Silicon Photonics market Research Report - Segmented By Component (Optical Waveguides , Optical Modulators , Photodetectors Wavelength-Division Multiplexing (WDM) Filters, Laser); By Application(Data Centers and High-performance, computing Telecommunication Military, Defense and Aerospace, Medical and Life Science, Other); By Product (Transceivers , Active Optical Cables, Optical Multiplexers, Optical Attenuators, Others); and Region - Size, Share, Growth Analysis | Forecast (2023 – 2030)

Silicon Photonics Market SIze (2023 - 2030)

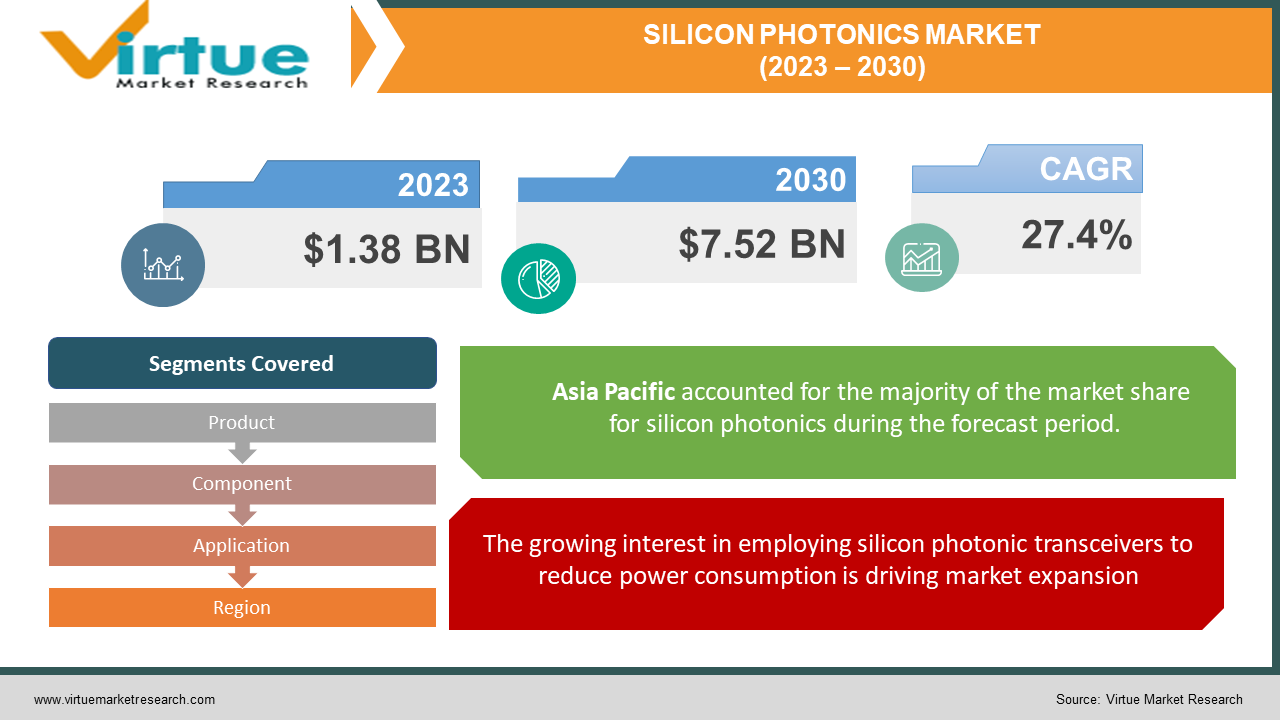

The Global Silicon Photonics market was valued at USD 1.38 billion and is projected to reach a market size of USD 7.52 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 27.4%.

INDUSTRY OVERVIEW

A recent and developing area of study called silicon photonics makes use of photonic systems to greatly speed up the production, transmission, and processing of data between microchips. This technology uses silicon as the optical medium for data transport. Numerous manufacturers are implementing this technology to enhance the processing and computing power of data centers as a result of the ongoing requirement for higher data transfer speeds. Due to its decreased prices and energy consumption, silicon photonics is expanding steadily. The majority of firms support silicon photonics and are prepared to invest in this technology to obtain a competitive edge. There is a high demand for silicon photonics because of its use in the medical and life sciences, military, communications, and data centre industries, among others. The factor anticipated to boost market expansion globally is the increasing usage of automated production techniques and cutting-edge technological advancements. Numerous businesses are adopting silicon photonics technology as a result of the silicon being used so often in the creation of integrated circuits. The spread of 5G technology and the rise in bandwidth demand will provide businesses more chances to advance their research program in the photonics sector. This innovative technology will aid in the effective transformation of the radio access network and the routing of a significant volume of data traffic during 5G transmission. With the rising need for new safety technologies like an improved vision in automobiles, silicon photonics technology is also making progress in the automotive industry. Leaders in the market are consistently concentrating on incorporating the newest technology into LiDAR chips, expanding their potential for growth in the automotive industry. However, the COVID-19 epidemic has impacted the silicon photonics market's total manufacturing capacity due to a lack of competent labor. The Chinese semiconductor industry's decline has had a significant negative influence on the market expansion. However, as the number of people working from home increases globally, so will the need for 5G technology.

COVID-19 IMPACT ON THE SILICON PHOTONICS MARKET

As a result of the COVID-19 outbreak's impact on the component supply, industrial disruptions, and global value chains, demand and consumer expenditure is slowing down. Due to the high acceptability of the work-from-home norm, and a greater propensity for television viewing and online learning, among other factors, there has been a rise in internet usage since the COVID-19 pandemic outbreak. However, the rising usage of digital services has also led to businesses cutting back on spending or laying off workers. As a result, the sale of networking hardware, such as silicon photonic devices, has significantly decreased. One of the fastest-growing uses for silicon photonic technologies is anticipated to be in data centres and high-performance computing. The deployment of the 5G network, which is now in its first stages, has been hampered by COVID-19. This has caused a delay in the rollout of the 5G network, which will have an impact on the expansion of the silicon photonics industry during the course of FY 2021–2022.

MARKET DRIVERS:

The growing interest in employing silicon photonic transceivers to reduce power consumption is driving market expansion

It is challenging to accommodate the rising demand for high-speed data transport using traditional copper connections. This problem of the constrained spectral range is resolved by the use of silicon photonic transceivers and optical interconnects. Additionally, silicon photonics-based components used in communication networks, such as transceivers, interconnects, and switches, utilize less power. CISCO and Intel, for example, have developed optical switches with low power consumption (0.6 mW) and high switching speeds of 6 ns. In contrast to conventional goods, which rely on board-to-board and computer-to-computer integrations, silicon photonic devices are built on on-chip integration, which not only shrinks the size of the product but also aids in lowering power consumption.

Demand for high-speed internet services is increasing which is fueling the market expansion

With the widespread deployment in governmental organizations, businesses, and other applications, the need for high-speed broadband services is sharply increasing. According to IMEC, in the coming years, data centre optical links will be upgraded to 400Gb/s capacity, increasing the total bandwidth that can be handled by a single data centre switch to 51.2Tb/s. This will necessitate the use of ultra-high-density silicon photonics transceiver technology, which must be tightly integrated and co-packaged with the switch CMOS chip. In high-speed broadband applications, silicon photonics-based devices including modulators, waveguides, transceivers, and so on are widely employed. As a result, the market will be driven by the increasing demand for high-speed internet.

New uses for silicon photonics will drive market growth

Numerous applications, including sensors and high-performance computers, use silicon photonics. The market impact of the large sensor deployment in autonomous cars and the expanding attempts to produce autonomous vehicles is examined. To provide LiDAR solutions for driverless vehicles, SiLC, a top company in silicon photonics chips, revealed in March 2020 that it had received $12 million.

MARKET RESTRAINTS:

On-chip laser integration is difficult which is restraining the market growth

The Silicon Photonics sector has invested much in research, but the work has remained fragmented, with advancements occurring only at the component level. The integration of complicated systems like high-performance computing with silicon photonics devices is where the actual problem resides. Even though not many products have yet to be released, significant R&D expenditures have still to be made in Silicon Photonics. The sole practical alternative accessible to makers of Silicon Photon Devices has been semiconductor laser, either through wafer-to-wafer bonding or wafer-to-chip bonding. Since silicon lasers have not yet been developed, it may take many years until they are produced in their commercial form, which limits the integration of light sources beyond the device. The alignment of laser connections about waveguides, which is essential for high transmission rates, also presents difficulties, which will restrain market expansion.

SILICON PHOTONICS MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2022 - 2030 |

|

Base Year |

2022 |

|

Forecast Period |

2023 - 2030 |

|

CAGR |

27.4% |

|

Segments Covered |

By Product, Component, Application, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

AIO CORE CO. LTD., CISCO SYSTEMS INC., FINISAR CORPORATION, HAMAMATSU PHOTONICS K.K, IBM CORPORATION, INFINERA CORPORATION., INTEL CORPORATION, IPG PHOTONICS CORPORATION, MELLANOX TECHNOLOGIES LTD., SICOYA, STMICROELECTRONICS NV |

This research report on the Silicon Photonics Market has been segmented and sub-segmented based on Component, Product, By Application and By Region.

SILICON PHOTONICS MARKET – BY COMPONENT

- Optical Waveguides

- Optical Modulators

- Photodetectors

- Wavelength-Division Multiplexing (WDM) Filters

- Laser

Based on the component, the Silicon Photonics market is segmented into Optical Waveguides, Optical Modulators, Photodetectors, Wavelength-Division Multiplexing (WDM) Filters and Laser. By 2030, it is predicted that the WDM filters sector would be the largest and rule the component market in terms of size. WDM filters make it possible to use modern electronics and fibers, but they do it by sharing fibers by sending distinct channels at various light wavelengths. Increased expansion in the telecommunication and data communication sectors is sparked by the widespread use of the Internet, where the WDM filter plays a significant role.

SILICON PHOTONICS MARKET - BY PRODUCT

- Transceivers

- Active Optical Cables

- Optical Multiplexers

- Optical Attenuators

- Others

Based on the product, the Silicon Photonics market is segmented into Transceivers, Active Optical Cables, Optical Multiplexers, Optical Attenuators and Others. In terms of size in 2021, the Active Optical Cables (AOC) category was the largest. AOC can use silicon photonic devices to send large amounts of data at rapid speeds across great distances. For high-performance computer and storage applications, active optical cables offer simpler installation and considerable cost savings over conventional optical modules. From 2023 - 2030, the optical multiplexers market will see the highest CAGR.

SILICON PHOTONICS MARKET - BY APPLICATION

- Data Centers and High-performance computing

- Telecommunication

- Military, Defense and Aerospace

- Medical and Life Science

- Other

Based on the application, the Silicon Photonics market is segmented into Data Centers and High-performance computing, Telecommunication, Military, Defense and Aerospace, Medical and Life Science, and Other Applications. By 2030, it is anticipated that the application sector for data centres and high-performance computing would command the biggest market share. Demand for silicon photonics is rising as high-performance computing (HPC) applications spread and data centres expand in size, especially those used in high-bandwidth optical transceivers. The expansion of data centres through 2021 as a result of increased commercial and consumer traffic may present a sizable potential for the silicon photonics industry. Computing and cooperation inside the organisation are the main factors influencing workload and computation requirements in data centres. Due to this performance improvement, silicon photonics now has greater room to function without connectivity constraints. In addition to the massive rise in the data flow, the Internet of Everything (IoE) design emphasises the need for real-time reactions between people and objects. Big data analysis, cloud computing, and cognitive computing are all playing an increasing role in data processing and traffic management, which puts pressure on market vendors to deliver the speed and capacity required to generate a swift response. Silicon nanophotonics technology is rapidly being used in optical communication systems. The silicon Photonics market is anticipated to expand rapidly over the course of the forecast period as a result of demand from large data centres and the introduction of 5G technologies. High-speed silicon photonics-based technologies are making it possible to create smaller form factors with more bandwidth and improved power efficiency. On the consumer side, streaming video and other media is the major source. In response to the anticipated data centre traffic, significant corporations like Google, Facebook, and Microsoft are getting ready to expand their worldwide data centre volumes. As a result, compared to conventional electronics, the need for long-distance data transport may grow throughout the anticipated period.

SILICON PHOTONICS MARKET - BY REGION

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East

- Africa

By region, the Silicon Photonics Market is grouped into North America, Europe, Asia Pacific, Latin America, The Middle East and Africa. With the greatest revenue share in the worldwide Silicon Photonics Market, Asia Pacific led the industry. Rising demand for high-speed internet networks and more use of mobile devices in the region are the main drivers of this regional growth. The region's Silicon Photonics Market is expanding as a result of rising technical advancements. In addition, encouraging government initiatives and the abundance of cheap labor are anticipated to boost market expansion. Additionally, due to the growing utilization of high-speed broadband networks, North America is anticipated to favour the silicon photonics market with a progressive CAGR during the anticipated years. Additionally, the presence in the United States of major market players like Intel, IBM, and Cisco, among others, is anticipated to open up tremendous prospects for market expansion.

SILICON PHOTONICS MARKET - BY COMPANIES

Some of the major players operating in the Silicon Photonics Market include:

- AIO CORE CO. LTD.

- CISCO SYSTEMS INC.

- FINISAR CORPORATION

- HAMAMATSU PHOTONICS K.K

- IBM CORPORATION

- INFINERA CORPORATION.

- INTEL CORPORATION

- IPG PHOTONICS CORPORATION

- MELLANOX TECHNOLOGIES LTD.

- SICOYA

- STMICROELECTRONICS NV

NOTABLE HAPPENING IN THE SILICON PHOTONICS MARKET

- ACQUISITION- Intel Corporation procured Tower Semiconductors in February 2022 to enable a globally diversified product portfolio to meet the rising demand for semiconductors. Additionally, this purchase allows the business to provide a global clientele with foundry services.

- PRODUCT LAUNCH- Global Foundries launched the latest generation of silicon photonics solutions in March 2022 and worked with leading business figures to usher in a new age of greater data center capacity. It may be possible to meet the faster increase of skyrocketing data volumes while drastically reducing power consumption using a first-of-its-kind silicon photonics design.

- COLLABORATION- In October 2021, Cisco Systems and researchers from UC Santa Barbara teamed up to develop new quantum technology applications. This partnership is a component of Cisco's strategy toward the advancement of quantum technologies.

Chapter 1.SILICON PHOTONICS MARKET – Scope & Methodology

1.1. Market Segmentation

1.2. Assumptions

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2.SILICON PHOTONICS MARKET – Executive Summary

2.1. Market Size & Forecast – (2022 – 2026) ($M/$Bn)

2.2. Key Trends & Insights

2.3. COVID-16 Impact Analysis

2.3.1. Impact during 2022 - 2026

2.3.2. Impact on Supply – Demand

Chapter 3.SILICON PHOTONICS MARKET – Competition Scenario

3.1. Market Share Analysis

3.2. Product Benchmarking

3.3. Competitive Strategy & Development Scenario

3.4. Competitive Pricing Analysis

3.5. Supplier - Distributor Analysis

Chapter 4.SILICON PHOTONICS MARKET - Entry Scenario

4.1. Case Studies – Start-up/Thriving Companies

4.2. Regulatory Scenario - By Region

4.3 Customer Analysis

4.4. Porter's Five Force Model

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Powers of Customers

4.4.3. Threat of New Entrants

4.4.4. Rivalry among Existing Players

4.4.5. Threat of Substitutes

Chapter 5. SILICON PHOTONICS MARKET - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6.SILICON PHOTONICS MARKET – By COMPONENT

6.1. Optical Waveguides

6.2. Optical Modulators

6.3. Photodetectors

6.4. Wavelength-Division Multiplexing (WDM) Filters

6.5. Laser

Chapter 7.SILICON PHOTONICS MARKET – By PRODUCT

7.1. Transceivers

7.2. Active Optical Cables

7.3. Optical Multiplexers

7.4. Optical Attenuators

7.5. Others

Chapter 8.SILICON PHOTONICS MARKET – By APPLICATION

8.1.Data Centers and High-performance computing

8.2. Telecommunication

8.3. Military, Defense and Aerospace

8.4. Medical and Life Science

8.5. Other

Chapter 9.SILICON PHOTONICS MARKET – By Region

9.1. North America

9.2. Europe

9.3. The Asia Pacific

9.4. Latin America

9.5. The Middle East

9.6. Africa

Chapter 10SILICON PHOTONICS MARKET – Company Profiles – (Overview, Product Portfolio, Financials, Developments)

10.1. AIO CORE CO. LTD.

10.2. CISCO SYSTEMS INC.

10.3. FINISAR CORPORATION

10.4. HAMAMATSU PHOTONICS K.K

10.5. IBM CORPORATION

10.6. INFINERA CORPORATION.

10.7. INTEL CORPORATION

10.8. IPG PHOTONICS CORPORATION

10.9. MELLANOX TECHNOLOGIES LTD.

10.10. SICOYA

10.11. STMICROELECTRONICS NV12.14. Airgas

Download Sample

Choose License Type

2500

4250

5250

6900