Computer Vision Market Size (2024 – 2030)

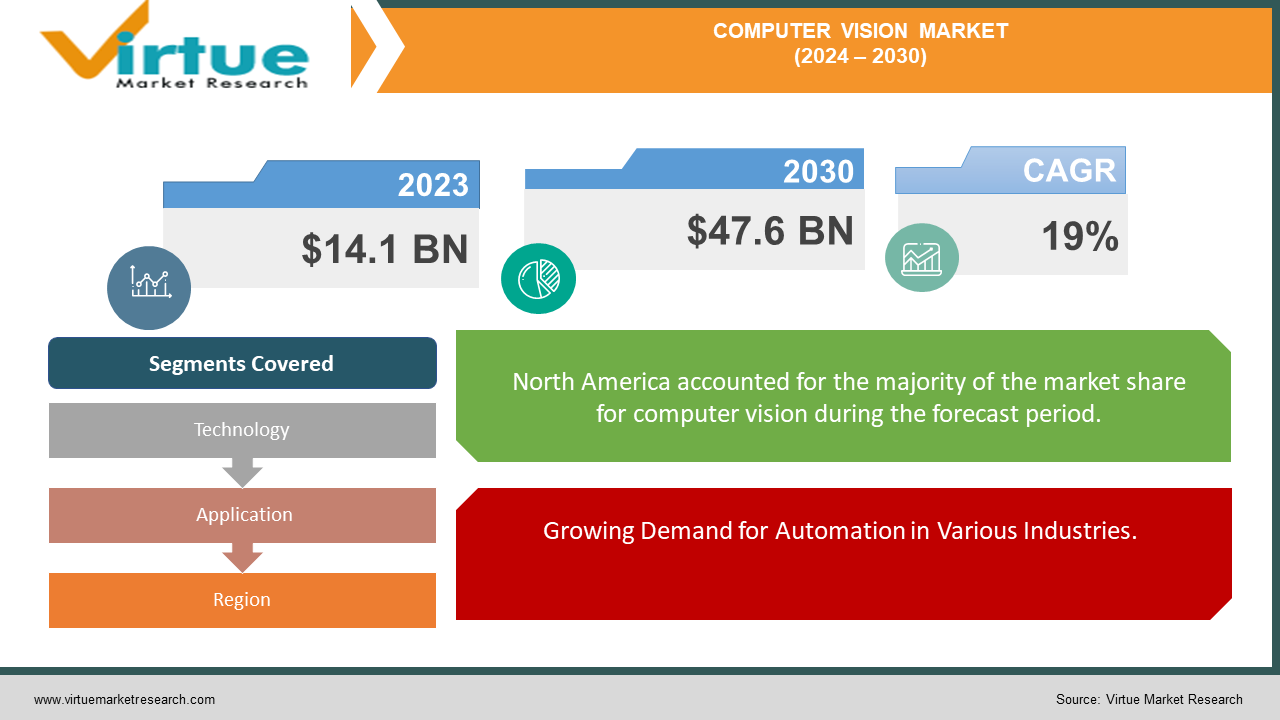

The Global Computer Vision Market was valued at USD 14.1 billion in 2023 and is projected to reach a market size of USD 47.6 billion by the end of 2030. The market is anticipated to expand at a compound annual growth rate (CAGR) of 19% between 2024 and 2030.

The Global Computer Vision Market is experiencing rapid growth, driven by advancements in artificial intelligence (AI) and machine learning technologies. This technology empowers machines to interpret and process visual data, enabling applications across a wide range of industries, including healthcare, automotive, retail, and manufacturing. Key drivers include the increasing demand for automation, enhanced security systems, and improved quality control mechanisms. In sectors such as autonomous vehicles, computer vision plays a pivotal role in object detection and decision-making processes. The surge in smartphone penetration and the integration of AI-driven cameras are also fueling market expansion. Additionally, innovations in hardware, such as high-performance image sensors and processors, are enhancing the capabilities of computer vision systems. However, challenges like high implementation costs and the complexity of algorithms could pose obstacles to widespread adoption. As businesses and governments worldwide invest in AI and automation, the computer vision market is poised to witness significant advancements, revolutionizing how machines perceive and interact with the world.

Key Market Insights:

AI-powered computer vision adoption is growing at a CAGR of over 7%.

Automotive industry accounts for approximately 20% of the market's total revenue.

Healthcare applications are projected to grow by more than 9% annually.

Asia-Pacific region is expected to dominate with over 35% market share by 2026.

Image recognition technology constitutes about 40% of the market's application scope.

The use of computer vision in retail is expected to rise by 15% in the next 5 years.

Facial recognition systems are anticipated to grow by nearly 12% annually.

By 2027, over 50% of the market's growth will come from the manufacturing sector.

Global Computer Vision Market Drivers:

Growing Demand for Automation in Various Industries.

The rising demand for automation across multiple industries is a key driver of the Global Computer Vision Market. Industries such as manufacturing, automotive, and retail are increasingly adopting computer vision technology to enhance efficiency, precision, and safety in their operations. In manufacturing, computer vision systems are used for quality control, defect detection, and automated assembly lines, significantly reducing human error and improving productivity. In the automotive sector, computer vision is integral to the development of autonomous vehicles, enabling real-time analysis of the environment and decision-making. Retailers are leveraging this technology for customer behavior analysis, inventory management, and automated checkouts, improving the shopping experience. The global push towards Industry 4.0 and the increasing reliance on AI-driven systems to streamline operations are further accelerating the adoption of computer vision solutions. This trend is likely to continue as businesses across sectors seek to reduce operational costs and enhance performance, fueling the growth of the computer vision market.

Advancements in AI and Machine Learning Technologies

Advancements in artificial intelligence (AI) and machine learning (ML) technologies are significantly propelling the Global Computer Vision Market. AI-powered computer vision systems have enhanced the ability of machines to process and interpret complex visual data, leading to breakthroughs in various sectors. In healthcare, AI-driven computer vision is used for diagnostic imaging, assisting in detecting diseases such as cancer, and providing more accurate and timely diagnoses. In the automotive industry, AI-enhanced computer vision improves the functionality of autonomous vehicles, enabling better object detection and navigation in complex environments. Moreover, in the security and surveillance sectors, AI-powered computer vision systems are enabling real-time monitoring and threat detection, leading to improved safety. The integration of machine learning algorithms allows these systems to learn and adapt over time, improving their accuracy and efficiency. As AI and ML technologies continue to evolve, the capabilities of computer vision systems are expanding, driving further growth and innovation in the market.

Global Computer Vision Market Restraints and Challenges:

One of the primary restraints and challenges facing the Global Computer Vision Market is the high implementation cost and complexity of the technology. Developing and deploying computer vision systems requires substantial investment in advanced hardware components such as high-performance cameras, sensors, and processors, which can be prohibitively expensive for small and medium-sized enterprises (SMEs). Additionally, the complexity of creating and training algorithms to accurately interpret visual data presents a significant technical challenge. These systems must be finely tuned to ensure reliable performance, especially in critical applications like healthcare and autonomous vehicles, where errors could have serious consequences. Furthermore, computer vision technologies often require vast amounts of labeled data for effective machine learning model training, which can be difficult to obtain and manage. Privacy and security concerns also pose challenges, particularly in applications like facial recognition and surveillance, where data misuse or breaches could lead to ethical and legal issues. As a result, many organizations are hesitant to adopt these systems without clear solutions to these challenges. The need for robust regulatory frameworks and standardized practices to ensure safety, security, and affordability remains an ongoing challenge for the global computer vision market’s growth.

Global Computer Vision Market Opportunities:

The Global Computer Vision Market presents significant opportunities, particularly through the growing integration of artificial intelligence (AI) and the Internet of Things (IoT). As industries increasingly adopt smart technologies, the demand for advanced computer vision solutions is set to rise. In sectors such as healthcare, AI-driven computer vision is opening doors for innovations like automated diagnostics, robotic surgeries, and precision medicine. Similarly, in retail, the use of computer vision in cashier-less stores, customer behavior analytics, and personalized shopping experiences is gaining traction. Another major opportunity lies in the automotive industry, where the development of autonomous vehicles and advanced driver assistance systems (ADAS) is heavily reliant on computer vision technologies for tasks like object detection, lane departure warnings, and collision avoidance. Moreover, the expansion of IoT devices, including smart cameras and sensors, is fueling the adoption of computer vision in security and surveillance, smart homes, and industrial automation. As cloud-based and edge computing technologies mature, they further enhance the scalability and accessibility of computer vision solutions, making it easier for businesses to implement these technologies. With continuous innovation in AI, hardware, and data processing, the global computer vision market is poised for exponential growth, offering vast opportunities across multiple industries.

COMPUTER VISION MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

19% |

|

Segments Covered

|

By Technology, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Intel Corporation, NVIDIA Corporation, Cognex Corporation, Basler AG, Teledyne Technologies Inc., Sony Corporation, Microsoft Corporation, Google LLC, Qualcomm Technologies Inc., Omron Corporation

|

Global Computer Vision Market Segmentation: By Technology

In 2023, based on market segmentation by Technology, Hardware had the highest share of the Global Computer Vision Market. Technological advancements in the Global Computer Vision Market are significantly enhancing the capabilities and accessibility of visual data processing. One notable development is the improvement in camera technology, which now features higher resolutions and better low-light capabilities, enabling the capture of more detailed and accurate visual data under various conditions. This advancement has made it easier to implement computer vision solutions in applications that require high precision. Additionally, there is an increasing demand for specialized hardware components driven by the growing adoption of computer vision across diverse industries such as automotive, healthcare, and manufacturing. These industries rely on advanced hardware to support complex algorithms and real-time data analysis. The market is also experiencing a reduction in hardware costs, particularly for graphics processing units (GPUs), which are crucial for handling the computational demands of computer vision tasks. This cost reduction is making computer vision solutions more affordable and accessible to businesses of all sizes, from startups to large enterprises. Together, these advancements are driving innovation in computer vision technology, expanding its applications, and facilitating broader adoption across various sectors.

Global Computer Vision Market Segmentation: By Application

-

Automotive

-

Healthcare

-

Manufacturing

-

Retail

In 2023, based on market segmentation by Application, Automotive had the highest share of the Global Computer Vision Market. The automotive sector’s prominence in the Global Computer Vision Market in 2023 is driven by several crucial factors. Firstly, the development of autonomous vehicles heavily relies on computer vision technologies for essential tasks such as object detection, lane keeping, and traffic sign recognition, enabling vehicles to navigate safely and autonomously. Advanced Driver Assistance Systems (ADAS) are also a significant contributor, with features like adaptive cruise control, lane departure warning, and automatic emergency braking increasingly incorporating computer vision to enhance vehicle safety and driver comfort. Stringent safety regulations imposed by governments worldwide further drive the adoption of computer vision technologies, as manufacturers seek to comply with these standards and improve vehicle safety. Additionally, growing consumer demand for advanced automotive features has fueled market expansion, as buyers increasingly seek vehicles equipped with cutting-edge technologies powered by computer vision. These combined factors have cemented the automotive sector as a leading segment in the computer vision market, highlighting its crucial role in advancing vehicle technology and meeting evolving safety and consumer expectations.

Global Computer Vision Market Segmentation: By Region

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

In 2023, based on market segmentation by Region, North America had the highest share of the Global Computer Vision Market. North America has been a key driver of growth in the Global Computer Vision Market due to several pivotal factors. Early adoption of computer vision technologies by companies in the technology and automotive sectors established the region as a leader in this space. North American firms were among the first to integrate computer vision into their products and services, driving significant market growth. Additionally, the region boasts a strong research and development ecosystem, with numerous research institutions, universities, and technology companies actively advancing computer vision innovations. This robust R&D environment has been instrumental in pushing the boundaries of technology and fostering new applications. The favorable regulatory environment in the United States and Canada also plays a crucial role, as these countries offer supportive frameworks for the development and deployment of computer vision technologies. Furthermore, the presence of major market players, such as Google, Intel, and NVIDIA, headquartered in North America, contributes to the region’s leadership. These companies not only drive technological advancements but also set industry standards, further solidifying North America’s position as a dominant force in the computer vision market.

COVID-19 Impact Analysis on the Global Computer Vision Market.

The COVID-19 pandemic had a mixed impact on the Global Computer Vision Market, with disruptions and opportunities emerging across various sectors. Initially, the pandemic caused supply chain interruptions and project delays, particularly in industries like automotive and manufacturing, which experienced slowdowns due to lockdowns and restrictions. However, the crisis also accelerated the adoption of computer vision technologies in several key areas. In healthcare, computer vision was leveraged for AI-driven diagnostics, such as automated detection of COVID-19 symptoms in medical imaging, as well as in patient monitoring and telemedicine. The retail sector saw increased use of computer vision for contactless shopping solutions, such as automated checkouts and inventory management, as businesses adapted to social distancing guidelines. Additionally, the surge in demand for automation and remote operations during the pandemic boosted the adoption of computer vision in industries like logistics, security, and surveillance. As businesses sought ways to enhance efficiency and reduce human contact, computer vision played a crucial role in supporting automation. While certain industries faced short-term setbacks, the pandemic ultimately accelerated the integration of computer vision solutions across various sectors, reinforcing the market's long-term growth prospects.

Latest trends / Developments:

The Global Computer Vision Market is witnessing several key trends and developments, driven by advancements in AI, machine learning, and edge computing. One major trend is the increasing adoption of AI-powered computer vision systems across industries, enabling more sophisticated image and video analysis. This has led to enhanced applications in areas such as autonomous vehicles, where computer vision is crucial for navigation, object detection, and decision-making. The integration of computer vision with IoT devices is also gaining momentum, particularly in smart cities, manufacturing, and retail, enabling real-time data collection and analysis for improved decision-making and operational efficiency. Another notable development is the rise of edge computing, which allows computer vision systems to process data locally, reducing latency and enabling faster, more efficient analysis in applications such as surveillance and industrial automation. Additionally, computer vision is increasingly being used in healthcare for advanced diagnostics, including AI-assisted medical imaging and robotic surgery. The growing focus on privacy and data security is also shaping the market, as new regulations push for more secure and ethical use of computer vision, particularly in areas like facial recognition. These trends are poised to drive innovation and growth in the computer vision market, expanding its applications and capabilities.

Key Players:

-

Intel Corporation

-

NVIDIA Corporation

-

Cognex Corporation

-

Basler AG

-

Teledyne Technologies Inc.

-

Sony Corporation

-

Microsoft Corporation

-

Google LLC

-

Qualcomm Technologies Inc.

-

Omron Corporation