GLOBAL CHEMOTHERAPY - BASED HEPATOCELLULAR CARCINOMA (HCC) TREATMENT MARKET (2024 - 2030)

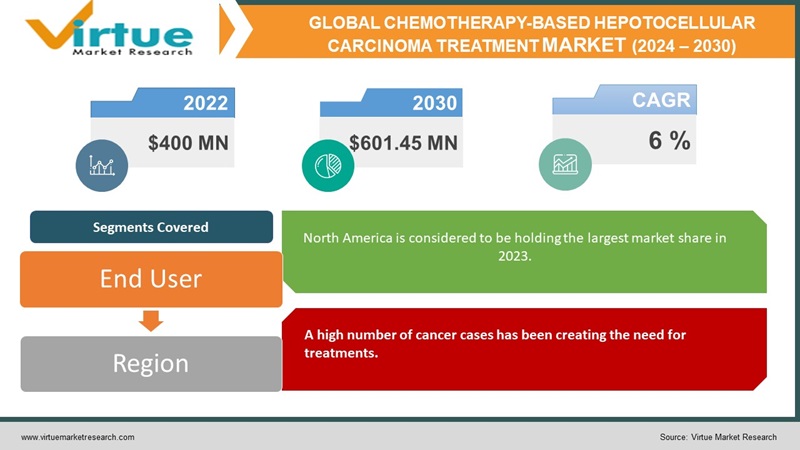

The global chemotherapy-based hepatocellular carcinoma (HCC) treatment market was valued at USD 400 million and is projected to reach a market size of USD 601.45 million by the end of 2030. Over the forecast period of 2024–2030, the market is projected to grow at a CAGR of 6%.

HCC, one of the most prevalent primary tumors of the liver, is a solid tumor of the liver. This is a very aggressive tumor that frequently develops in the context of cirrhosis and chronic liver disease. The most significant form of treatment for advanced hepatocellular carcinoma (HCC) is chemotherapy. In the past, this market had limited options and a small presence. Additionally, economic instability persisted, due to which only a very small fraction of the population was able to afford the treatment. Presently, the market has grown significantly owing to extensive efforts in research and developmental activities. In the future, with a growing focus on targeted therapies and personalized medicine, this market is set to see good growth.

Key Market Insights:

By 2027, it is anticipated that spending in the oncology sector will reach over 370 billion dollars. The CAGR for 2023–2027 is projected to be at most 16 percent.

By 2024, it is anticipated that Roche's cancer medicines will bring in 27.8 billion dollars in revenue.

Merck & Co.'s Keytruda produced around 21 billion dollars in sales in 2022, making it the most profitable cancer medicine globally. Patients with hepatocellular carcinoma (HCC) who have had sorafenib therapy in the past are eligible to receive KEYTRUDA.

When it comes to systemic therapy regimens, Lenvatinib and PD-1 inhibitors have been studied in several studies, with conversion success rates ranging from 15.9% to 30.8%. It is also linked to the lowest progressive disease rate and the greatest ORR (36.0–54.2%).

The most prevalent kind of liver cancer, or HCC, is also the fifth most common cause of cancer globally. Therefore, hospitals and other organizations have been taking measures to spread awareness about vaccinations against the hepatitis B virus (HBV). This vaccination is crucial, as a chronic attack of this virus can cause HCC cancer. Additionally, citizens are encouraged to undergo screening programs for early detection and diagnosis

Chemotherapy-based Hepatocellular Carcinoma (HCC) Treatment Market Drivers:

A high number of cancer cases has been creating the need for treatments.

Around 800,000 individuals worldwide receive a diagnosis of this illness every year, according to the American Cancer Society. An estimated 12,000 cases are caused each year in the United States due to this cancer, as per an article by Johns Hopkins University. Various factors contribute to the increasing prevalence of this disease. People who are diagnosed with hepatitis B, hepatitis C, and type 2 diabetes are at greater risk. Additionally, there have been many lifestyle changes over the years. Consumption of alcohol and smoking has increased significantly. Besides, obesity has been on the rise. All these factors have been contributing to ill health and the deaths of millions. Furthermore, many people are not aware of the symptoms of this particular cancer. Only 50% of people can survive for less than two years. Therefore, even though there are limited treatment options that ensure complete success, it is essential to reduce the pain. This demand for the therapies is helping the market grow.

Advancements in R&D activities have been contributing to the success.

Oncology research is one of the most popular and in-demand activities. Many prestigious institutions across the world have been focusing on finding effective remedies to stop tumor growth. To support this, governmental organizations, companies, and other business tycoons have been investing large amounts. The Food and Drug Administration (FDA) has approved various drugs that have proven to reduce the multiplication of tumors. Novel chemotherapeutic drugs, including oxaliplatin, have demonstrated effectiveness in the management of digestive tract malignancies, including colorectal, pancreatic, and stomach tumors. Some of these medications have also been investigated for the treatment of advanced HCC, with encouraging results based on positive outcomes.

The concept of personalized medicine has been facilitating market expansion.

Personalized medicine, also known as precision medicine, is the process where drugs are designed based on the genetic makeup of an individual. Biomarkers are used for this purpose because they provide information about the activities that take place in a cell. There have been many breakthroughs in understanding molecular pathways and other chemical reactions. Over the past ten years, systemic therapy for hepatocellular carcinoma (HCC) has advanced quickly. Physicians may now treat patients with advanced HCC with a greater variety of new medications, including immune checkpoint inhibitors and targeted therapies, either in parallel or sequential fashion.

Chemotherapy-based Hepatocellular Carcinoma (HCC) Treatment Market Restraints and Challenges:

Efficacy, side effects, costs, biomarker validation, and the emergence of other treatment options are the main issues that the market is currently experiencing.

One of the biggest hurdles in the market is the limited efficiency of chemotherapy agents. Few drugs can cause a toxic reaction. They may damage vital organs like the liver, kidneys, heart, lungs, and other reproductive parts. There is always a chance of relapsing with this condition. Secondly, this has been associated with a lot of side effects. Chemotherapies often lead to hair loss, nausea, mouth sores, reduction in immunity, loss of appetite, etc. It takes a toll on the physical and mental health of the individual. Thirdly, cancer treatments are very expensive. They need constant visits to the hospital, which can drain the individual financially. Moreover, the identification of the biomarker is a challenge. HCC is a deadly cancer that has complex molecular profiles. There haven't been many advancements in this regard. Furthermore, surgery, liver transplants, and other radiation therapies have garnered attention. Therefore, people might opt out of the treatment that has the best success rate, causing losses for this market.

Chemotherapy-based Hepatocellular Carcinoma (HCC) Treatment Market Opportunities:

Research and developmental activities are the primary factors that help broaden human knowledge. This field has an ample number of opportunities that benefit this market. Many studies and clinical trials are being carried out to find the most effective drugs. Currently, 115 drugs are in Phase 4. Drug repurposing is being emphasized. This is the process of finding new therapeutic uses for pharmaceuticals that are currently on the market or that are outdated. It is a useful method for finding or creating pharmaceutical compounds with novel pharmacological or therapeutic uses. Furthermore, combination therapies are being prioritized. This involves using chemotherapy along with other treatment options like immunotherapy and other targeted therapies. Apart from this, initiatives are being taken to improve awareness about various kinds of cancer. Governmental bodies have been generating schemes and other strategies to make sure that everybody has equal access to treatment.

GLOBAL CHEMOTHERAPY-BASED HEPATOCELLULAR CARCINOMA TREATMENT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6 %

|

|

Segments Covered

|

By End User and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Bayer AG, Eisai Co., Ltd., Bristol Myers Squibb (BMS), Merck & Co., Inc. (MSD)

Roche , AstraZeneca, Jiangsu Hengrui Medicine Co., Ltd., CStone Pharmaceuticals

BeiGene, Ono Pharmaceutical Co., Ltd.

|

Chemotherapy-based Hepatocellular Carcinoma (HCC) Treatment Market Segmentation:

Market Segmentation: By End-Users:

- Hospitals

- Specialty Clinics

- Research Institutes

- Others

Based on end-users, in 2023 the hospital segment is the largest segment in the market, holding a share exceeding 50%. The upsurge in this category is mainly because of the advanced treatment options that are offered over here. They offer comprehensive care and facilities that satisfy the needs of the patients, thereby increasing their trust. Secondly, these centers have licensed professionals, which include doctors, nurses, ward boys, and other essential workers. These people have been well equipped with knowledge and can perform various diagnoses, analyze the best possible treatment options, and provide 24/7 care. Apart from this, they offer various services like counseling, which is vital for a few patients to ensure that they have good mental well-being. Specialty clinics are considered to be the fastest-growing end-users in this market. These facilities are focused on a specific cancer type or other disorders. They offer specialized expertise, which includes oncologists and hepatologists who have renowned knowledge regarding different types of liver cancer. Besides, these facilities collaborate with research institutes and other organizations that work on drug discovery and development. This helps in gaining easy access to various chemotherapy drugs. Furthermore, few patients opt for these services, as specialized care is provided to the patients who are admitted. This leads to a more comfortable and trustworthy treatment, ensuring a faster recovery.

Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

Based on region, North America is considered to be holding the largest market share in 2023. The region holds a rough share of 34%. Countries like the United States and Canada are at the forefront. This region is known for its advanced healthcare facilities. The hospitals and clinics over here are well equipped with advanced infrastructure facilities, which can include drugs, beds, treatment, doctors, and other necessary services. Secondly, they have a good economy. This means that they have better investments and strength when it comes to carrying out R&D activities. This region has experienced major milestones in drug development and clinical trials. Prestigious institutes like Harvard, Cambridge, Johns Hopkins, Cornell, etc., have been the notable ones. Apart from this, this region has key players like AbbVie Inc., Amgen Inc., Bristol-Myers Squibb Company, Eli Lilly and Company, and many more who are actively involved in investing, partnerships, and developing oncology medications. Asia-Pacific is the fastest-growing region, with China, Japan, India, and Australia as the leading countries. This region holds an approximate share of 23%. One major factor in this is the rising incidence of HCC cancer cases. This is attributed to changes in lifestyle and diet. Secondly, significant progress has been made in spreading awareness. Various training activities and campaigns have been hosted by academic institutes and other major companies. This has led to the early detection of the disease. Thirdly, improving economic conditions have been responsible for the elevation. The funds allocated are being increased. This is leading to technological upgrades and extensive R&D activities. Furthermore, pharmaceutical companies have global operations, leading to increased partnerships and drug other advancements.

COVID-19 Impact Analysis on the Global Chemotherapy-based Hepatocellular Carcinoma (HCC) Treatment Market:

The pandemic hurt the market. Lockdowns, social isolation, and movement restrictions were the new norm. This caused a lot of disruptions in the supply chain, transportation, and other logistics. Routine screenings and the diagnosis of cancer were delayed. People were afraid to step out owing to virus contamination. Besides, cancer and other immunity-suppressed patients had a higher risk of coronavirus, due to which postponement and cancellation of appointments were observed. There was a lot of uncertainty due to financial restraints. Layoffs became common, and people were losing their jobs. Many of them were unable to afford treatments and other necessary facilities. An economic downfall was observed due to this. There was a shift in priorities, which included investments and clinical trials. Researchers were giving prominence to the vaccine development of the coronavirus. Furthermore, there was a decrease in cancer cases. The National Institute of Health stated that an online survey conducted in the Asian region reported a 26.7% decrease in the number of HCC cancer cases during the pandemic. Post-pandemic, the market has picked up with the resumption of R&D activities and technological adoption.

Latest Trends/ Developments:

The companies in this market are motivated to achieve a higher market share by implementing different strategies, such as acquisitions, partnerships, and investments. This has further resulted in increased enlargement.

To treat HCC, there has been a shift towards combining immunotherapy drugs, such as immune checkpoint inhibitors like pembrolizumab and nivolumab, with chemotherapy. Research and experimental trials are assessing the effectiveness of integrating immunotherapies with chemotherapy to improve patients' responsiveness to treatment and overall survival.

Key Players:

- Bayer AG

- Eisai Co., Ltd.

- Bristol Myers Squibb (BMS)

- Merck & Co., Inc. (MSD)

- Roche

- AstraZeneca

- Jiangsu Hengrui Medicine Co., Ltd.

- CStone Pharmaceuticals

- BeiGene

- Ono Pharmaceutical Co., Ltd.

In December 2022, Replimune and Roche signed a clinical collaboration agreement for the development of RP3 in hepatocellular carcinoma and colorectal cancer. For the first- and second-line therapy of hepatocellular carcinoma (HCC) as well as the third-line treatment of colorectal cancer (CRC), RP3 will be developed in conjunction with Bevacizumab and Atezolizumab.

In August 2022, BeiGene, a biotechnology company focused on developing innovative and affordable oncology medicines to improve treatment outcomes and access for patients worldwide, announced that the global Phase 3 rationale 301 trial with tislelizumab as a first-line treatment for adult patients with unresectable hepatocellular carcinoma (HCC) met its primary endpoint of non-inferior overall survival (OS) versus sorafenib. Tislelizumab's safety profile matched that of earlier research, and no new safety signals were noted.