Cervical Cancer Treatment Market Size (2024 – 2030)

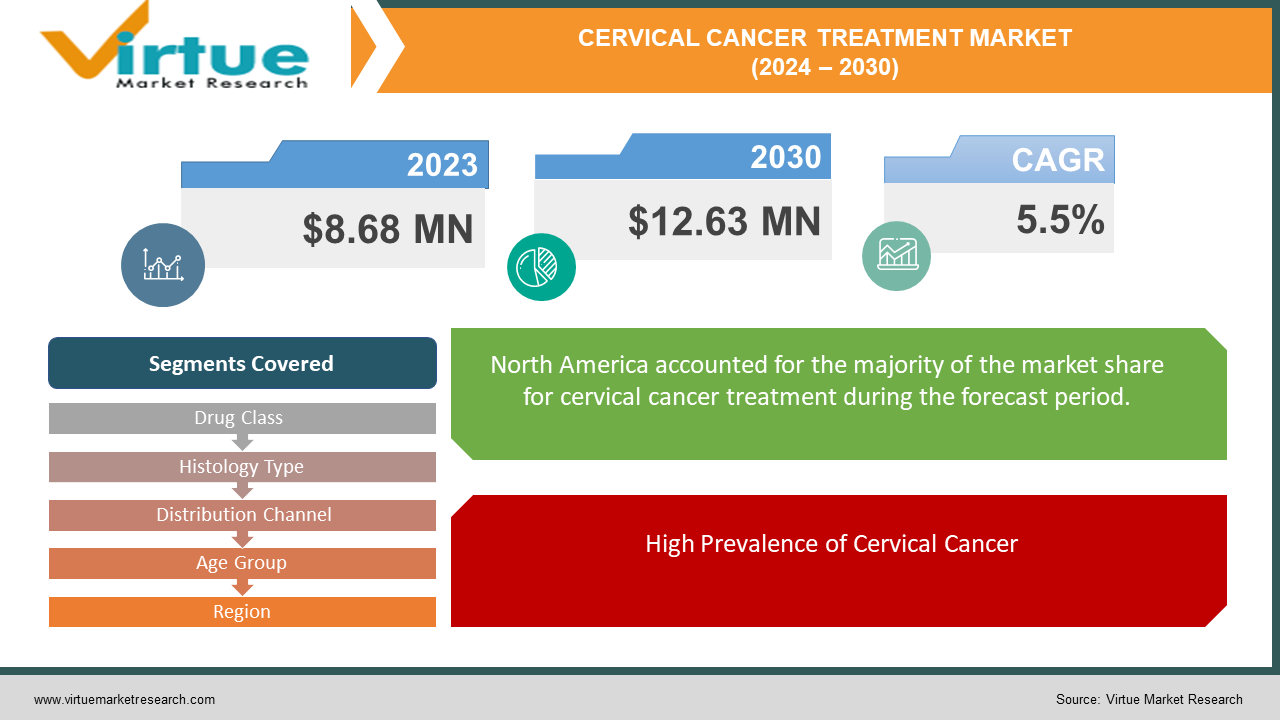

The Cervical Cancer Treatment Market was valued at USD 8.68 million in 2023. Over the forecast period of 2024-2030 it is projected to reach USD 12.63 million by 2030, growing at a CAGR of 5.5%.

Key Market Insights:

Cervical cancer exhibits a mortality rate of around 50%, yet this can be significantly reduced through early diagnosis and preventive measures. Given that the progression of the disease is typically gradual, there are opportunities to address and treat precancerous alterations. Many instances are detected at advanced stages due to insufficient awareness or limited access to diagnostic resources. Human Papillomavirus (HPV), predominantly transmitted sexually, is a primary cause of cervical cancer. There are over 100 HPV strains, with 13 identified as high-risk or oncogenic.

Cervical Cancer Treatment Market Drivers:

New Therapies drive the market growth.

New medications are continually being approved and introduced for the treatment of cervical cancer. Among these are Pembrolizumab, which is used in combination with chemotherapy, with or without bevacizumab, for patients with persistent, recurrent, or metastatic disease whose tumors express PD-L1 (CPS 1). The approval of tisotumab-vedotin-tftv for adult patients with recurrent or metastatic cervical cancer is also driving market growth. Another significant development is the expedited approval of Pembrolizumab as a second-line treatment for patients with recurrent or metastatic cervical cancer that has progressed during or after chemotherapy and whose tumors express PD-L1. Additionally, the use of bevacizumab for treating persistent, recurrent, or metastatic cervical cancer can significantly aid in patient recovery. Furthermore, the imminent launch of Pembrolizumab for treating second-line plus (2L+) patients with recurrent cervical cancer in Japan is anticipated to further stimulate market growth.

High Prevalence of Cervical Cancer

The mortality rate for cervical cancer is higher in developing countries due to inadequate early-stage detection. The rising number of cervical cancer cases presents a significant opportunity for market expansion. The adoption of advanced technologies in cancer treatment and the increase in chemotherapy treatments are expected to drive growth in the cervical cancer treatment market.

Cervical Cancer Treatment Market Restraints and Challenges:

Lack of Awareness hinders market growth.

The market for cervical cancer medications is hindered by a lack of awareness and various misconceptions about the disease. Delayed diagnoses are a significant factor in the high mortality rate among women with cervical cancer. Misinformation leads to delays in diagnosis, medication, and treatment, while ignorance results in avoidance of medical care. For example, a study conducted at the Bowen University Teaching Hospital (BUTH) interviewed approximately 318 women from the general outpatient clinic to assess their knowledge of cervical cancer. The awareness rate was found to be 22.6%, with 17.9% having undergone screening tests. The primary sources of information were health discussions and hospital staff.

Cervical Cancer Treatment Market Opportunities:

Growing Investments in Research and Development creates market growth.

The cervical cancer market has recently seen significant advancements with the introduction of immunotherapies combined with other treatment modalities. There is a notable trend in R&D strategies towards the use of immunotherapies in conjunction with other treatments for both front-line and second-line settings.

Additionally, leading market players are investing heavily in the development of new products and research, as well as engaging in major acquisitions and collaborations to gain a competitive advantage. Significant investments in R&D capabilities and infrastructure by both the industry and governments are expected to create lucrative market opportunities. For instance, in September 2021, Akeso, Inc. announced that China's National Medical Products Administration (NMPA) had officially accepted the new drug application for Cadonilimab (a PD-1/CTLA-4 bi-specific antibody) for the treatment of metastatic or relapsed cervical cancer.

CERVICAL CANCER TREATMENT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

5.5% |

|

Segments Covered

|

By Drug Class, Histology Type, Distribution Channel, Age Group, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Mylan N.V, Johnson & Johnson Private Limited, Sun Pharmaceutical Industries Limited, Sanofi S.A. CLOVIS ONCOLOGY , Alnylam Pharmaceuticals, Inc, Novartis AG, Merck & Co., Bayer AG , Vivesto AB , GSK plc

|

Cervical Cancer Treatment Market Segmentation - By Drug Class

-

Chemotherapy

-

Targeted therapy

The chemotherapy segment is the largest contributor to the cervical cancer treatment market. Chemotherapy utilizes powerful chemicals to destroy rapidly dividing cells in the body, a characteristic of cancer cells, which proliferate faster than most normal cells. There is a wide variety of chemotherapy drugs available, and many cancers can be treated using these medications alone or in combination with other therapies. While chemotherapy is effective for treating various types of cancer, it can also cause adverse effects. Some side effects are minor and manageable, while others can have significant negative impacts.

Targeted therapy employs medications that specifically target genes and proteins that help cancer cells survive and grow. This approach can modify the environment in which cancer cells exist within the body's tissues or target cells associated with cancer progression, such as blood vessel cells. Although not all cancer types currently have targeted treatments, this field is rapidly evolving, with many new targeted therapies being tested in clinical trials.

Cervical Cancer Treatment Market Segmentation - By Histology Type

-

Squamous Cell Carcinoma

-

Adenocarcinoma

-

Mixed Carcinoma

The squamous cell carcinoma (SCC) segment holds the largest market share in cervical cancer treatment. Squamous cell carcinoma originates in the squamous cells, which are thin, flat cells lining the part of the cervix that extends into the vagina. SCC constitutes the majority of cervical cancer cases. Although it can be aggressive, it is generally not life-threatening. The most common precursor lesion for SCC is a high-grade squamous intraepithelial lesion (HSIL), which is associated with high-risk human papillomavirus (HPV), particularly HPV 16 and HPV 18. The incidence of SCC is higher among women without adequate cytologic screening and in countries with limited resources.

Cervical Cancer Treatment Market Segmentation - By Distribution Channel

The retail and specialty pharmacies segment is the leading contributor to the market. This dominance is attributed to growing collaborations between government entities and the private sector with retail and specialty pharmacies. While retail pharmacies cater to short-term conditions, specialty pharmacies work closely with patients and doctors to provide medications for chronic and severe illnesses. Specialty pharmacies are designed to support patients with complex medical conditions that require intricate treatment regimens. These pharmacies often manage patients with chronic disorders, necessitating detailed medication management procedures. Consequently, specialty pharmacies provide extensive education and patient care services to ensure proper medication use and adherence.

Cervical Cancer Treatment Market Segmentation - By Age Group

-

Below 29 years

-

30-49 years

-

50+ years

The 50+ years segment holds the largest market share, driven by the fact that the average age at diagnosis for cervical cancer in women is 50 years. Many older women remain unaware that their risk of developing cervical cancer persists as they age. Women over 65 years old account for more than 20% of cervical cancer cases. However, women who have undergone regular cervical cancer screenings before the age of 65 are significantly less likely to develop this disease.

Cervical Cancer Treatment Market Segmentation- by region

-

North America

-

Europe

-

Asia Pacific

-

South America

-

Middle East & Africa

North America is the dominant region in the global cervical cancer therapeutics market, with the U.S. being the most significant contributor. This dominance is driven by increased disease prevalence, heightened consumer awareness, and advancements in technology for diagnosing and treating oncological diseases. The development of various cervical cancer vaccines and drugs also bolsters the regional market. Additionally, positive lifestyle changes are expected to further propel market growth in the region. Consequently, the U.S. cervical cancer treatment market is anticipated to experience substantial growth during the forecast period.

China is projected to grow at a compound annual growth rate (CAGR) of 5.84% over the forecast period. The growth in the Chinese cervical cancer market is attributed to the presence of key industry players and improved access to healthcare due to a well-established healthcare infrastructure. The increasing focus of vendors on research and development (R&D) to create novel drugs is expected to significantly impact market growth. The continuous involvement of primary and emerging players in R&D activities is likely to lead to the development of several innovative products in the coming years. The demand for cervical cancer treatment in China is primarily driven by the prevalence of the disease, the robust healthcare infrastructure, and the extensive reach of new therapeutics.

COVID-19 Pandemic: Impact Analysis

The COVID-19 pandemic significantly impacted the diagnosis and treatment of cervical cancer. A study published in the Diagnostics Journal in April 2022 revealed that during the initial lockdown in April 2020, the number of tests conducted dropped by 75.5%, leading to a subsequent decrease in the number of diagnosed cases by up to 36.1% in 2021. Over the first 24 months of the pandemic, there was a total loss of 49.9% in the volume of tests performed. The percentage of late-stage cervical cancers (stages III-IV) increased by 17%, while the number of newly diagnosed cases in outpatient clinics decreased by 45% compared to baseline levels. However, in the current scenario post-COVID-19, market growth is showing signs of stabilization as worldwide restrictions have eased and disease screening services have resumed.

Latest Trends/ Developments:

In September 2022, the Drugs Controller General of India (DCGI) authorized the Serum Institute of India (SII) to produce a domestically developed vaccine targeting cervical cancer. In June 2022, Karkinos Healthcare, an oncology-focused health-tech platform, introduced CerviRaksha. It is a pioneering HPV test, clinically validated and prequalified by the World Health Organization, and sanctioned by the Food and Drug Administration. This launch was in collaboration with Karkinos network hospital professionals, including doctors and nurses.

Key Players:

These are top 10 players in the Cervical Cancer Treatment Market: -

-

Mylan N.V

-

Johnson & Johnson Private Limited

-

Sun Pharmaceutical Industries Limited

-

Sanofi S.A. CLOVIS ONCOLOGY

-

Alnylam Pharmaceuticals, Inc

-

Novartis AG

-

Merck & Co.

-

Bayer AG

-

Vivesto AB

-

GSK plc