Counter-UAS Systems Market

In 2025, the Global Counter-UAS Systems Market was valued at approximately USD 3,214 million and is projected to reach around USD 8,472 million by 2030, expanding at a CAGR of about 21.4% during 2026–2030.

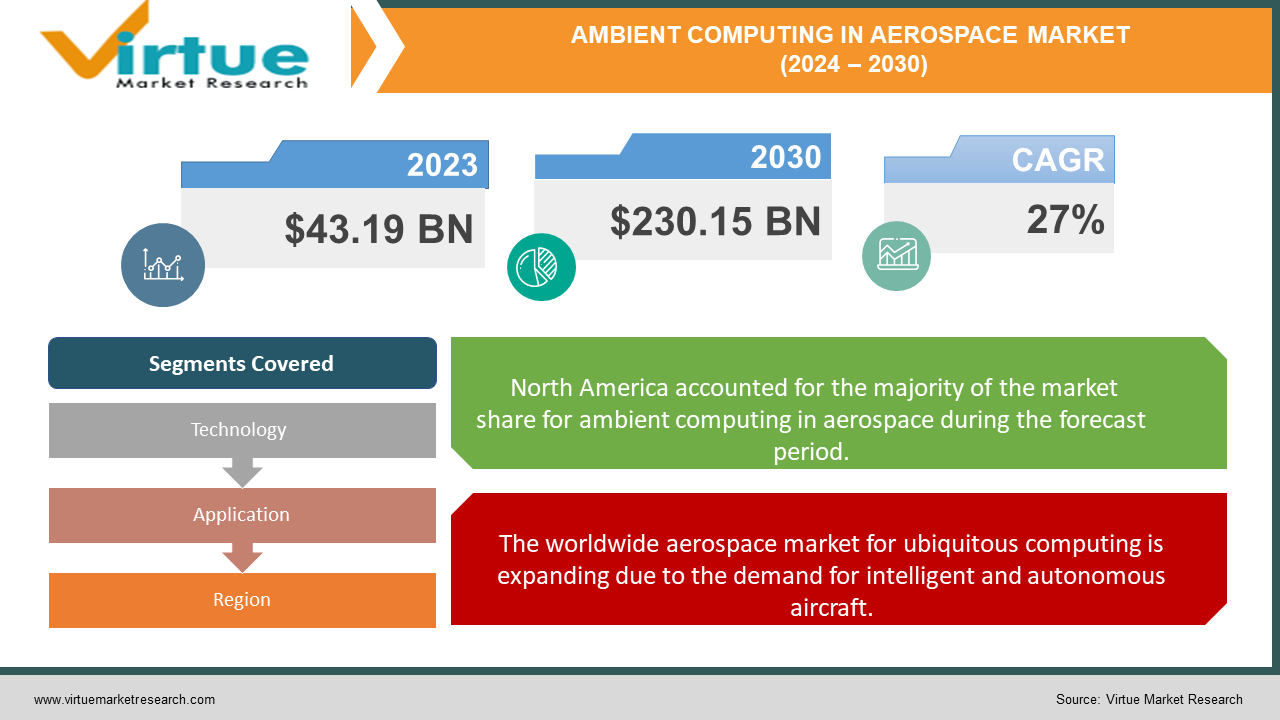

Explore reportThe Global Ambient Computing in Aerospace Market was valued at USD 43.19 billion in 2023 and is projected to reach a market size of USD 230.15 billion by 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 27%.

The aerospace industry uses a variety of technologies, including networks, sensors, and artificial intelligence, to build intelligent, self-sufficient systems. These developments can boost crew and passenger comfort while also enhancing aeroplane and spaceship performance and safety. Through providing relevant information, they can ensure security and offer customised services. Even though this subject offers many prospects for innovation and research, problems with usability, security, and privacy still need to be solved. Pervasive computing is expected to have a major influence on aeroplanes in the future.

Key Market Insights:

There's an opportunity to develop predictive maintenance solutions using ubiquitous computing. By utilising sensors built into aircraft components to track their health in real time and foresee potential issues before they develop, businesses can save maintenance costs and downtime. North America with a 40% market share dominates the Ambient Computing in Aerospace Market. Europe is the fastest-growing segment during the forecast period. The Internet of Things (IoT) is transforming aviation operations by connecting disparate aircraft components, ground infrastructure, and other devices. IoT sensors and gadgets may track the positions of things, check equipment performance, and gather environmental data. This increases productivity and lessens the likelihood of problems.

Global Ambient Computing in Aerospace Market Drivers:

The worldwide aerospace market for ubiquitous computing is expanding due to the demand for intelligent and autonomous aircraft.

Thanks to innovations in technology, such as self-healing components and smart systems, aeroplanes and spacecraft can fix themselves when they sustain damage. They may also operate together with other satellites or planes by utilising cutting-edge networking and artificial intelligence. Real-time data analysis increases productivity and reduces pollution. In addition to better services tailored to the demands of the passengers, safety is improved by reducing human mistake and weariness. This improves the efficiency and enjoyment of air travel while meeting the demands and preferences of passengers.

The global market for ubiquitous computing in the aerospace sector is expected to grow because of advancements in this discipline.

Sensors are devices that measure a range of characteristics, including movement, sound, light, and temperature. These tools are connected to PCs and servers via networks using either wired or wireless technologies. Artificial intelligence is the process of making computers clever enough to carry out activities requiring human-like learning, thinking, and decision-making. The creation of settings that facilitate easy computer collaboration is the aim of human-computer interaction. These technologies provide quick data analysis, insightful information provision, and communication in space and aviation. Additionally, by utilising techniques like augmented reality and digital twins, crew members and pilots may streamline and make their interfaces easier to use. These technologies are also utilised in the construction of astronaut smart houses and robotics for space exploration.

Global Ambient Computing in Aerospace Market Restraints and Challenges:

The capacity of a system to continuously carry out its intended function correctly under a range of circumstances is known as reliability. If a system can handle additional data without running into scalability problems, it is scalable. Systems that use ubiquitous computing, like those in aviation and space exploration, must integrate a lot of interconnected parts. Additionally, these systems need to be able to self-correct and adapt to changes. For this reason, they need to be flexible, error-tolerant, and able to disperse if a component fails.

Global Ambient Computing in Aerospace Market Opportunities:

The aircraft sector has several business potentials pertaining to ubiquitous computing. The need for real-time data analysis solutions is growing. These technologies' quick data collecting, processing, and interpretation capabilities allow for well-informed decision-making in flight operations, maintenance scheduling, and passenger services. There's an opportunity to develop predictive maintenance solutions using ubiquitous computing. By utilising sensors built into aircraft components to track their health in real time and foresee potential issues before they develop, businesses can save maintenance costs and downtime. Other prospects include developing contactless operational solutions, enhancing passenger experience with personalised services, and designing "smart" aircraft components that continually monitor performance and maintain safety. Pervasive computing generally presents chances to improve customer happiness, security, and productivity in the aircraft industry.

AMBIENT COMPUTING IN AEROSPACE MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

27% |

|

Segments Covered |

By Technology, Application, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Airbus Group SE, Bombardier Inc, General Dynamics, General Electric Company, Honeywell International Inc, Northrop Grumman Corp, Raytheon Technologies Corporation, Rolls-Royce Holdings plc, Safran SA, The Boeing Company |

Sensors

Networks

Artificial intelligence

Human-computer interaction

Sensors are devices that monitor light, temperature, movement, and other environmental factors. They have several uses in aeroplanes, including helping to ensure safe flying, monitoring the vehicle, and making sure the engines and structure are operating as they should. Because of their immense value in gathering data and helping with performance and safety concerns, sensors are predicted to play a significant role and increase quickly in the aerospace sector. Networks are systems that connect different technological components, including computers and servers, via wired or wireless connections. They make it easier for various components to communicate and share information. In the aerospace industry, networks are utilised for air traffic management and satellite-to-satellite communication.

Aviation

Space exploration

All facets of flying are included in the field of aviation, including the creation, maintenance, and use of aeroplanes, drones, and helicopters. It addresses many different subjects, including how aeroplanes are managed, function, and even the emotions of its occupants. Because of this, aviation contributes significantly to the widespread usage of technology in the aerospace sector. It makes flying more efficient, enjoyable, and safe for everyone. Many factors, like the amount of people who want to fly, aviation rules, creative ideas, and firm competitiveness, influence the market for employing technology in aeroplanes. Space exploration is similar in that it involves sending robots, satellites, and rockets into space to learn more about it.

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Aviation and space exploration are in high demand in North America. They make use of a vast array of cutting-edge technology, including as networks, sensors, and artificial intelligence. Therefore, it is expected that North America would lead the way in technical innovation in the aircraft industry. Europe is a major user of many of these cutting-edge technologies and has a strong interest in aviation and space exploration. Because of the plethora of fresh concepts, intense rivalry, and substantial expenditures, the European market for technology used in aeroplanes and spacecraft is growing at the quickest rate.

COVID-19 Impact Analysis on the Global Ambient Computing in Aerospace Market:

The COVID-19 epidemic has affected the aviation computing sector in both good and bad ways. Among the main problems it brought about for the aviation business were fewer passengers flying and a reduction in the demand for planes and cargo. As a result, airports, airlines, and aircraft manufacturers saw a decline in income. The epidemic also resulted in issues and delays in the manufacture and supply of aeroplane parts. On the plus side, more individuals started using technology to enhance safe flying. Enhanced communication, entertainment, and navigation are a few instances of this. In addition, there is a rising interest in satellite applications, including communication and Earth observation, as well as space exploration. Thus, while the epidemic caused problems, it also compelled the industry to use technology in more creative and efficient ways.

Recent Trends and Developments in the Global Ambient Computing in Aerospace Market:

The Internet of Things (IoT) is transforming aviation operations by connecting disparate aircraft components, ground infrastructure, and other devices. IoT sensors and gadgets may track the positions of things, check equipment performance, and gather environmental data. This increases productivity and lessens the likelihood of problems. It is essential to defend aircraft systems and components against cyberattacks as more and more are going digital. Aerospace companies are spending money on sophisticated data security solutions, such intrusion detection systems and strong encryption. Environmental stewardship is also highly appreciated in the aircraft industry. In aeroplanes, fuel consumption, toxic petrol emissions, and overall energy efficiency are all being decreased with the application of modern technologies. This includes using intelligent algorithms to identify the best flying paths, designing lighter aircraft, and working out how to improve the energy efficiency of aircraft equipment. Companies are working together more often to enhance their operations. By combining their resources and knowledge, they may create novel strategies for using technology in the aerospace sector. These agreements involve research institutes, tech businesses, and aerospace corporations. When they work together, their diverse skill sets and viewpoints will be combined to create outstanding solutions for the aerospace industry. Companies are focusing more on making sure their technology works with the equipment currently used in the aerospace sector. Their objective is to provide solutions that are easily incorporated into the systems and technology now used by the aerospace industry. They're promoting more seamless cooperation between different aircraft industry sectors by following set procedures and using common techniques for communication and data exchange. Establishing a unified and effective framework that promotes enhanced cooperation across the various aerospace sectors is the aim of this movement. Businesses are spending a lot of money on research and development (R&D) to produce new and better ideas. Their main goal is to improve the state-of-the-art ubiquitous computing technology and create innovative uses for them. By making R&D investments, businesses may stay ahead of the curve and satisfy client expectations. This facilitates their capacity to devise innovative solutions that tackle problems and capitalise on recently opened markets.

Key Players:

Airbus Group SE

Bombardier Inc

General Dynamics

General Electric Company

Honeywell International Inc

Northrop Grumman Corp

Raytheon Technologies Corporation

Rolls-Royce Holdings plc

Safran SA

The Boeing Company

The Global Ambient Computing in Aerospace Market size is valued at USD 43.19 billion in 2023.

The worldwide Global Ambient Computing in Aerospace Market growth is estimated to be 27% from 2024 to 2030.

Converging trends indicate that the aircraft industries worldwide ambient computing market is poised for development in the future. First, there's an increasing need for aeronautical systems to include self-healing and predictive maintenance features. Second, a networked environment for data collecting and analysis is being created by the combination of cloud computing and the Internet of Things (IoT) in aerospace applications. Lastly, more stringent laws are driving the need for sophisticated data analytics to guarantee security and safety, which is driving ambient computing's uptake in the aircraft industry.

There have been two ways in which the COVID-19 pandemic has affected the worldwide ambient computing in aircraft sector. It did, however, make remote monitoring and data analysis of aircraft systems more necessary. However, delays in projects and interruptions in the supply chain hindered expansion.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.