Counter-UAS Systems Market

In 2025, the Global Counter-UAS Systems Market was valued at approximately USD 3,214 million and is projected to reach around USD 8,472 million by 2030, expanding at a CAGR of about 21.4% during 2026–2030.

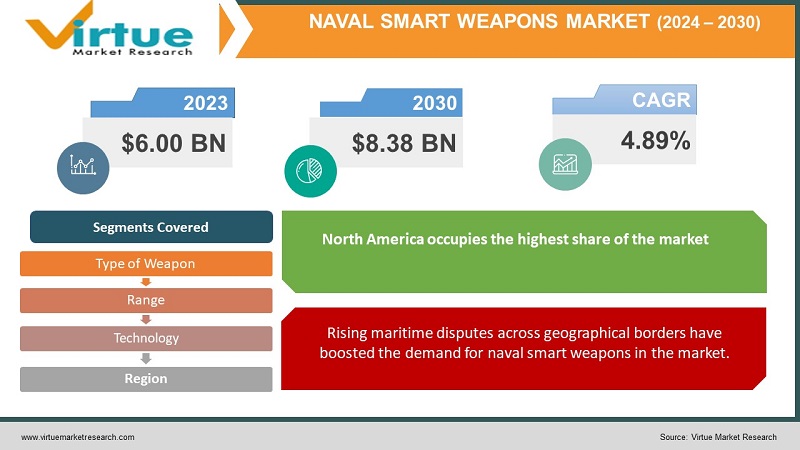

Explore reportThe Naval Smart Weapons Market was estimated to be worth USD 6.00 Billion in 2023 and is anticipated to reach a value of USD 8.38 Billion by 2030, growing at a fast CAGR of 4.89% during the forecast period 2024-2030.

Naval smart weapons are technologically updated weapons that are used by naval forces. These weapons are equipped with advanced features that offer higher efficiency and accuracy. Moreover, these weapons have high-tech sensors, guidance systems, and communication systems for enhanced protection across ocean or sea borders. Some of the most common naval smart weapons used by navy forces are precision-guided missiles, anti-ship missiles, anti-submarine warfare weapons, cruise missiles, aerial drones, and others. Further, these advanced machines are increasingly used during naval warfare and for air defense purposes. Additionally, smart anti-ship missiles, smart anti-field weapons, and smart rifles are used for counter-attacking and combat threats posed by pirates, armed robbery, drug smugglers, and others. Furthermore, advancements in technology and rising demand for fast and precision warfare machines have increased the demand for naval smart weapons in the market.

Global Naval Smart Weapons Market Drivers:

Technological advancements have boosted the demand for naval smart weapons in the market.

Advances in naval warfare technologies have enhanced protection across ocean and sea boundaries, leading to an increase in demand for accurate and precision technologies. Furthermore, the infusion of AI and machine learning algorithms have enabled navy forces to remotely monitor unusual movement through its connection to smart GPS navigation systems. Moreover, the use of unmanned aerial drones has made it possible for navy forces to map long distances and prevent attackers from entering the territories. Furthermore, advanced sensors such as multi-mode sensors have enabled smart missiles to analyze different types of targets and minimized the risk of hitting or shooting at the wrong targets. Furthermore, electromagnetic railguns and directed energy weapons are increasingly used in the navy for propelling projectiles and beams of energy at high speeds, thereby making it possible to perform long-range attacks. Additionally, the growing trends in AI have enabled navy forces to combat enemies with automated weapons that are sent in swarms to attack enemies. It also allows for remote monitoring of weapon delivery via advanced communications networks.

Rising maritime disputes across geographical borders have boosted the demand for naval smart weapons in the market.

Maritime disputes arise from the political ideologies of nations, influence from illegal sources, and territorial disputes, leading to greater threats to the nation’s safety. These disputes further tamper the military and navy forces of the nations and lead to conflict, which requires the use of smart and accurate naval weapons. Further, the most common contributor to maritime disputes is territorial conflicts that arise between two or more nations fighting over territorial claims or overlapping EEZ (Exclusive Economic Zones) disputes. These disputes require protecting the natural habitat of the nation such as fisheries and other marine animals, energy resources, and protecting the maritime boundaries, which increases the demand for smart naval weapons. These include anti-ship missiles meant for defending the maritime boundaries from unauthorized and illegal ships entering the territorial boundaries, coastal defense batteries used to operate anti-ship artillery or fixed gun batteries in coastal fortifications, and use of naval mines that are placed deep inside the water for destroying surface ships and submarines from attacking. These mines are specifically placed in water to deny the entry of maritime enemies into local territories.

Global Naval Smart Weapons Market Challenges:

The expensive cost of deploying naval smart weapons can decline its market growth. Naval smart weapons are equipped with advanced sensors and guidance systems, which require high-end technology to produce and manufacture smart weapons, raising the final cost for its users.

Further, a lack of proper technical training and education in operating naval smart weapons can reduce their effectiveness and result in mission failure, which can decline the demand for naval smart weapons in the market.

Global Naval Smart Weapons Market Opportunities:

The Global Naval Smart Weapons Market is anticipated to deliver lucrative opportunities for businesses, which include acquisitions, partnerships, collaborations, product launches, and agreements during the forecasted period. Furthermore, rising demand for enhanced protection across maritime boundaries due to an increase in maritime disputes among countries across the world is predicted to develop the market for Naval Smart Weapons and enhance its future growth opportunities.

COVID-19 Impact on the Global Naval Smart Weapons Market:

The pandemic hurt the naval smart weapons market. Due to the lockdown, major weapons-making manufacturing units were closed down leading to delays in the production of naval smart weapons. Further, travel restrictions created a shortage of major components used in building naval smart weather declining the demand for naval smart weapons in the market. Moreover, the reallocation of the budget by the government towards the healthcare sector during the pandemic such as for relief, vaccine production and distribution, for hospitals, and others, halted the production of smart navy weapons in the market.

Global Naval Smart Weapons Market Recent Developments:

In June 2023, Boeing Company announced to launch kits to the USA to convert anti-submarine torpedoes into high-altitude long-range glide weapons. The product is designed to help navy forces to detect, track, and attack enemy submarines autonomously.

NAVAL SMART WEAPONS MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

4.89% |

|

Segments Covered |

By Type of Weapon, Range, Technology, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Boeing Company, BAE Systems, General Dynamics Corporation, Raytheon Technologies Corporation, Lockheed Martin Corporation, Hyundai WIA, Bharat Dynamics Ltd |

Missiles

Ammunition

Drones

Warfare and Control Systems

Mines

Others

In 2022, based on market segmentation by type of weapon, missiles occupy the highest share in the market. These missiles include anti-ship missiles, anti-submarine missiles, surface-to-air missiles, cruise missiles, and others. These missiles are equipped with advanced guidance systems that enable navy forces to track enemies and target enemy ships, and other attackers. Moreover, anti-ship missiles are increasingly used in maritime boundaries for targeting unauthorized and illegal access to ships and vessels, as these weapons are equipped with advanced sensors and guidance systems that offer remote monitoring and enemy attack information before projecting the missiles to attack them.

The ammunition segment is the fastest-growing segment during the forecast period. Ammunitions include smart guns, artillery shells, rockets, and precision munitions that are specifically designed to attack enemies and reduce risks across maritime boundaries. Artillery shells are increasingly used to hit the target on land or sea, or ocean. These are fired directly from naval guns and are equipped with multimode sensors and laser-based guidance systems that allow for predicting the weather and environment for easy targeting of enemies.

Short-Range

Medium-Range

Long-Range

In 2022, based on market segmentation by range, short-range occupies the highest share in the market. Short-range naval smart weapons are designed to target enemies at closer distances. These weapons are used to target enemies within the short-range radar and are increasingly used for coastal defense, protection of harbors, and maritime boundaries. Short-range surface-to-air missiles and anti-ship missiles are some examples of short-range naval smart weapons.

Long-range naval smart weapons are the fastest-growing segment during the forecast period. These weapons are used to attack enemies at a longer distance. Further, long-range weapons are used for power projection, attacking enemies at far-reaching distances, and for reducing potential collateral damage by preventing them from entering territorial boundaries. Long-range unmanned aerial vehicles and long-range anti-ship missiles are some examples of long-range naval smart weapons.

Guidance Systems

AI Systems

Propulsion Systems

Seekers

Others

In 2022, propulsion systems occupy the highest share of the market. Propulsion systems are increasingly used in navy forces for fast-moving targets and help in enhancing the effectiveness of naval smart weapons. Jet propulsions, rocket propulsions, and electromagnetic propulsions are some examples of propulsion systems used in navy forces. They are usually used to launch air missiles such as anti-ship missiles and are increasingly used for fast-moving and longer targets.

AI systems are the fastest-growing segment during the forecast period. These have gained momentum due to accuracy and enhanced protection. Moreover, naval weapons equipped with AI and machine learning algorithms enable navy forces to plan and make better target decisions. Further, AI algorithms help in recognizing the target through advanced sensors and provide visual imagery of enemies on guidance systems. Further, autonomous naval robots such as aerial drones and navigation systems help in detecting obstacles and target movement in real-time by allowing navy forces to remotely monitor it. Furthermore, advanced AI models help in assessing potential threats by detecting incoming missiles, aircraft, or ships to local territories and allow navy forces to plan defensive measures immediately.

North America

Europe

Asia Pacific

Middle East and Africa

South America

In 2022, based on market segmentation by region, North America occupies the highest share of the market. The presence of advanced technologies and naval capabilities are driving the growth of naval smart weapons in the region.

Asia-Pacific is the fastest-growing region during the forecast period. Maritime disputes among countries such as China, Vietnam, and others over claiming islands and waters, and rapid technological adoption by South-East Asian countries have contributed to the demand for naval smart weapons in the region.

Global Naval Smart Weapons Market Key Players:

Boeing Company

BAE Systems

General Dynamics Corporation

Raytheon Technologies Corporation

Lockheed Martin Corporation

Hyundai WIA

Bharat Dynamics Ltd

The Naval Smart Weapons Market was estimated to be worth USD 6.00 Billion in 2023 and is anticipated to reach a value of USD 8.38 Billion by 2030, growing at a fast CAGR of 4.89% during the forecast period 2024-2030.

Technological advancements and Rising maritime disputes across geographical borders are the market drivers for Global Naval Smart Weapons Market.

Missiles, Ammunition, Drones, Warfare and Control Systems, Mines, and Others are the segments under Global Naval Smart Weapons Market by type of weapon.

North America dominates the market for Global Naval Smart Weapons Market.

Asia-Pacific is the fastest-growing region in the Global Naval Smart Weapons Market.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.