutions. AI is being harnessed to develop predictive tools that can anticipate and prevent network outages, while ML is enabling the creation of solutions adept at detecting and responding to cybersecurity threats. The rising adoption of AI and ML stands as a key catalyst in propelling the sector forward, enhancing its capabilities in anticipation of evolving challenges.

In tandem with technological advancements, there is a growing demand for cloud-based critical communication solutions, which offer scalability, flexibility, and cost reductions compared to traditional on-premises alternatives. This burgeoning trend is transforming the way critical communication systems operate, providing an agile and adaptable framework. The ascendancy of cloud-based solutions reflects a strategic shift towards optimizing operational efficiency and harnessing the full potential of advanced technologies in the critical communication sector.

Key Players:

- Motorola Solutions, Inc.

- Ericsson

- Nokia Corporation

- L3Harris Technologies (formerly Harris Corporation)

- Hytera Communications Corporation Ltd.

- Airbus SE

- Hexagon AB

- JVCKENWOOD Corporation

- Cisco Systems, Inc.

- ZTE Corporation

Key players wield substantial influence in the global critical communication market, with industry giants such as Nokia, Motorola Solutions, Huawei, ZTE, and Hytera at the forefront. These companies offer an extensive array of critical communication solutions, encompassing devices, networks, and services. Their strategic positioning is fortified by substantial investments in research and development, underscoring a commitment to innovation and staying at the vanguard of this swiftly evolving market.